agrobacter/iStock through Getty Pictures

Funding Thought

A robust rebound within the journey trade will profit your complete sector. Since Reserving Holdings Inc. (NASDAQ:BKNG) has a dominant place within the on-line journey trade, we count on it to rebound. We just like the fairness story, however we’d not pay for progress as their aggressive benefit is at the moment robust within the lodging phase and never within the new divisions the corporate is making an attempt to introduce itself to by mergers and acquisitions. It’s all the time good to do not forget that moats should not all the time company-based. Typically an organization has wonderful dominance with one among its merchandise or segments. Nonetheless, it doesn’t suggest they’ll ship the identical ends in different new ventures, even when they’re associated to the agency’s major trade.

We imagine that zero p.c progress is fairly valued on the present market costs, and we’ll all the time search sufficient margin of security. Our Intrinsic valuation is round USD 1,850 per share. We have to guess the execution of the present and future acquisitions, and people executions may be dangerous, and there are nearly no property to again up the worth or any margin of security.

So, we’ll look to go in as soon as we now have a desired margin of security. We’re taking a look at an entry worth near USD1,600 per share and an exit worth of round USD 2,000 per share.

Reserving at a look

Reserving Holdings is the main supplier of on-line journey and associated companies, working in additional than 220 nations and proudly owning a number of fare aggregators and meta-search engines, together with six major manufacturers.

Reserving: Dutch on-line journey company for lodging reservations and different journey merchandise.

Agoda: Singaporean on-line journey company for resorts, trip leases, flights, and airport transfers.

Kayak: American on-line journey company and Meta Search engine.

OpenTable: American on-line restaurant reservations service firm.

Priceline: American on-line journey company for locating low cost charges for travel-related purchases corresponding to airline tickets and lodge stays.

RentalCar: British rental automotive service

Reserving has three vital sources of income:

Company revenues are derived from travel-related transactions and consist nearly completely of journey reservation commissions from lodging, rental vehicles, and airline reservation companies. Reserving invoices the journey service suppliers for his or her commissions after journey is accomplished.

Service provider revenues are derived from transactions that facilitate vacationers’ funds for the companies offered, typically on the time of reserving. Service provider revenues embody journey reservation commissions and transaction internet revenues (i.e., the quantity charged to vacationers much less the quantity owed to journey service suppliers), bank card processing rebates, buyer processing charges, and ancillary charges, together with travel-related insurance coverage revenues.

Promoting and different revenues are derived primarily from A: revenues earned by KAYAK for sending referrals to on-line journey firms (“OTCs”) and journey service suppliers and B: for promoting placements on its platforms and revenues earned by OpenTable for its restaurant reservation companies and subscription charges for restaurant administration companies. The final interval of normalized earnings was 2019, when shoppers booked 845 million room nights of lodging, 77 million rental automotive days, and seven million airplane tickets utilizing web sites owned by Reserving Holdings, reporting a internet earnings of USD 4.8 billion.

Reserving primarily operates within the lodge trade, flights, rental vehicles, and airport taxi companies. In addition they work within the points of interest trade, providing the actions to be carried out in that space.

Reserving got here up with the digitalization of the trade and constructed its platform on which resorts might register themselves and provide their companies, altering the entire dynamics of the trade. Now individuals can search and evaluate totally different resorts by way of costs and high quality of companies, which might now be reached from the opinions individuals have given.

Reserving went into this trade additional and developed a powerful relationship with the shoppers and the resorts with their loyalty and incentive packages. For some small lodge chains, BKNG is now a major supply of earnings, and for resorts, The corporate additionally has incentives and loyalty packages. Some years again, the corporate launched the choice so as to add your fee particulars on the Reserving platform and pay immediately from it for all of the companies the lodge trade has to supply; this has been an enormous success which we will see from the expansion on this income stream (Service provider income). The platform is now such a central piece within the lodge trade that it has gained a stable aggressive benefit on this sector.

