[ad_1]

Kwarkot

Investment Thesis

The FTSE All Equity REIT saw its total returns drop by 4.97 percent in December, bringing its yearly loss to -24.95 percent. That marked the worst year for publicly traded real estate investment trusts (“REITs”) since the Great Financial Crisis of 2008, when total returns dropped by almost 40 percent.

However, despite this awful performance last year, REIT W. P. Carey Inc. (NYSE:WPC) recorded what I would term a good performance, gaining about 8% in share prices and outperforming the market by a margin of about 17%. Additionally, the company’s financial performance proved its resilience to the harsh economic climate by registering a YoY revenue growth of more than 10%, solid cash flow performance, and attractive profitability. I attribute the company’s good performance to its diversified business model.

W. P. Carey Inc. has a solid balance sheet that is relatively low in debt ($7.78B, or 0.4X its market cap of $17.78) and has $188.99M in cash on hand. The firm’s robust balance sheet should serve as a safety net during economic downturns. I am optimistic about this stock due to the industry’s bright future and its solid financial position.

2023 REIT Outlook: Optimism for the Future

The U.S. economy likely will continue to see uneven economic growth, declining job gains, rising inflation, and increasing interest rates in 2023. These factors increased economic uncertainty. The Bloomberg consensus forecast survey projected a U.S. recession within 12 months at 62.5% in November 2022, up from 15% at the start of the year.

At the end of 2022, property fundamentals were still strong, but there were signs of weakness heading into 2023. Occupancy rates for industrial, retail, and apartment buildings remained higher than before the pandemic. Office occupancy fell roughly 3% in 2019. Industrial, retail, and apartment rent growth remained strong in the fourth quarter, while office rent growth remained positive. Interest rates and debt costs are slowing commercial real estate transactions. The third quarter of 2022 saw the lowest REIT capital raising since 2009 due to high rates and low valuations.

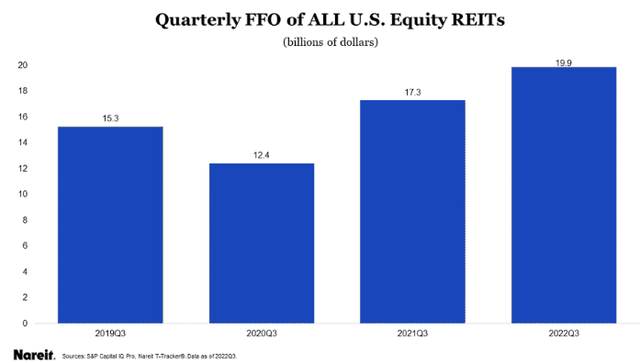

From a business viewpoint, equity REITs have proven to be fairly resilient despite economic headwinds and depressed valuations. REITs are well-positioned for continuing economic uncertainties in 2023. In the third quarter of 2022, the Nareit T-Tracker showed strong growth in FFO, NOI, and same-store NOI. Thanks to solid operational performance and balance sheets, REITs can handle economic and market unpredictability in 2023.

Nareit

When considering the forecasts for the REITs industry, I believe that WPC’s strong balance sheet will be crucial to its future success.

The Business Model

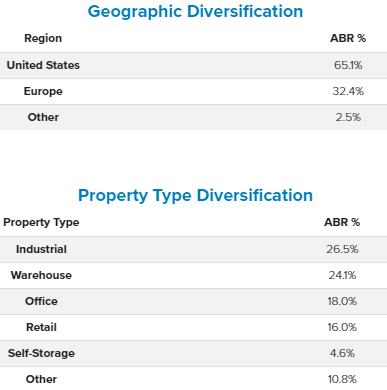

I think WPC’s success can be mainly attributed to the company’s incredibly diverse portfolio of investments. Its diversification is both geographical and property-wise. Regarding geography, the company has a presence in the USA and Europe, accounting for more than 97% of its portfolio. Further, they have diversified to different properties, which will help meet the diversity in the real estate industry.

