[ad_1]

Co-produced with “Hidden Alternatives”

onurdongel/iStock by way of Getty Photos

Introduction

Dorchester Minerals, L.P. (NASDAQ:DMLP) is a pure-play crude oil and pure gasoline royalty alternative backed by a shareholder-friendly working construction and administration. This MLP owns mineral rights and web revenue pursuits in key geographies throughout the U.S. and distributes just about all web money from operations to shareholders. On this inflation-ridden financial system, power commodity costs are fueling value hikes throughout the board. Therefore, an funding correlating with commodity costs provides you the final word inflation safety.

DMLP’s distributions are variable primarily based on the amount of hydrocarbons produced and their corresponding value. We count on crude and pure gasoline costs to stay elevated for the foreseeable future, and we challenge even increased yields from DMLP within the upcoming quarters. Briefly, in the event you like commodities, and may tolerate variable distributions, this 10.7% yielding MLP is a unbelievable addition to your revenue portfolio and preferrred for dividend reinvestments.

DMLP is a partnership that points a Schedule Ok-1.

Final Inflation Safety, 10.7% Yield

You’ve got heard of ebook and music royalties. J.Ok. Rowling earned $60 million from the Harry Potter franchise in 2020. Ed Sheeran earns about $5 million yearly from his tune “Form of You.” Warren Buffett compares a royalty to proudly owning a tollbooth; after you make an preliminary funding to construct the toll street, the maintenance is minimal, however the money movement is sort of perpetual. In that spirit, we convey a royalty funding within the power sector.

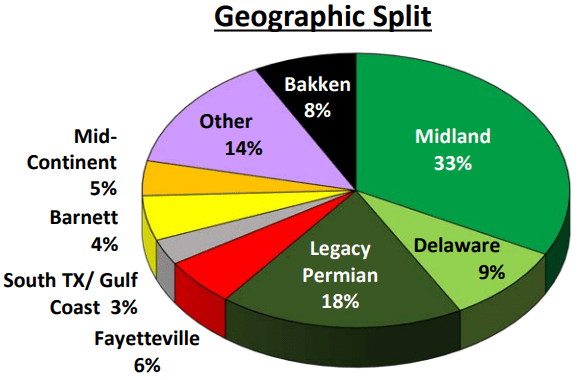

Dorchester Minerals, L.P. owns land and mineral rights in strategically essential oil and gasoline fields situated in 27 states. (Supply: 2021 Investor Presentation)

2021 Investor Presentation

Being the proprietor of royalty and web revenue pursuits, DMLP doesn’t spend cash or sources to discover, produce (upstream), transport (midstream), or course of and rework (downstream) the hydrocarbon output. They merely acquire a payment from E & P firms that drill on their land, and the proceeds differ by the amount extracted and the worth of the commodity. 80% of the partnership’s revenues come from oil gross sales, 10% from pure gasoline, and 10% from different sources. Traders ought to count on DMLP distributions to trace actions within the value of crude oil and pure gasoline.

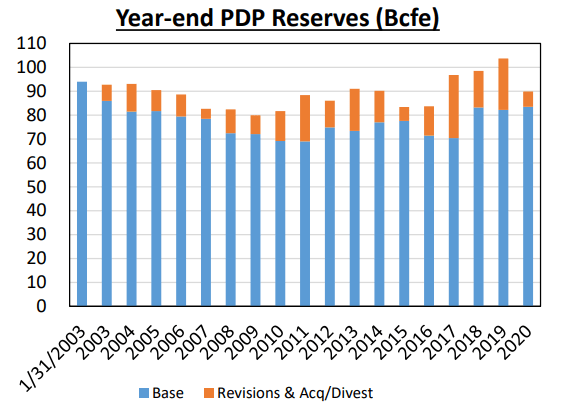

Most frequently, royalties dry out when the reserves are depleted. That is the place DMLP stands out as constructed to final. Administration has been making strategic acquisitions through the years, and present reserves are virtually on the similar degree as when the partnership commenced its operations in 2003. Therefore, DMLP can be a perpetual money cow to your portfolio for many years.

2021 Investor Presentation

So, in case you are involved about increased costs on the pump, we’ve got a method so that you can get your lower via mineral royalties. Maintain studying to know extra.

DMLP is a grasp restricted partnership that points a schedule Ok-1 for tax functions.

