RichLegg/E+ by means of Getty Photos

Funding Thesis

I’ve beforehand found that Wabash Nationwide Firm (NYSE:WNC) is a wonderful agency with rising working margins, capital efficiencies, and returns over the last few years. There could also be nothing to counsel that this has modified. An updated valuation triangulating with 3 utterly totally different value approaches reveals that the stock is cheap. That’s now an funding various.

Background

After I remaining coated WNC in Would possibly 2024, it was shopping for and promoting at USD 23 per share. I had concluded that whereas it was an beautiful agency, there was not adequate margin of safety.

The market worth has since declined to USD 18 per share and I wanted to re-visit my valuation to see whether or not or not there’s now a ample margin of safety. For this analysis, I cowl the interval from 2017 to 2024.

- I used the Jun 2024 LTM outcomes as the 2024 values.

- I start from 2017 to be in line with my Would possibly 2024 analysis.

I’m a long-term value investor holding onto firms for 5 to 6 years. As such I check out long-term developments when analysing valuing firms. On this context, I’ll argue that the enterprise fundamentals of the company haven’t modified significantly since my Would possibly article.

To recap:

- WNC is a primary producer of trailers and liquid transportation strategies that has re-positioned itself as a “chief of linked choices for the transportation, logistics, and distribution industries.”

- This could be a cyclical agency and from 2017 to 2024, revenue grew at 3.8% CAGR. It’s not a high-growth agency. In my earlier article, I quoted 2 market evaluation experiences displaying that the sector is predicted to develop at a low single-digit progress charge.

- I had beforehand assessed the company to be financially sound. I hold this place making an attempt on the current solvency and liquidity positions.

- Beforehand, I concluded that there was an amazing observe file of bettering working and capital efficiencies. Nonetheless on this exchange, I’ll current that not all metrics degree to the equivalent path.

- Returns have been larger than the respective worth of funds indicating that it created shareholders’ value.

I had concluded that WNC was an beautiful agency and I’ve not seen one thing to counsel in some other case.

Valuation narrative

I valued WNC based on the working model illustrated in Chart 1.

Chart 1: Working Income (Author)

Observe to Op Income Profile. I broke down the working earnings into mounted costs and variable costs.

- Fixed worth = SGA, Depreciation & Amortization and Others.

- Variable worth = Worth of Product sales – Depreciation & Amortization.

- Contribution = Earnings – Variable Worth.

- Contribution margin = Contribution/Earnings.

There are 3 key parameters in my valuation model.

- Earnings.

- Contribution margin to suggest working effectivity.

- Capital turnover (revenue/entire capital employed) to suggest capital effectivity.

Earnings

Primarily based on Damodaran, projecting the effectivity of cyclical firms based on the current effectivity can lead to misleading valuations. Fairly it’s further relevant to base the valuation on the effectivity over the cycle.

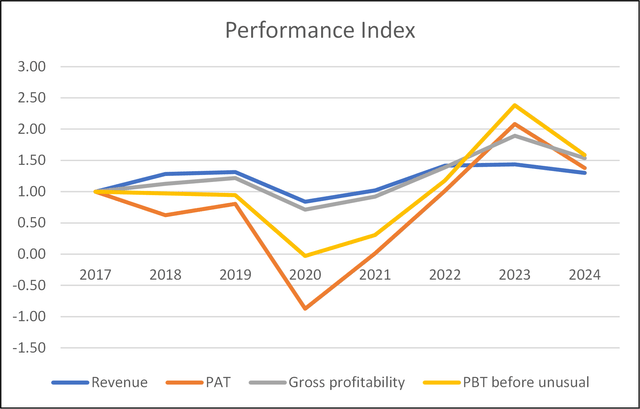

On this context, 2017 to 2024 appears to cowl as a minimum one peak-to-peak cycle. Search recommendation from Chart 2.

In projecting the revenue for my valuation, I assumed that the widespread 2017 to 2024 revenue represents the underside revenue. I moreover assumed that revenue would develop at 4% CAGR in perpetuity.

Chart 2: Effectivity Index (Author)

Attempting on the 2024 effectivity, you may be fearful that it’s a sign of declining fundamentals. I would counter by pointing to its cyclical nature. Furthermore whereas the 2024 outcomes is also lower than these in 2023, they’re nonetheless loads higher than these in 2017.

Furthermore, in my Would possibly article, I had confirmed that in 2022/23 there was a leap inside the Producer Worth Index. This led to an increase inside the widespread unit selling worth in 2023 for WNC. The Producer Worth Index in 2024 is lower than that in 2023. As such you shouldn’t be surprised to see lower revenue in 2024.

My rivalry is that WNC stays to be an beautiful agency. This narrative is in line with the other findings beneath.

