[ad_1]

Shares of Constellation Manufacturers Inc. (NYSE: STZ) stayed in inexperienced territory on Friday. The inventory has gained 8% over the previous 12 months. The brewer ended fiscal 12 months 2022 on a stable notice with better-than-expected outcomes for the fourth quarter of 2022. Right here’s a take a look at the corporate’s expectations for the approaching 12 months:

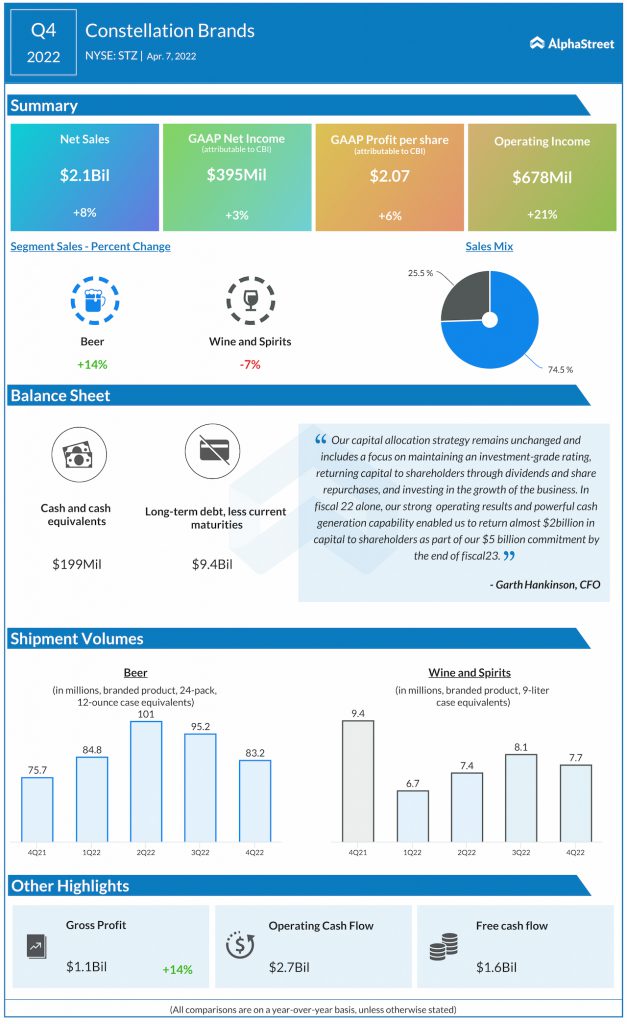

Income and profitability

For the fourth quarter of 2022, Constellation reported web gross sales of $2.1 billion, reflecting a progress of 8% in comparison with the year-ago interval. The highest line exceeded estimates and was pushed by energy within the beer enterprise.

EPS, on a reported foundation, rose 6% to $2.07 whereas comparable EPS jumped 30% to $2.37, beating estimates. For fiscal 12 months 2023, Constellation expects reported EPS to vary between $11.15-11.45 and comparable EPS to vary between $11.20-11.50.

Beer and wine segments

Constellation’s beer enterprise continues to indicate sturdy momentum. Web gross sales rose 14% to $1.56 billion in This autumn. Depletion progress was practically 10%, pushed by energy within the Modelo Especial and Corona Additional manufacturers. Working revenue elevated 21% to $613.6 million.

In FY2023, web gross sales for the beer phase is predicted to develop 7-9% whereas working revenue is estimated to develop 2-4%. Whole beverage alcohol servings per cupboard are anticipated to remain secure, with progress of about 1-2% yearly. Mexican imports are anticipated to be a key driver of good points within the total beer phase. The flavors class is predicted to see vital progress, together with seltzers, flavoured beer, RPG spirits, and flavoured malt drinks, with all classes displaying sturdy future progress prospects.

On its quarterly convention name, the corporate mentioned its Modelo Especial model holds the quantity two place in greenback gross sales within the nation and has significant distribution runway over the medium time period to facilitate mid to excessive single digit whole annual quantity progress within the off-premise channel.

The Corona Additional model has a reasonably excessive family penetration nevertheless it continues to lag behind bigger rivals. Constellation tasks modest progress for this model within the upcoming 12 months. For the Pacifico model, the corporate is forecasting 10-15% whole annual quantity progress within the medium time period from distribution alone.

Inside the Wine and Spirits enterprise, web gross sales decreased 7% year-over-year to $536.8 million in This autumn however on an natural foundation, gross sales grew 5%. Working revenue elevated 6% to $121.8 million. For FY2023, web gross sales in Wine and Spirits are anticipated to say no 1-3% whereas working revenue is predicted to develop 4-6%. Within the coming 12 months, inside this phase, Constellation will deal with continued premiumization, margin enlargement, and progress in DTC channels and the worldwide enterprise.

Capex, money move and shareholder returns

Capital expenditures are anticipated to vary between $1.3-1.4 billion in FY2023. Working money move is estimated to be $2.6-2.8 billion whereas free money move is predicted to be $1.3-1.4 billion. Constellation returned practically $2 billion to shareholders within the type of dividends and share buybacks throughout FY2022 and the corporate plans to repurchase $500 million of its shares in Q1 2023.

Click on right here to learn the total transcript of Constellation Manufacturers’ This autumn 2022 earnings convention name

[ad_2]

Source link