Tailwinds For The Sector

Vitality safety is a rising precedence following the struggle between Russia and Ukraine. As power costs are hovering, there are provide considerations for a lot of commodities akin to oil, pure gasoline, and coal. And immediately, Germany is firing up its coal crops and investing in LNG terminals, and main economies are properly wanting their Paris Settlement targets.

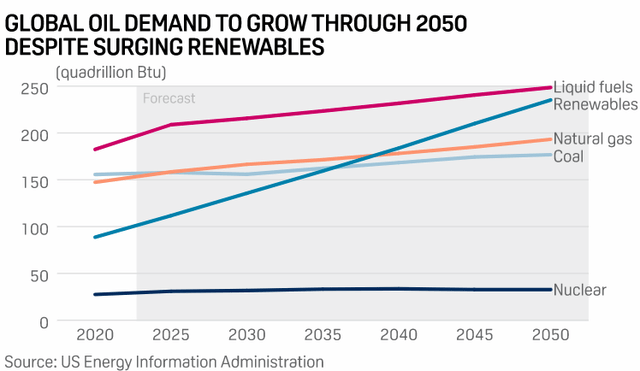

Based on the Worldwide Vitality Company (“IEA”), world crude oil demand is anticipated to extend for many years.

SP World

Booming U.S. shale oil manufacturing performed a major position within the oil value plunge from mid-2014 to early 2016. However up to now 5 years, Huge Oil firms spent little or no CapEx on exploration and manufacturing enhancements. In 2021, upstream funding was 23% beneath pre-pandemic ranges regardless of a powerful demand rebound. The trade succumbed to Wall Road pressures and commenced utilizing earnings for debt paydown, share buybacks, and dividends. There may be large demand for hydrocarbons, however the provide is considerably constrained on account of CapEx hunger.

Oil and gasoline can be round for lots longer than folks suppose, and it’s time to make the most of dirt-cheap valuations within the power sector. Whereas these commodity costs are already elevated, main analysts akin to Moody’s expect these ranges to persist for some time.

“Restrained provide will maintain costs excessive over the subsequent 12-18 months, however with out important basic enhancement in working situations as progress in demand begins to ease” – Elena Nadtotchi, a senior vice chairman at Moody’s

The U.S. is the biggest oil producer, and since hydrocarbon costs are projected to stay elevated for the foreseeable future, we wish to spend money on U.S.-based mineral royalty firms to gather our share from the hovering demand amidst constrained provides. DMLP straight advantages from increased manufacturing and better costs and its construction passes the advantages alongside to traders.

No Debt, Excessive Margin Enterprise

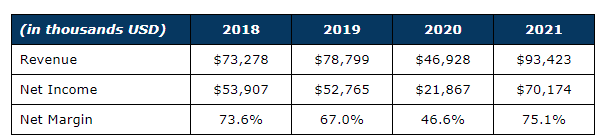

Being an entity designed for royalty revenue, DMLP has comparatively flat prices and bills. You’ll be able to see that the distinction between income and web revenue is constantly $20-$25 million. Any further income has a negligible influence on bills and web margin will increase.

DMLP 10-Ok filings

Vitality is a pretty sector, however many firms within the trade have debt on the upper facet. That is the place we like DMLP’s construction -the agency’s partnership settlement prohibits it from incurring indebtedness in extra of $50,000. Additionally, the partnership doesn’t have a credit score facility, they usually aren’t permitted to incur indebtedness to make acquisitions.

The corporate distributes just about all money generated from working actions. DMLP’s distributions come from the royalty revenue and NPI (web earnings curiosity) from earlier quarters. Therefore, for higher perception into web working money movement and distributions, it’s best to have a look at the mixed information for a couple of years. We will see that the partnership has distributed ~98% of the money from working actions over the previous 4 years.

DMLP 10-Ok filings

Allow us to now take a look at the revenue potential for DMLP.

