[ad_1]

ollo

Rexford Industrial Realty, Inc (NYSE:REXR) owns a portfolio of irreplaceable industrial properties within the infill area of Southern California, a severely supply-constrained market the place common rents are considerably increased than the nationwide common.

Their focus on this market has produced market-leading returns over the previous a number of years, with complete shareholder returns of 145% since 2017 and a three-year compound annual development price (“CAGR”) of 34% and 20% in consolidated web working revenue (“NOI”) and funds from operations (“FFO”), respectively.

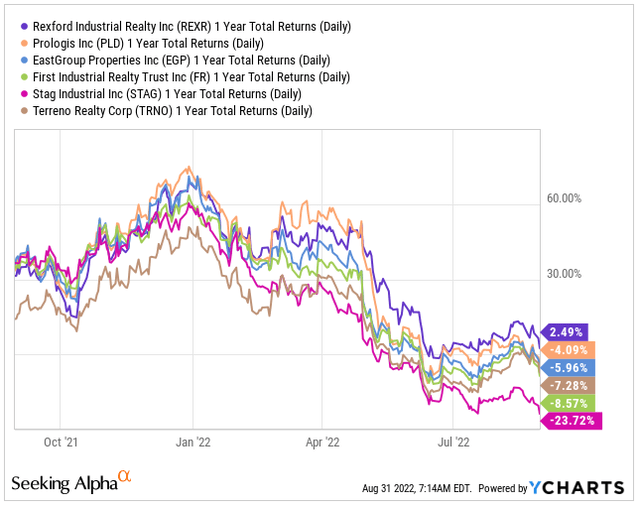

REXR can also be main the peer set over the previous one yr, with a return of about 2.5%, the one title within the optimistic.

YCharts – Complete 1-YR Returns of REXR In contrast To Peer Set

Regardless of sturdy underlying fundamentals, shares are at present buying and selling on the decrease finish of their 52-week vary. Whereas the present pricing a number of of 32x ahead FFO is a premium relative to friends, it’s justified, given the dynamics of their major working location. And when thought of towards present dividend development charges, one might moderately verify a considerably increased intrinsic share value. For long-term traders, REXR is one industrial REIT that’s actually price consideration following its YTD pullback of over 20%.

Focused Focus On Nation’s Largest Industrial Market

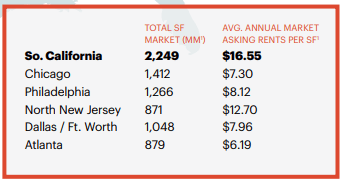

A core aggressive benefit of REXR is their focused deal with Southern California, which is the biggest U.S. industrial market and the fourth largest on this planet, behind solely China and Japan outdoors of the U.S. Inside the U.S, the worth of the market is sort of as massive as the subsequent 5 largest markets mixed, with common annual base rents (“ABR”) of over $16 per sq. foot (“psf”) versus sub $10/psf in 4 out of the subsequent 5 largest markets.

July 2022 Investor Presentation – Comparability of Common Base Rents Throughout The Nation’s High Markets

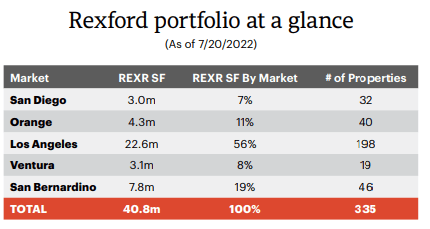

As of mid-July 2022, REXR owned 335 properties in infill areas concentrated in Los Angeles County. These infill markets are characterised as high-barrier-to-entry markets with a shortage of vacant or developable land and excessive concentrations of individuals and financial exercise.

As well as, these markets have skilled a web discount in provide over time as extra industrial property is transformed to non-industrial makes use of. Compounding the availability points is extra industrial demand that continues to exceed development deliveries, which are sometimes set again as a result of excessive land and redevelopment prices.

Q2FY22 Investor Presentation – Breakout of Particular person Working Markets Inside Southern California

The favorable provide/demand dynamics within the area allows REXR to command considerably increased ABR than their friends. By means of Q2, for instance, REXR’s ABR/psf was $12.33, greater than $5/psf increased than their peer set.