wpcarey

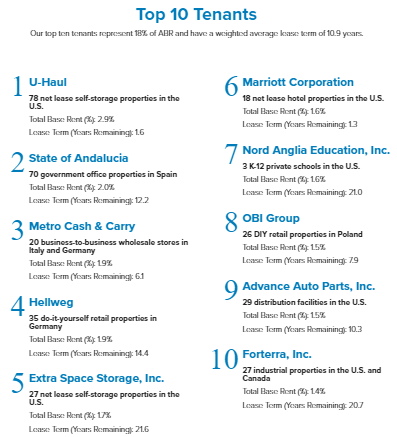

I am pleased that the company’s top 10 tenants are all locked into long-term leases, as this bodes well for the company’s long-term financial security thanks to the diversity of its customer base.

wpcarey

The company’s diversity, in my opinion, will provide them an edge in the market because of the following advantages:

- Addressing the Foreign Exchange Problem: Most senior executives know that exchange rates can affect the dollar value of their foreign currency assets and liabilities. However, few realize that exchange rates can seriously impact operating profit. Since the company can earn in various currencies depending on its location, it can pay for its expenses in regions with weaker currencies with money it earns from regions with stronger currencies, eliminating a significant source of potential loss.

- Expanding clientele and meeting diverse needs: WPC’s ability to develop its property in a geographically diverse position allows it to meet the needs of a broader range of customers, allowing it to capitalize on the market to a greater extent than it would have been able to do with a more limited product line.

- Exploiting different economies: Since economies in other regions perform differently at various points, a business operating in multiple regions can take advantage of the best-performing economies while being protected against the worst. I think this will allow the company’s performance to remain stable.

Profitability

Profits have increased alongside revenue as the company’s diversified portfolio has led to a 10% year-over-year increase in sales. WPC is one of the best options for investments focused on making a profit because their profit margins are high compared to the industry medians. The company has a gross profit margin of 95.29%, an EBIT margin of 52.03%, and a net income margin of 34.59%. All these figures are way above the industry medians of 67.39%, 23.425, and 17%, respectively.

Cash Flows

W. P. Carey Inc.’s cash flow generation has been reliable since 2018. Its cash flows from operations have been rising steadily since 2018, with a dip in 2020 due to covid-related problems, but have since recovered. The nearly two-fold increase in the company’s cash flows from operations from 2018’s $509.2M to $1 billion on a TTM basis is impressive. Their leveraged CFC balance of $804.67M is also highly appealing. Overall, the company’s ability to generate cash flows is reflected in its free cash flow per share, which currently stands at $5.17. The company’s ability to generate sufficient cash flow to meet its operating needs and surplus cash for use in capital expenditures, debt repayment, and shareholder distributions is demonstrated by its solid cash flow history.

Dividends

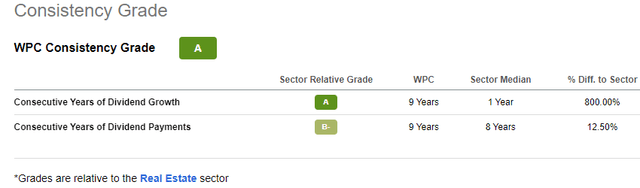

When it comes to dividends, W. P. Carey Inc. is a reliable payer. It has a 9-year track record of dividend growth. In contrast, the median in the business is only one year, and WPC has a 9-year track record of uninterrupted dividend payments, while the median in the industry is eight years. As a result, they have earned a stellar reputation among their industry rivals and are consistently able to distribute dividends to their shareholders.

Seeking Alpha

W. P. Carey Inc.’s average dividend yield over the past four years is 5.50%, which is higher than its competitors. This company’s dividend distribution is significantly better than its peers.

Conclusion

With W. P. Carey Inc.’s diversified business model, future success looks almost assured, making the company a good prospect. Its solid balance sheet should act as a buffer against tough economic times. Additionally, they have attractive and consistent cashflows, which bode well for the company’s smooth operational performance.

With its dividend policy looking more attractive and consistent than peers, this makes W. P. Carey Inc. one of the best dividend payers in the industry. For these reasons, I rate W. P. Carey Inc. company a buy.

[ad_2]

Source link