[ad_1]

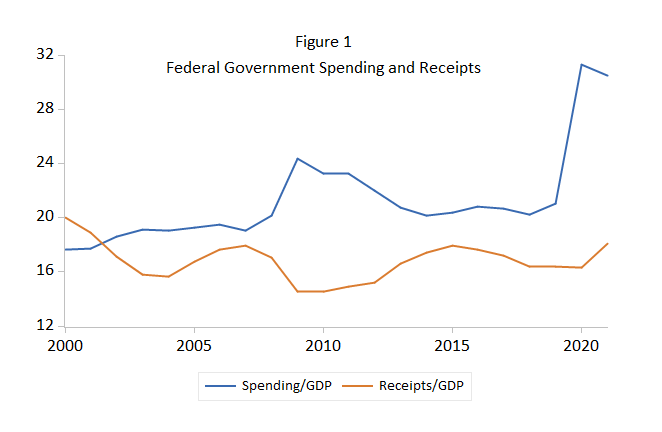

The final couple of years have witnessed extraordinary spending by the federal authorities. It has been fairly the get together. Determine 1 exhibits authorities spending since 2000.

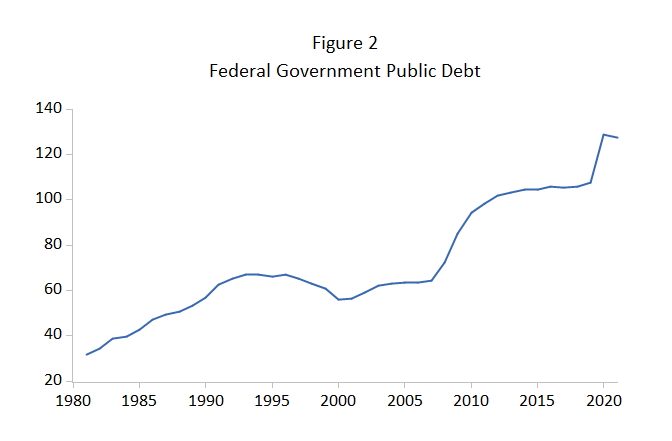

The rise to 30 % of Gross Home Product (GDP) in 2020 stands out. Authorities income, additionally proven in Determine 1, doesn’t soar. Federal authorities income in 2020 and 2021 shouldn’t be significantly increased or decrease than earlier years. The rise in spending was financed by dramatic will increase in debt. Public debt issued by the federal authorities elevated from 107.4 % of GDP on the finish of fiscal yr 2019 to 127.6 % two years later. As Determine 2 exhibits, the rise and the extent are fairly extraordinary.

Rates of interest have been comparatively low just lately, which makes this stage of debt not as onerous because it may very well be. In fiscal yr 2021, the common rate of interest on public debt was 1.8 % per yr. The low stage of rates of interest within the financial system has made it doable for the federal authorities to borrow at traditionally low charges and to have comparatively modest curiosity funds.

There’s each cause to anticipate these low charges to vanish within the subsequent yr or two. In 1981, after the Nice Inflation, the federal authorities paid a median rate of interest over 13 % in 1981 and 1982.

Inflation in the US at present is operating over 7 % per yr; the low stage of present charges is not going to persist. Whether or not the extent of charges will get to 13 % relies upon partially on the Federal Reserve. The Federal Reserve elevated short-term rates of interest at its assembly on March 15. Given the extent of inflation of over 7 % per yr, there’s little doubt that the Fed’s goal rate of interest and the rates of interest paid by the Treasury shall be rising fairly a bit over the subsequent yr and even two if inflation is to be subdued.

The implications of upper rates of interest for the federal authorities’s funds are usually not interesting. Even on the low common rate of interest of 1.8 % per yr, curiosity funds had been 12.7 % of federal authorities income in fiscal yr 2021.

What’s going to occur when common rates of interest on public debt improve? Holders of public debt at present at 1.8 % are shedding on common greater than 5 % of the buying energy of their funds in a yr. A median rate of interest of 5 % on public debt suggests curiosity funds equal to 35 % of present federal authorities income. This rate of interest is hardly a horny proposition although. At an rate of interest of 5 share factors, anybody holding public debt at present inflation charges nonetheless could be shedding 2 % a yr in buying energy. A median rate of interest of seven %, excessive relative to latest rates of interest however not excessive relative to latest inflation charges, would require 50 % of the federal government’s income.

The Federal Reserve is presently dedicated to a sluggish improve in rates of interest. A sluggish tempo carries its personal dangers for controlling inflation. It does suggest, although, that these extraordinary ranges of curiosity funds in comparison with federal authorities income is not going to be reached within the close to time period. Simply later somewhat than sooner.

There’s a dilemma right here although. Elevating rates of interest slowly given the present excessive inflation will let inflation worsen. Elevating rates of interest rapidly has the potential to make the federal authorities’s funds deficit dramatically worse.

Eventually, absent considerably reducing authorities spending or elevating taxes, curiosity funds will overwhelm the federal government’s funds. The scenario would possibly even be termed a sovereign debt disaster as a result of all of the spending, income, deficit and inflation selections are unpalatable.

One believable decision of the dilemma is to extend inflation much more than folks anticipate. This could inflate away the extraordinary debt issued within the final couple of years. In a method, it resolves the dilemma, simply not in a really fascinating method from the perspective of holders of depreciating US {dollars}.

Gerald P. Dwyer

Gerald P. Dwyer is a Professor and BB&T Scholar at Clemson College. From 1997 to 2012, he served as Director of the Heart for Monetary Innovation and Stability and Vice President on the Federal Reserve Financial institution of Atlanta. Dwyer’s analysis has appeared in main economics and finance journals, in addition to publications by the Federal Reserve Banks of Atlanta and St. Louis. He serves on the editorial boards of the Journal of Monetary Stability, Financial Inquiry, and Finance Analysis Letters. He’s a previous President and member of the Govt Committee of the Affiliation of Non-public Enterprise Schooling. He’s additionally a founding member of the Society for Nonlinear Dynamics and Econometrics, a corporation for which he served as President and Treasurer.

Dwyer earned his Ph.D. in Economics on the College of Chicago, his M.A. in Economics on the College of Tennessee, and his B.B.A. in Enterprise, Authorities, and Society on the College of Washington.

[ad_2]

Source link