[ad_1]

Scharfsinn86

Note:

I have covered Westport Fuel Systems Inc. (NASDAQ:WPRT) previously, so investors should view this as an update to my earlier articles on the company.

After the close of Monday’s regular session, Westport Fuel Systems Inc. or “Westport” reported mixed fourth quarter and full year 2023 results.

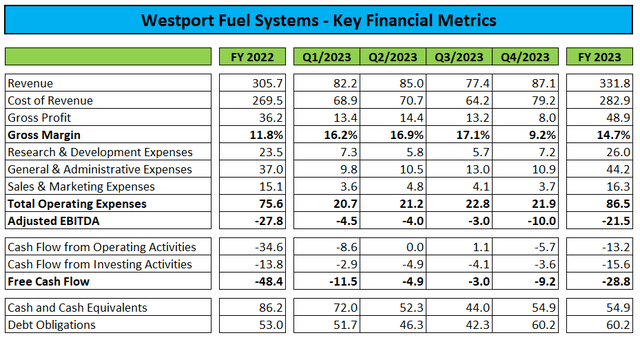

While revenues of $87.2 million came in slightly above consensus expectations, gross margins were impacted by an aggregate $5.0 million of inventory write-downs.

Company Press Releases

Adjusted for the write-downs, consolidated Q4 gross margin would have been 14.9%, much closer to the company’s performance in the first nine months of 2023.

While free cash flow for the quarter was negative $9.2 million, higher drawdowns under the company’s revolving credit facility and the addition of new term loan facilities in Italy resulted in cash and cash equivalents increasing by $10.9 million sequentially to $54.9 million.

Subsequent to quarter-end, the company closed on an additional $3.8 million term loan facility in Italy.

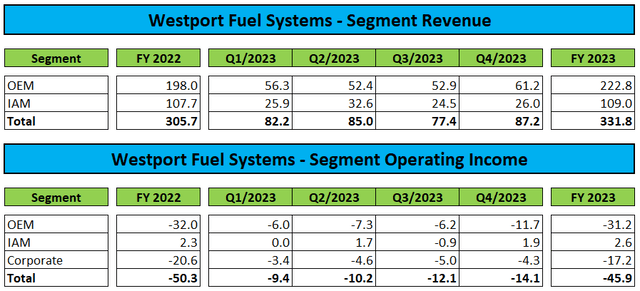

Westport’s Q4 segment performance showed the usual pattern of the smaller Independent Aftermarket (“IAM”) business operating at a modest profit while the larger Original Equipment Manufacturer (“OEM”) segment continues to experience material losses:

Company Press Releases

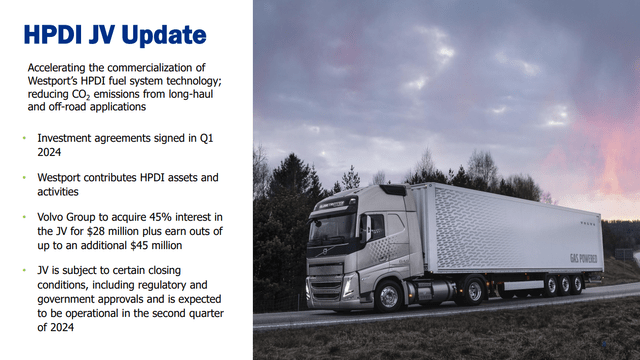

However, the company’s proposed High Pressure Direct Injection (“HPDI”) joint venture with key customer AB Volvo or “Volvo” (OTCPK:VLVLY, OTCPK:VOLAF, OTCPK:VOLVF) will have a material impact on Westport’s financial position, results of operations, and cash flows going forward.

Company Presentation

Two weeks ago, the company and Volvo entered into definitive agreements for the establishment of the joint venture, as outlined in Westport’s financial statements:

As part of the formation of the JV, the Company will contribute certain HPDI™ assets and liabilities, including related fixed assets, intellectual property, and net working capital. The Volvo Group will acquire a 45% interest in the JV for an initial consideration of $28,350. The JV is to be jointly controlled by both parties, and is intended to enhance the commercialization of Westport’s HPDI™ fuel system technology and to accelerate the decarbonization efforts of global OEM customers. Upon closing of the JV with Volvo Group, the HPDI business will be operated through the joint venture.

The Company’s preliminary assessment is the interest in the JV is to be accounted for using the equity method. Under this method, the Company’s initial investment in the JV is recognized at cost and subsequently adjusted for the Company’s share of the JV’s net income or loss and other comprehensive income, as well as for dividends or distributions received from the JV.

In layman’s terms: Upon formal closing of the joint venture (currently expected in Q2), Westport will receive a $28.4 million cash payment from Volvo. However, the requirement to fund the joint venture on a pro rata basis will offset the positive impact on liquidity somewhat.

In addition, the company will no longer consolidate the money-losing HPDI business, thus resulting in decreased OEM revenues, improved segment gross margins and substantially reduced losses from operations, as well as materially lower cash outflows going forward.

Consequently, I would expect the company’s liquidity to remain sufficient until at least 2026, particularly given new management’s stated focus on cost-cutting, as discussed on the conference call:

In the near term, we are focusing on cutting costs and optimizing operations. Nothing is off limits. We have already begun to identify and eliminate redundancies, and we are looking at spending throughout the organization. Additionally, better inventory management is key. These are only a few examples of the areas we are targeting to improve Westport’s overall profitability.

Please note also that lost HPDI revenues will be partially offset by the gradual ramp of large LPG system supply contracts with an anticipated revenue contribution of €255 million over the next four years.

Perhaps most disappointingly, management rebuffed or sidestepped basically all analyst questions regarding more color on the company’s anticipated near- and medium-term financial performance, anticipated impact of the HPDI joint venture and capex expectations.

However, management warned of an approximately six-month delay to the company’s new manufacturing operations in China:

Regarding China, facility construction is underway and capital investment for the assembly lines and other equipment is in progress. Recently, the regulations associated with hydrogen components have changed in China, resulting in a slightly longer timeline to complete the certification of the initial products we plan to launch in China. We therefore anticipate production will commence in the second quarter of 2025, rather than later in 2024 as originally expected.

In sum, new CEO Dan Sceli’s performance on the call left much to be desired as he seemed largely unprepared for the questions-and-answers session. However, after just two months at the helm there should be room for improvement going forward.

Bottom Line

Westport Fuel Systems delivered another set of uninspiring quarterly results with meaningful cash burn and inventory write-downs resulting in profitability falling short of consensus expectations.

On the flip side, the company managed to shore up liquidity and signed definitive agreements with Volvo regarding the establishment of a new HPDI joint venture.

The new joint venture should materially benefit the company’s liquidity, margins and cash flows going forward. Consequently, I would expect liquidity to remain sufficient until at least 2026.

However, management declined to quantify the impact on the company’s financial results going forward and sidestepped or outright rebuffed a large number of analyst questions on the conference call, which wasn’t exactly suited to instill confidence in the company’s ability to execute under new leadership.

At this point, I don’t see any reason to initiate or add to existing positions, but given the apparent benefits from the upcoming HPDI joint venture with Volvo, I am reiterating my “Hold” rating on the shares.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

[ad_2]

Source link