Concerning Flight operations, Reserving has began to broaden on this non-accommodation trade with a shocking enhance in airline tickets booked, from 7 million in 2019 to fifteen million in 2021. The problem with this sector is that there is not such a giant pool obtainable like resorts to go looking from. Individuals can simply immediately name the companies and have a number of choices obtainable. Additionally, the opponents on this phase, GoogleFlights, and GotoGate, pose an actual risk as Google has huge sources to broaden and is already most well-liked by many shoppers on this phase.

The primary challenge, in our opinion, is the dearth of fee on the platform for a number of technical causes. So, once you begin reserving a flight, Reserving’s platform will reroute you to different web sites two or 3 times earlier than touchdown you in the end on the airline’s web site, which is an actual deal breaker for most individuals. Additionally, when the taxes are added later, the airline ticket appears much more costly than those initially marketed on the Reserving’s platform. These are the problems that pose an actual risk to Reserving in flight operations.

The airport taxis and rental automotive companies Reserving present does not have a giant pool to select from in comparison with the Lodge trade. So, individuals can shortly name the companies immediately and rent them. It additionally is dependent upon the choice of the shoppers. Individuals these days principally favor companies like Uber, and it is a $46 billion firm whose major service is to offer technique of transport. So, the competitors with native service suppliers and different firms and the decrease margins within the non-accommodations enterprise make us a bit skeptical about the way forward for this phase.

The Points of interest phase is the place you may go on the Reserving’s platform, e book the actions you need, and pay immediately on the platform. This can be a phase the place Reserving has a wonderful progress alternative. GetYourGuide has proven spectacular progress on this part. We count on the corporate to develop extra on this phase.

Lately Reserving has been working to realize Related Journeys, that means they need to have a platform the place an individual can e book the entire journey “Airline tickets, resorts, Airport Taxis, Rental vehicles, Eating places, and different points of interest.” This can be a long-term imaginative and prescient of the administration, and they’re engaged on this, as we will see from their acquisitions.

After being just lately hit by Covid, Restoration within the journey trade from the low factors of covid (as witnessed by SGI World Journey and Leisure Index) and in Reserving is nicely underway. Gross bookings from reservations of room nights, rental automotive days, and the airline made via each of the income streams Company and Service provider for Q1-22 have been a report USD 27 billion & 7% up from Q1-19’s stage.

M&A Dialogue

We all know that Reserving’s progress over time has come from acquisitions.

Reserving is buying firms not only for progress but additionally for increasing into the non-accommodation enterprise; only recently, they’ve spent $3.1 billion on acquisitions in two months for each of the explanations defined above. One co. is Getaroom which is an ideal instance of spending for progress as reserving already has experience on this phase. The opposite is Etraveli which is acquired to broaden into non-accommodation flight operations & obtain the related journey imaginative and prescient.

Since Reserving does not report the valuation of targets acquired and premiums paid or the segmental information to know higher, under is a dialogue of the acquisition’s “Normal Dangers.”

Firms typically get hooked on this type of progress as a result of it is each a simple and quick route of progress, and due to this, firms lose inside efficiencies.

The price of this quick and comparatively simple progress route all the time has an additional worth within the type of premiums paid in acquisitions like Reserving acquired Opentable at 46% premium and Kayak at 29% premium. These are primarily based on the day shares have been purchased by Reserving. Primarily based on the pre-announcement costs, these premiums could be much more.

After firms purchase at such excessive premiums, the query is whether or not there will likely be sufficient synergies. The primary threat is that firms principally have motives to overstate synergies to justify their acquisitions and broaden extra shortly. To realize this, they might pay an excessive amount of at the price of destroying worth.

These synergies come from economies of scale, finest practices, sharing of capabilities and alternatives, and sometimes the stimulating impact of the mix of firms. It takes solely a minimal error in estimating these values to trigger an acquisition effort to stumble.

Different errors contain Threat switch, utilizing your WACC when valuing an acquisition goal, assuming your individual enterprise and monetary threat reasonably than the goal’s, and undermining or overstating the goal’s threat profile. One other challenge with exterior progress is the supply of funds. Typically the price of fairness is so excessive, and debt may include too many covenants, crippling your decision-making. So, in situations like these rising via acquisitions won’t be attainable.

