[ad_1]

NanoStockk

Investment Thesis

UiPath (NYSE:PATH) has been out of favor with investors from the moment of its IPO until last October. In essence, investors didn’t buy into its vision that its technology to avoid the duplication of menial tasks was all that alluring.

That being said, what’s compelling here is that, unlike many other disruptive tech companies, it doesn’t suffer from a lack of profitability.

Indeed, not only is PATH already significantly profitable but its guidance for the upcoming fiscal year looks even more enticing.

The issue here boils down to the question of what sort of multiple will investors be willing to pay for its middle-of-the-road growth rates.

However, before we answer that question in full and why I’m bullish on its prospect from this point, let’s first get some context.

What’s Happened in the Past Year?

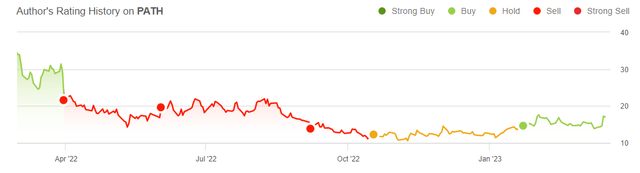

Author’s rating, PATH

The good news for prospective shareholders is that the bottom on this stock appears to be put in around October of last year. Yes, the stock is down massively since its IPO, and yes, it’s difficult to envision this stock returning to the high $70s per share, thereby increasing by 5x from the current prices.

But at the same time, I believe that anyone that wanted out of this name has by now long ago sold it.

Why UiPath? Why Now?

Today, PATH is a Robotic Process Automation (”RPA”) company. But the company is broadening its products to process mining, intelligent document processing, API integration, and low-code app development. Meaning that the business can grow its customer base by not only expanding what can be automated but also who can develop automation.

This is what PATH stated on its earnings call:

A great example is Swisscom, which, after successfully implementing RPA and Test Suite in their finance, IT, HR and Customer Service departments, is rolling out automation across their entire organization to improve customer service, attract and retain talent, enhance operational efficiency and launch new growth engines in B2B with automation-as-a-service.

All that said, the one blemish in its results is PATH’s dollar-based net retention rates (”DBNRR”). In last year’s fiscal Q4 2022, DBNRR was 145%. Then, this figure dropped to 138% at the start of this fiscal year. Then, in fiscal Q3 2023, the figure dropped again to 126%. And this latest set of results saw its DBNRR reach 123%.

For long-term buy-and-hold investors, I believe that keeping an eye on this DBNRR figure is important.

Revenue Growth Rates Will Reaccelerate

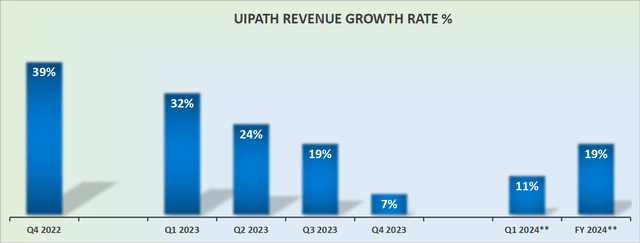

PATH revenue growth rates

Further, the graphic above is a reminder of just how challenging fiscal 2023 has been for shareholders. PATH started fiscal 2023 by reporting more than 30% y/y growth rates, and by the time the year was finished, PATH’s topline was eking out mid-single-digit growth rates. Hardly a revenue growth rate that is commensurate with its high-tech narrative.

Nevertheless, the silver lining here is that as we look ahead to fiscal 2024, the comparables will be relatively easy, at least in the early parts of fiscal 2024.

Profitability Profile Set to Pick Up Momentum

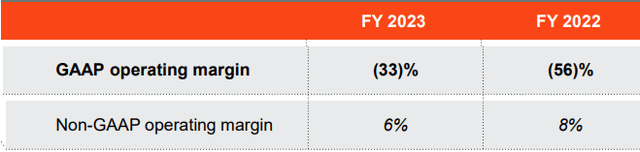

PATH fiscal Q4 2023

Fiscal 2023 ended with non-GAAP operating margins of 6% compared with 8% for the year. But what got investors to take notice and become bullish on PATH’s potential is that its guidance for fiscal 2024 points to approximately 10% non-GAAP operating margins.

That would be a significant improvement in profitability compared with any point in the past 3 years.

Furthermore, keep in mind that PATH’s balance sheet holds no debt and that 18% of its market cap is made up of cash and equivalents.

Put another way, given that PATH is already pointing towards significant non-GAAP profitability and clearly isn’t burning through free cash flows in fiscal 2024, the business is not only already self-sustainable but its balance sheet isn’t causing it any impediment of any sort.

Hence, from this point, it’s largely a question of what sort of multiple is justified.

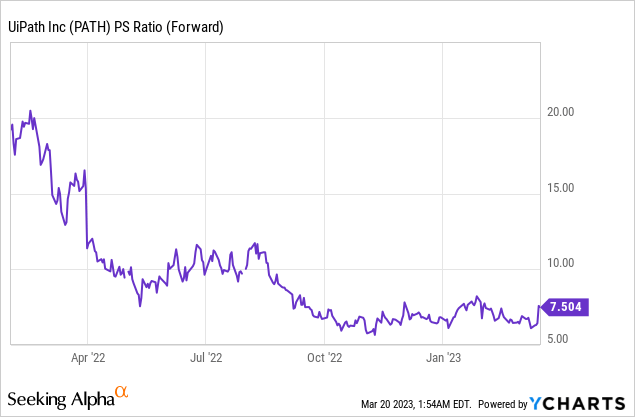

PATH Stock Valuation – 77x Forward Non-GAAP Operating Profits

As you can see above, PATH’s multiple has already massively collapsed. This time last year, investors were more than willing to pay 20x forward sales. And today, investors are being asked to pay less than half this multiple.

What’s more, as already discussed, today PATH’s underlying profitability is pointing to the year ahead towards a significant improvement.

The Bottom Line

In conclusion, PATH’s prospects point to an acceleration in the back half of fiscal 2024 (calendar 2023).

Meanwhile, I make the case that PATH’s valuation has already fully derisked, and not much hope is now priced into these shares.

[ad_2]

Source link