JHVEPhoto/iStock Editorial via Getty Images

Stifel (NYSE:SF) is expected to bounce back significantly with a strong rebound in the stock price following the current market turmoil, as its current revenue mix is incredibly healthy to withstand the economic changes and continue growing the top line over the next several years. Investors are focusing on the wrong thing and not looking at the big picture, where Stifel has been able to increase revenue from asset management fees during a bear market.

Introduction

Stifel Financial Corp recently published their quarterly report for June 2022. Despite the shifting climate, rising costs, declining stock market, and drop in global M&A volumes, the company managed to maintain revenue over the past year, following an outstanding year for investment banking.

While revenue did drop almost -3% over the past year, it is a lot better than expected given the group’s exposure to M&A and the subsequent drop in M&A volumes over the past year.

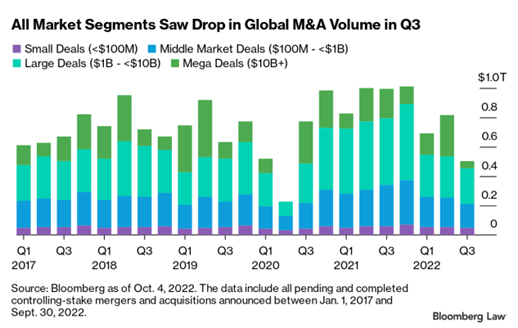

Bloomberg

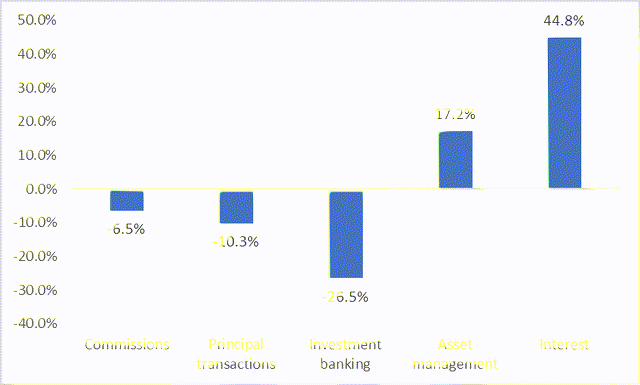

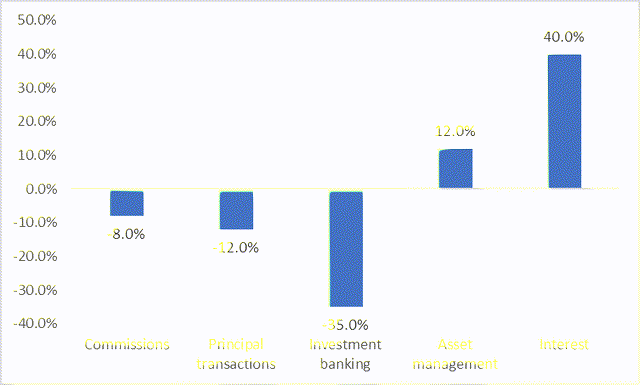

The market has been choppy, and M&A volumes are expected to continue to decline over the short term (although private equity still has a lot of dry powder and will no doubt take advantage of the discounted opportunities). This has led to a decline in Investment Banking revenues for Stifel, a drop of 27%.

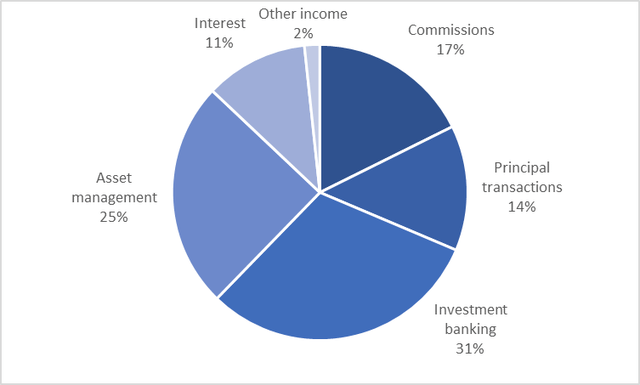

This is on top of a decline in other revenues, such as Commissions (-6.5%) and Principal Transactions (-10%). As expected, the revenue segment that has grown was interest income, from the consumer division, given the rise in the base rate. Unfortunately, Stifel is not much of a consumer banking powerhouse, and the interest income segment only accounts for 17% of revenue (previously 12%), so one cannot rely on this segment to make a considerable impact on the overall top-line growth of the company.

However, the last division of Stifel, one that you would expect revenues to drop given its correlation with the stock market, is Asset Management fees. These are revenues generated by investment advisory services provided for private clients and institutional investors and are subject to overall market performance. As stated, there tends to be a positive correlation, so rising markets have historically had a positive impact on Asset Management fees.