The problem is that we do not know for positive that the cash spent on acquisitions can create worth with synergies as a result of we haven’t any proof from the corporate that that is occurring and can proceed to occur.

Then again, it’s price mentioning that the acquisition of Reserving.com by Priceline group has been one of the vital profitable and value-creating acquisitions. Additionally, the acquisitions of Opentable and Kayak at excessive premiums talked about that regardless that Reserving failed to extend their working margins considerably, they pushed Reserving to a $15 billion income firm from $9 billion in 5 years, a formidable 67% progress.

One assuring factor is that proper now, Reserving has a share repurchase program occurring. In Q1-22, they bought 486,112 shares for an mixture price of $1.1 billion, implying a per share worth of 2263, and now have a $9.5 billion permitted quantity left for repurchase, which they plan to finish within the coming three years. Though there was a bond covenant in place since October 2020 which restricts the corporate from declaring dividends and repurchasing shares earlier than attaining sure efficiency obligations, Reserving has been reaching these. It has been in a position to full share repurchases to date. So, we do not take into account this a difficulty going ahead both.

Monetary Evaluation & Valuation Angle

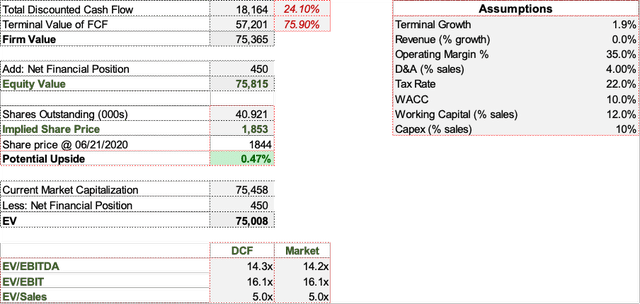

Comps. primarily based valuation is just not appropriate for this inventory as it is a main Firm in its trade and cannot be in comparison with the second largest firm Airbnb due to totally different enterprise fashions, income streams, and many others. In comparison with the third most distinguished firm within the on-line journey trade, Journey.com has a market Cap diff of $56 billion, which tells so much in regards to the place of reserving in its sector and the inappropriateness of comps. Primarily based valuation.

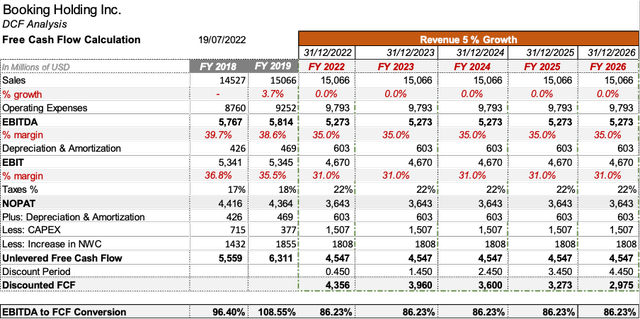

Initially, we needed to do a DCF for all the segments individually by which reserving is working to have a greater understanding as a result of, as defined, it does not have a moat in all segments, so we as worth traders do not need to pay for progress in segments the place it does not have a moat, Additionally every phase has its dynamics, totally different opponents, totally different margins, totally different progress charges however we have been unable to search out the required information as Reserving is just not reporting its segmental info.

So, to take care of all these points, we now have approached this valuation utilizing a 5-year single-stage DCF Mannequin with 0% progress within the subsequent 5 years to know the inventory worth with no growth implied. We are able to assess totally different situations utilizing sensitivity evaluation. We’re utilizing 1.9% terminal progress.

Reserving has spent $873 million yearly on acquisitions for the previous ten years. Contemplating this, our expectations for future capital expenditures, together with upkeep, are at 10% of revenues per 12 months.

One of many income streams of Reserving is service provider revenues, by which money fee is acquired upfront by the corporate. These advance funds assist them handle their working capital, so that they have had adverse working capital necessities for the final 12 years, positively impacting free money flows. Contemplating the common Internet working price of the normalized intervals earlier than 2020, we’re utilizing NWC at 12% of the revenues per 12 months.