Excessive Yield Royalty Revenue Alternative

DMLP’s distributions differ primarily based on the manufacturing quantity and value of oil and gasoline. The upper the worth of underlying commodities, the higher the distributions. Equally, when the commodity costs drop, subsequent distributions are smaller. This is without doubt one of the causes DMLP is a perfect candidate for the Dividend Reinvestment Program (‘DRIP’)

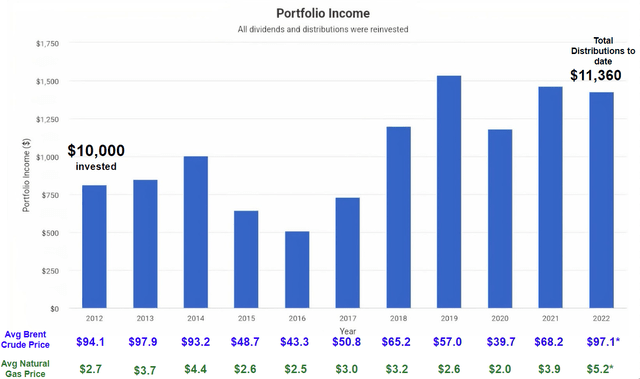

We perceive you’ll ask this query – Is it value shopping for DMLP when commodity costs are at historic excessive ranges? Enable me to reply this by analyzing DMLP’s revenue for the previous ten years. In 2012-13, oil costs have been just like immediately. $10,000 invested in DMLP in 2012 (with dividend reinvestments) would have produced $11,360 in distributions so far, and you’d be sitting on ~21% capital positive aspects. (Supply: PortfolioVisualizer)

PortfolioVisualizer

Word: With out DRIP enabled, this funding would have produced a good-looking 7% yearly.

DMLP’s current distribution of $0.754/share got here from the operations when crude costs have been beneath $90. Resulting from elevated costs up to now two months, we count on its subsequent distribution to be bigger, within the $0.80-$0.85 vary (assuming no acquisitions are made). Annualizing the current distribution gives us with an estimated 10.7% yield.

Shareholder Pleasant by Design

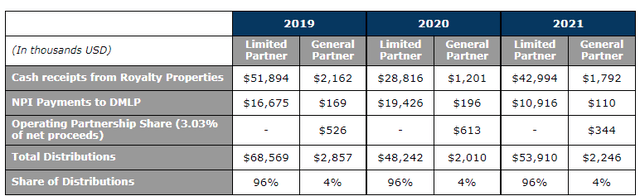

Usually, one of the crucial important drawbacks of an MLP construction is a grasping common companion. Some MLPs have the overall companion drawing an rising portion of the money obtainable for distribution, leaving common traders excessive and dry.

With DMLP, we’ve got a really shareholder-friendly working mannequin. The Common Accomplice is allotted not more than 4% and 1% of the agency’s Royalty Properties’ web revenues and NPI, respectively. Resulting from these fastened percentages, the Common Accomplice doesn’t have any incentive distribution rights (‘IDR’) or different preparations to extend its proportion share of web money generated from DMLP’s working actions. Over the previous three years, the Common Accomplice has acquired not more than 4% of the entire distributable money movement.

DMLP 10-Ok filings

MLP is a shareholder-friendly firm by design and checks virtually each field in Warren Buffett’s standards sheet. Nonetheless, with a market cap shy of $1 billion, this partnership is comparatively tiny for Mr. Buffett’s consideration. That does not need to cease you from amassing good-looking paychecks from this mineral royalty inventory.

Dreamstime

Conclusion

Huge Oil has been compelled to speculate much less and fewer in upstream operations to develop provide for the previous few years. In “Are We Getting into A Commodity Supercycle?” we stated {that a} near-term hydrocarbon value surge was within the playing cards. This Russo-Ukraine struggle grew to become the straw that broke the camel’s again.

The struggle has shined a light-weight on the worldwide dependence on hydrocarbons and the catastrophic influence its scarcity would have on main economies. Regardless of all of the political talks about net-zero, clear power, and renewables, it’s clear that we are going to be more and more depending on crude oil and pure gasoline for the foreseeable future. We count on oil and gasoline costs to stay elevated for a number of years, and DMLP is the revenue methodology of driving the commodity wave.

DMLP is a pure royalty play in crude oil and pure gasoline, with a partnership construction and administration that uphold the distribution stewardship we count on from a top quality funding. This MLP distributes virtually all money from operations to shareholders, fluctuating with the worth of underlying commodities. This structural excessive yielder is a Buffett-quality funding that may pay giant sustainable dividends for years whereas safeguarding your portfolio in opposition to the perils of inflation. Purchase and DRIP, as this money cow is constructed to final.

[ad_2]

Source link