The company has had success in advisor recruiting and growing the interest-earning assets within the Asset Management division. The private client group is now fairly significant, with over 2,300 financial advisors and over 400 regional offices. The increase in revenue is due to the recent rebranding of their independent broker-dealer subsidiary, and the heavy push of advisor acquisition, where 121 advisors were added in 2021 alone.

This has allowed Stifel to grow its Asset Management revenue by almost 20% when the market (S&P 500) has declined by 20%.

Google

Financial Performance

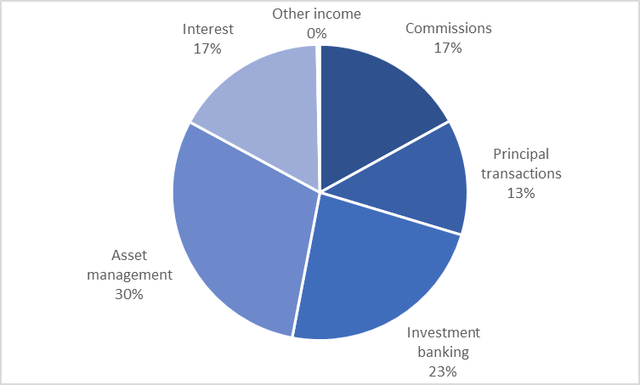

This increase in Asset Management revenue has led to the division accounting for 30% of total group revenue.

June 2021

10Q company accounts

June 2022

10Q company accounts

Assuming a base case that the stock market continues its decline, we could see SF generate positive revenue growth over the next year, even though M&A volumes will be muted. If we assume a scenario that each division has the same % growth compared to the previous period (so Investment Banking fees falling further, Asset Management fees growing), and using the new portfolio of fee generation, Asset Management revenue could grow to almost $800m, accounting for almost 34% of total revenues, and leading to an increase in overall revenues (although this was helped by Interest Income).

2023 FY revenue growth forecast by division.

10Q

These growth rates give a 2023 FY revenue figure of $2.336b, which is almost 4% higher than the 2022 figure and 1% higher than 2021.

Even if we were to taper these growth rates to a more conservative estimate (see below), where banking fees fall even further, and Asset Management fees and Interest income do not grow as much, we obtain a revenue figure of $2.227b, only -1.1% less than 2021’s figure. This is still an excellent result for a bear market (bear in mind this scenario is if the stock market continues to fall further)

10Q

Stifel has had recent success in growing its client base.

Now, the interesting thing here is if the stock market stops falling. As stated previously, rising stock markets have historically had a positive impact on investment advisory fees given that account balances not only rise in value, but investors tend to allocate more money as they have confidence. Therefore this recent growth in AM fees has increased the size of client accounts within the Stifel portfolio, at a point where the stock market is at a low. A rebound now with robust growth would amplify the returns significantly for Stifel.

Risks

One risk would be the continuation of the bear market and a steep fall in valuations leading to a deep recession. No doubt investors will start to pull their money out of Stifel’s advisory portfolios as they become more anxious, not only leading to a drop in the standard fixed rate of advisory fees as well as the potential for performance fees, but a mass withdrawal of investor funds from the Stifel portfolio could lead to fire sales, and therefore losses on investments.

A second risk could be if Stifel were to not continue its success in acquiring new client assets, as there are signs that they are still focusing on expanding its Investment Banking division, given the recent acquisition of AXCIT Capital Partners (a corporate finance advisory firm). This acquisition shows that despite the gloomy market outlook and the expected drop in M&A volumes, Stifel continues to build their Investment Banking arm. While this could be a good long-term play when M&A volumes bounce back (if the acquisition were at a fair price), it is not great for the short term.

Conclusion

In conclusion, I believe that investors are not looking at the right picture with Stifel, there is too much emphasis and focus on the performance of the Transaction related divisions (which is fair given the historical position of Stifel and the corporate strategy revolving around M&A), and not enough focus being put on the Asset Management division performance (which also has a more stable revenue stream). Asset Management has taken over Investment Banking to be Stifel’s largest division for revenue generation and will continue to grow with some positive headwinds coming it’s way. The stock price has reflected the drop in revenues from Investment Banking when in reality it should also take into account the revenues from Asset Management. Therefore, the stock price is undervalued, and we can expect a rebound of around 30% to get back to being flat on the year. However, given consumer confidence and market performance, we would have to wait for the bear market to finish its course before the rebound happens. But when it does, it will be significant given Stifel’s head start.

/cdn.vox-cdn.com/uploads/chorus_asset/file/24020048/226270_iPHONE_14_PHO_akrales_0797.jpg "Apple confirms the iPhone is getting USB-C, but isn’t happy about the reason why")

{kind=link}