Reserving has had points sustaining working margins from 42% in 2013 to 35% in 2019, with a mean of 38% in 6 years. They’ve just lately offered their buyer care operations to their long-term companions in assembly seasonal calls for “Majorel” and are actually anticipated to avoid wasting $124 million every year, positively impacting margins.

With the rise of non-accommodation companies like flight operations as a share of complete commerce and the truth that they’ve decrease margins on this phase, working margins are anticipated to be negatively affected. Additionally, to the extent that Reserving is more and more processing extra transactions on a service provider foundation, they incur a larger stage of merchant-related bills, negatively affecting the margins.

Contemplating the working margins dialogue and being conservative, we’re utilizing an working margin of 35%. Given an inflationary Macro Atmosphere, enhance in rates of interest, and present market situations, we’re utilizing a WACC of 10%, D&A of 4% of income, and a tax charge of twenty-two%.

Primarily based on these assumptions, our fairness valuation is within the area of $1,853 per share, giving a possible upside of 0.47%.

DCF desk 1 – BNKG by Antonio Velardo – (Moat Investing) DCF desk 2 – BNKG by Antonio Velardo – (Moat Investing)

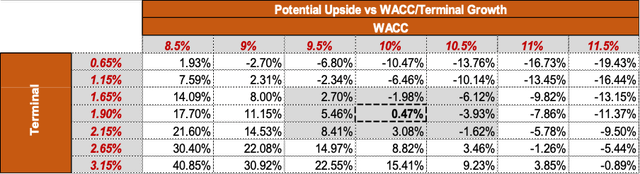

Sensitivity evaluation

Now we have carried out a sensitivity evaluation on the first worth drivers affecting the potential upside. It’s price noting that round 78% of the fairness worth relies on the terminal worth. Thus, our valuation is extraordinarily delicate to WACC and Terminal Progress modifications. Additionally, since we’re in an growing rate of interest surroundings, it’s useful to see the valuation below totally different WACC and terminal progress situations. The next desk reveals a sensitivity evaluation of the potential upside and draw back regarding our intrinsic fairness worth.

Sensitivity evaluation by Antonio Velardo (Moat Investing)

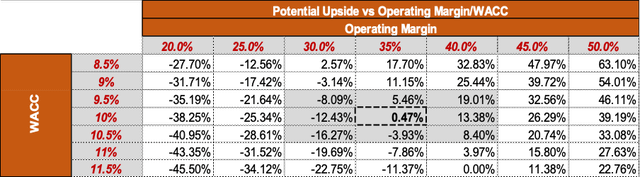

Contemplating our Working Margins dialogue, the desk under reveals the sensitivity evaluation, which is sort of useful in understanding this affect.

Sensitivity evaluation by Antonio Velardo (Moat Investing)

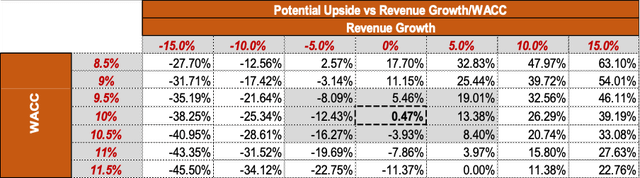

Since we assumed a zero p.c income progress, it is attention-grabbing to see how Reserving performs at totally different income progress charges. Taking a look at common income progress charges of 18% for the previous 5 years earlier than Covid, the sensitivity evaluation under dramatically helps to know the affect income progress could have on the inventory valuation.

Sensitivity evaluation by Antonio Velardo (Moat Investing)

Conclusion

Our Intrinsic valuation primarily based on the above valuation mannequin and assumptions tells us that the inventory is pretty valued at round USD 1,850 per share. We have to guess the execution of the present and future acquisitions, and people executions can typically be dangerous. Additionally, there are nearly no property to again up the worth or any margin of security.

So, we’ll look to go in as soon as we now have a desired margin of security. We’re taking a look at an entry worth near USD1,600 per share and an exit worth of round USD 2,000 per share.

")

")

:max_bytes(150000):strip_icc()/Health-GettyImages-1060820524-b9fd002a2a4b4506b7fbeafed4361931.jpg "Common Tongue Conditions in People With HIV")