Efficiencies

Whereas the company had a observe file of bettering working and capital efficiencies, I assumed that the 2017 to 2024 widespread contribution margin and capital turnover in my current valuation.

I didn’t assemble in any enhancements on account of there have been mixed outcomes after I checked out totally different measurements of working and capital efficiencies.

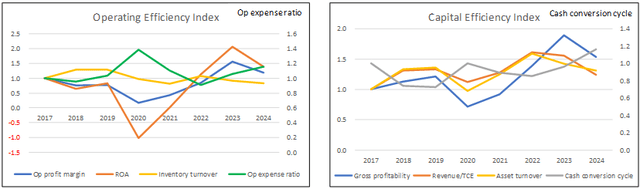

- Working efficiencies. You might even see from the left part of Chart 3 that there have been enhancements inside the working income margin and ROA. Nonetheless inventory turnover declined and the working expense ratio obtained worse.

- Capital efficiencies. Search recommendation from the exact part of Chart 3. There have been bettering developments in gross profitability, capital turnover, and asset turnover. Nonetheless, the cash conversion cycle deteriorated.

From a 2017 to 2024 perspective, there are further bettering developments than deteriorating ones.

Chart 3: Working and Capital Efficiencies (Author)

Progress

Progress should be funded and one metric for that’s the Reinvestment charge outlined as Reinvestment/NOPAT.

Based on the fundamental progress equation, now now we have:

Progress = Return X Reinvestment charge.

From 2017 to 2024, the widespread ROIC was 14.6 %. Earnings grew at 3.8 % from 2017 to 2024.

The derived Reinvestment charge = 3.8 / 14.6 = 26.0 %

Nonetheless you might also derive the exact Reinvestment charge from the first guidelines. I outlined Reinvestment = CAPEX + Acquisitions – Depreciation & Amortization + enhance in Web Working Capital.

Based on this, the company had a imply Reinvestment charge of 40.2% from 2017 to 2024

You might even see that there’s a distinction between the exact Reinvestment charge and that derived from the fundamental progress equation.

I would deduce that the company was not that atmosphere pleasant when Reinvesting. Inside the context of my valuation,

- I exploit the fundamental progress equation.

- For the prospect analysis, I would assume that the company would start with the historic Reinvestment charge and attain the fundamental charge on the terminal stage.

Valuation

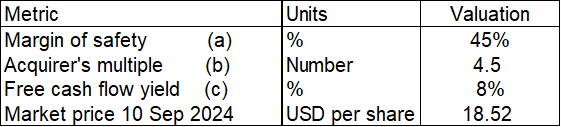

I check out 3 valuation methods to seek out out whether or not or not the company is cheap.

- Intrinsic value. That’s based on the single-stage Free Cash Flow into to the Company (FCFF) model. I obtained an Earnings Price of USD 27 per share. The margin of safety was derived by evaluating the intrinsic value with the market worth of USD 19 per share.

- Acquirer’s Various. This was based on EV / (earlier 3 years widespread EBITDA). Primarily based on Tobias Carlisle who favoured this metric, a worth of decrease than 6 is taken into consideration low-cost.

- Free cash stream yield. That’s based on the historic 2017 to 2024 widespread Free cash stream to the company dividend by the current market worth. I objective a charge larger than double the risk-free charge.

The outcomes are summarized in Desk 1. You might even see that each one 3 metrics degree to WNC being low-cost.

When having a look at Desk 1, phrase that the margin of safety was based on projecting the long term effectivity. Nonetheless, the Acquirer’s Various and Free cash stream yield was based on historic effectivity.

Desk 1: Valuation Summary (Author)

Notes to Desk 1:

a) Earnings Price c/w market worth.

b) Enterprise Price / (widespread 3 years EBITDA).

