Printed on August seventeenth, 2022, by Felix Martinez

There isn’t any precise definition for blue chip shares. We outline it as a inventory with at the least ten consecutive years of dividend will increase. We consider a longtime monitor document of annual dividend will increase going again at the least a decade reveals an organization’s skill to generate regular progress and lift its dividend, even in a recession.

In consequence, we really feel that blue chip shares are among the many most secure dividend shares traders can purchase.

With all this in thoughts, we created a listing of 350+ blue-chip shares, which you’ll be able to obtain by clicking under:

Along with the Excel spreadsheet above, we’ll individually overview the highest 50 blue chip shares immediately as ranked utilizing anticipated complete returns from the Positive Evaluation Analysis Database.

This text will analyze Atmos Power (ATO) as a part of the 2022 Blue Chip Shares In Focus sequence.

Enterprise Overview

Atmos Power can hint its beginnings again to 1906, when it was fashioned in Texas. Since then, it has grown organically and thru mergers to a $16.5 billion market capitalization.

The corporate distributes and shops pure fuel in eight states, serves over 3 million clients, and may generate about $3.7 billion in income this yr. Atmos Power manages proprietary pipeline and storage property, together with one in every of Texas’s largest intrastate pure fuel pipeline techniques. Atmos has a 38-year historical past of elevating dividends, placing it in a uncommon firm amongst dividend shares.

Atmos reported third-quarter earnings on August third, 2022, and outcomes have been higher than anticipated on each the highest and backside strains. Earnings-per-share got here to $0.92, which was seven cents forward of estimates. Whole funding earnings soared 34.8% to $816.4 million, beating expectations by $128.67 million.

Consolidated working earnings elevated by $21.2 million to $154.6 million for the third quarter from $133.4 million within the third quarter of 2021.

Distribution working earnings decreased to $66.1 million for the quarter in comparison with $68.1 million within the third quarter of 2021. Key working drivers for this phase embody a internet $30.5 million improve in charges, a $2.6 million improve attributable to internet buyer progress, a $3.3 million improve in consumption, internet of the corporate climate normalization changes (WNA), and a $1.8 million lower in different operation and upkeep expense primarily attributable to decrease dangerous debt expense within the current-year quarter, partially offset by a $13.7 million improve in depreciation and property tax bills and a $5.0 million improve in system upkeep expense.

Pipeline and storage working earnings elevated from $23.3 million to $88.5 million in comparison with $65.3 million for a similar interval of 2021. Key drivers for this phase have been a $21.0 million improve in fee attributable to GRIP filings permitted in 20211 and 2022. Additionally, a $6.1 million lower in system upkeep bills.

Supply: Investor Presentation

Development Prospects

Earnings progress throughout the utility business usually mimics GDP progress. Nevertheless, we count on Atmos Power to proceed outperforming this pattern attributable to its concentrate on capital funding in its regulated operations, a constructive regulatory surroundings in Texas, and inhabitants progress.

In consequence, the corporate ought to profit from stable fee base progress, which can generate annual earnings per share progress in accordance with administration’s 6% – 8% steerage. For instance, the corporate was permitted to extend its charges final yr.

The expansion drivers for Atmos Power are new clients, fee will increase, and aggressive capital expenditures. One good thing about working in a regulated business is that utilities are permitted to boost charges frequently, which just about assures a gentle degree of progress.

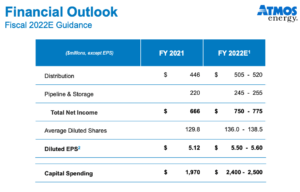

The corporate offered a 2022 outlook. The corporate expects a rise in distribution and complete internet earnings for the yr. Additionally they count on earnings progress from $5.12 per share in 2021 to $5.55 per share in 2022.

Supply: Investor Presentation

Aggressive Benefits & Recession Efficiency

Atmos Power’s principal aggressive benefit is the excessive regulatory hurdles of the utility business. Fuel service is important and important to society. In consequence, the business is very regulated, making it just about inconceivable for a brand new competitor to enter the market. This supplies nice certainty to Atmos Power and its annual earnings.

One other aggressive benefit is the corporate’s steady enterprise mannequin and sound stability sheet, giving it a pretty price of capital. This allows it to fund accretive acquisitions and progress capital expenditures, driving outsized earnings per share progress.

As well as, the utility enterprise mannequin is very recession-resistant. Whereas many firms skilled giant earnings declines in 2008 and 2009, Atmos Power’s earnings per share saved rising. Earnings-per-share in the course of the Nice Recession are proven under:

- 2007 earnings-per-share of $1.91

- 2008 earnings-per-share of $1.99 (4% progress)

- 2009 earnings-per-share of $2.07 (4% progress)

- 2010 earnings-per-share of $2.20 (6% progress)

The corporate nonetheless generated wholesome progress even in the course of the worst financial downturn. This resilience allowed Atmos Power to proceed rising its dividend every year.

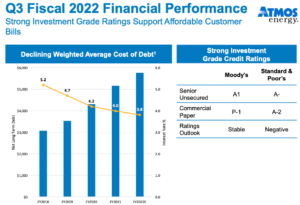

The corporate has a strong stability sheet. The corporate sports activities a debt-to-equity ratio of 0.9 and a long-term debt-to-capital ratio of 33.4. Additionally, the curiosity protection ratio is 10.3, which is an admirable ratio, that means that the corporate covers the curiosity on its debt effectively. The corporate additionally has an A- S&P credit standing. That is an funding grade score.

Supply: Investor Presentation

Valuation & Anticipated Returns

Atmos Power is predicted to earn $5.55 this yr. Based mostly on this, the inventory trades with a price-to-earnings ratio of 21.4. That is above our truthful worth estimate of 19X. The present ratio can also be above the corporate’s ten-year common ratio of 19.6x earnings. Nevertheless, it’s under the five-year common of twenty-two.3x earnings.

Thus, Atmos Power shares seem like overvalued. If the inventory valuation retraces to the truthful worth estimate over the subsequent 5 years, the corresponding a number of contractions will scale back annual returns by 1.9%. This might be a slight headwind for future returns.

The inventory may nonetheless present constructive returns to shareholders by way of earnings progress and dividends. We count on the corporate to develop earnings by 6% per yr over the subsequent 5 years.

As well as, the inventory has a present dividend yield of two.3%. Atmos Power final raised its dividend by 8.8% in November 2021. This marked the thirty eighth yr of dividend progress for Atmos Power. We count on the corporate to develop its dividend this November at a excessive single-digit fee.

General, if we add all this collectively, we are able to count on the corporate to have a 6.4% annual fee of return for the subsequent 5 years.

Closing Ideas

Atmos has robust fundamentals and a protracted monitor document of stable efficiency, however the valuation has risen of late. We’re forecasting complete annual returns of 6.4%, consisting of the present 2.3% yield, 6% earnings-per-share progress, and a slight potential headwind from the valuation. Thus, the inventory earns a maintain score.

The Blue Chips listing shouldn’t be the one option to shortly display for shares that repeatedly pay rising dividends.

Thanks for studying this text. Please ship any suggestions, corrections, or inquiries to [email protected].

{kind=link}