Persevering with depth in tenant demand can also be contributing to document excessive leasing spreads, which have been 83% and 62% on a GAAP and money foundation, respectively, within the present quarter. This builds atop respective spreads of 71% and 57% within the prior quarter.

A Tenant Base With Few Options For Spacing Wants

Tenant demand continues to be pushed by a variety of sectors. However within the final a number of quarters, the corporate has seen a notable enhance in demand from E-commerce-oriented tenants. Whereas there was a pullback in general E-commerce because of the receding of the pandemic, the sector nonetheless enjoys secular tailwinds.

Final-mile distribution methods within the nation’s largest market can also be driving incremental demand for REXR’s infill property areas. This positions them strongly to proceed serving their present tenant base, whereas additionally attracting new E-commerce-oriented and conventional distribution demand.

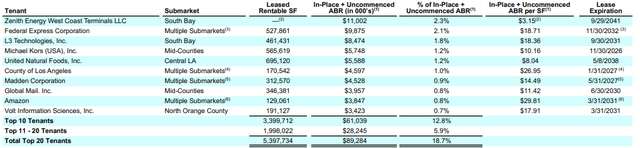

REXR’s general tenant base is broad, drawn from a number of industries. Not solely do the highest 20 signify lower than 20% of ABR, which is indicative of a extremely various portfolio, however no single tenant accounted for over 2.5% of ABR. This minimizes the corporate’s publicity to tenant default threat and earnings volatility.

Q2FY22 Investor Presentation – Abstract of High 20 Tenants

Any Downturn Would Be Confronted From A Place Of Energy

Within the present inflationary surroundings, one can moderately query whether or not their tenant base can proceed absorbing 70% leasing spreads, particularly with the present drag being created by their transportation prices. For a distribution-oriented tenant, nonetheless, lease prices are a small a part of their general economics. Moreover, by design, REXR’s properties are positioned nearer to each the tip factors of distribution and the ports. This allows their tenants to search out efficiencies on the bigger transportation expense base that offsets a lot of the hit from increased rents.

One other legitimate concern is the influence of a downturn on occupancy and the credit score high quality of their portfolio. With same-property common occupancy operating at traditionally excessive ranges at 99%, that is unlikely to be a problem. On the earnings name, administration alluded to the good monetary disaster within the late 2000s as some extent of reference.

Then, there was a big demand shock the place order flows to a lot of their tenants got here to a halt. And going into the disaster, emptiness stood at between 2-4%. But, regardless of the demand shock, the worst it ever bought was to 3-5.5%. That contrasts considerably with the present interval, the place emptiness is at 0.8% and the first points stem from supply-side forces versus demand. As such, the area and the portfolio are significantly better geared up to climate any near-medium downturn, ought to one happen.

Relating to credit score high quality, the current impact of the pandemic is an efficient instance. Regardless of being given the unilateral proper to not pay lease firstly of the COVID-19 pandemic, REXR skilled basically no influence to collections as their tenants continued to pay. As well as, given present provide dynamics, REXR could be extra selective in selecting the tenants that they’re placing into their areas. This enables them to push out underperforming tenants and convey within the increased high quality ones.

Present unhealthy debt reserves present additional assist of their tenant high quality. Over the previous 12 months, for instance, there have been no unhealthy money owed as a share of revenues. Trying forward, the corporate is projecting 10 foundation factors (“bps”) for full yr 2022, however that’s nonetheless under the 40 to 50bps reported previous to COVID-19.

Nonetheless Capitalizing On Inside And Exterior Development Alternatives

Although occupancy is actually maxed out, REXR continues to be posting superior earnings development by way of inside and exterior development methods. Within the present quarter, FFO grew 26% YOY, bringing their five-year FFO/share CAGR to over 15%. YTD, FFO is now up 55% and NOI is up 43%. That is pushed by sturdy leasing spreads and the accretive have an effect on of prior acquisitions.