c) (Widespread 2017 to 2024 Free cash stream to the company) / market worth

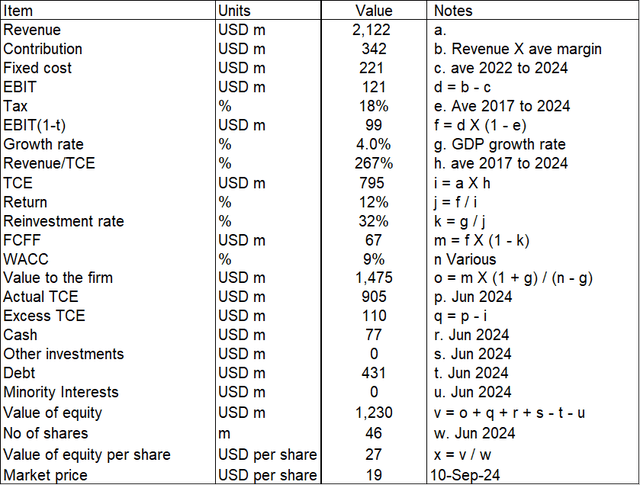

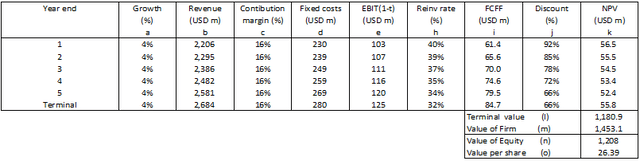

Valuation model – intrinsic value

The valuation model is illustrated in Desk 2. It was based on the following Free Cash Flow into to the Company (FCFF) equation:

Price to the Company = FCFF X (1 + g) / (WACC – g)

FCFF = EBIT(1- t) X (1 – Reinvestment charge).

EBIT(1-t) was estimated based on the working income profile as confirmed in Chart 1.

The Reinvestment charge was based on the fundamental progress equation.

I modelled this as a cyclical agency using 2017 to 2024 normalized values for the revenue, contribution margin, and capital effectivity (Earnings/TCE).

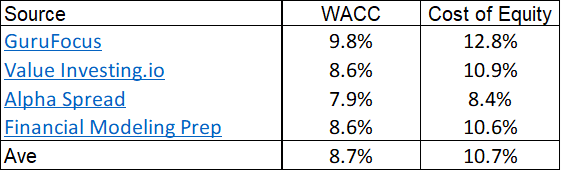

The WACC was based on a Google search for “Wabash Nationwide Firm WACC” as per Desk 3.

Desk 2: Sample calculation (Author)

Desk 3: Estimating the value of funds (Quite a few)

Risks and limitations

The Acquirer’s Various and Free cash stream yield was based on historic averages. Nonetheless I would argue that for cyclical firms, the effectivity pattern repeats. As such, they’re perhaps further reliable than these for companies on the start-up or progress stage.

Secondly, in my valuation model, I relied on the fundamental progress equation to derive the Reinvestment charge. I’ve earlier recognized that the historic Reinvestment charge was loads elevated than that derived from the fundamental progress equation.

To see the have an effect on of this, I used a multi-stage model, the place I decreased the Reinvestment charge from the 40% historic charge to the fundamental charge on the terminal stage.

That’s illustrated in Desk 4. The consequence’s that the intrinsic value was decreased from USD 27 per share to USD 26 per share. It was not very important.

Desk 4: Calculating intrinsic value with lowering Reinvestment charge (Author)

I would add that in Would possibly 2024 I had valued WNC at USD 26 per share. Thus, the current margin of safety is due further to the decline on the market worth from USD 23 per share in Would possibly 2024 to in the mean time USD 18 per share. That’s an just a few 24% decline.

The vital factor downside is whether or not or not you contemplate that the enterprise prospects of WNC had declined by 24% since Would possibly 2024. That’s significantly when the 2024 effectivity seems lower than these in 2023.

When you check out my analysis and valuation, it’s based on a long-term cum cyclical perspective. As such, I’m not fearful regarding the projected 2024 declining revenue. It has all being factored in when making an attempt on the cyclical effectivity.

Furthermore, in my Would possibly article, I had confirmed that in 2023 there was a leap inside the Producer Worth Index in 2022/23. This led to an increase inside the widespread unit selling worth in 2023 for WNC. The Producer Worth Index in 2024 is lower than that in 2023. As such, you shouldn’t be surprised to see lower revenue in 2024.

From 2017 to 2024, ROIC and ROE averaged 15% and 16%. The current WACC and worth of equity are 9% and 11%. You might even see that the returns are larger than the respective worth of funds, suggesting that shareholders’ value was created. These are often not indicators of deteriorating fundamentals.

Conclusion

I nonetheless consider WNC an beautiful agency based on the following:

- Whereas revenue in 2024 was lower than that in 2023, I see this as part of the cyclical effectivity.

- From 2017 to 2024 there have been further metrics with bettering developments than these with deteriorating ones.

- There was no very important change inside the quite a few solvency and liquidity metrics.

The issue was determining the “trustworthy worth”.

I used a single-stage FCFF valuation model to seek out out that the intrinsic value was USD 27 per share, thereby providing larger than a 30% margin of safety.

Recall that this intrinsic value was based on assuming the widespread 2017 to 2024 values for the vital factor parameters. These averages have been lower than the current values. A margin of safety based on these low averages is a conservative technique.

On the same time, the Acquirer’s Various and Free cash stream yield moreover components to the company being low-cost.

Based on these, I would consider WNC an funding various.

")

")

Q3 2025 Earnings Call Transcript")

{kind=link}