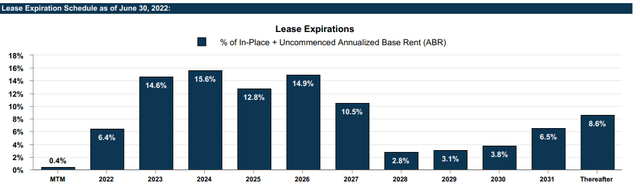

Trying forward, there’s a vital mark-to-market alternative on rental charges for his or her general portfolio, at present estimated at 60% on a money foundation. Upcoming lease expirations also needs to show profitable as these leases are rolled over at favorable spreads.

Q2FY22 Investor Presentation – Lease Expiration Schedule

On the exterior entrance, REXR accomplished 18 acquisitions for a complete of +$600M through the quarter, roughly 72% of which have been value-add investments. Moreover, over 50% of their investments have been both vacant or at below-market rents. On a YTD foundation, the corporate has now acquired 40 properties which might be projected to contribute almost +$40M to NOI in 2022 and +$60M in 2023.

A Supportive Stability Sheet With Ample Capability

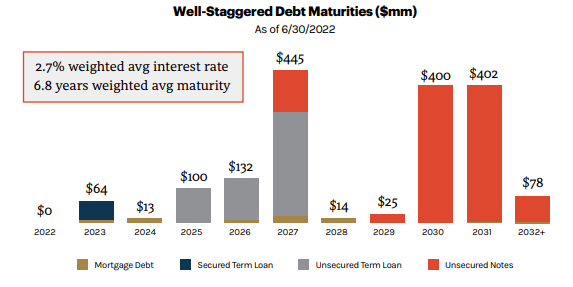

The power to stay energetic individuals available in the market is aided by a stability sheet that features +$1.5B of liquidity and a manageable debt load that accounts for simply 13.5% of their complete enterprise worth. Funding-grade credit score rankings with optimistic outlooks from all three companies supplies additional credibility to their monetary standing. Restricted near-term maturities and a web debt a number of sub 4x additionally supplies adequate flexibility to deploy capital elsewhere.

July 2022 Investor Presentation – Debt Maturity Schedule

A few of this capital has been directed to the dividend payout, which is exhibiting vital development. During the last 5 years, for instance, it has grown at a double-digit CAGR. Although the yield is simply 2% at present pricing ranges, additional development is probably going within the coming durations, given the present payout accounts for lower than 50% of adjusted FFO. There may be, thus, adequate cushion to enact additional will increase within the durations forward.

The Prime Location Warrants A Premium Pricing A number of

REXR trades at a premium to friends as a result of their working focus is concentrated to the infill area of the Southern California market, the nation’s largest industrial market and one of many largest on this planet by itself as an working area. This presence in a severely supply-constrained area the place market rents are considerably increased than the nationwide common has enabled the corporate to outperform their extra diversified peer set.

The elevated degree of focus does invite some considerations, such because the potential impacts of a downturn on the regional economic system and the tenant base. However on this, REXR can be coming into from a place of power, the place emptiness charges are at all-time lows and the present market dynamics are such that REXR could be extremely selective in selecting tenants for his or her properties. That is in stark distinction with prior downturns ensuing from extra demand-side forces.

REXR additionally has a minimally levered stability sheet with ample liquidity. This supplies a further protection mechanism and supplies them with adequate cushion to pounce on any newly obtainable alternatives. Within the present surroundings, they’ve opted for fairness financing, which has weighed on earnings. However regardless of that, their development charges are nonetheless within the higher tiers.

At over 30x ahead FFO, shares aren’t an overt discount on the floor degree. Rising charges additionally disproportionately have an effect on growth-oriented names in additional detailed fashions. Industrial cap charges, nonetheless, have faired higher than different sectors. This could present a extra steady flooring on valuations.

Important dividend development, which is at present trending at a 5-year development price of over 13% should even be thought of. When integrated right into a multi-stage dividend low cost mannequin utilizing an anticipated long-term development price of 6% and a CAPM-derived value of fairness of seven.68%, an estimated share value within the mid-$70s is derived. That might signify over 20% upside from present ranges, along with a steadily rising dividend. For long-term traders, these are returns that ought to clear any risk-premium-related hurdles.

[ad_2]

Source link