[ad_1]

Queso/iStock via Getty Images

My prior thesis on Upstart Holdings (NASDAQ:UPST) was fairly simple. They use AI and machine-learning to make better credit decisions than antiquated systems like the FICO score. This allows them to identify borrowers who are low risk but incorrectly are labeled as unworthy of credit by the existing system. Similarly, their models can also identify people who have high FICO scores but nevertheless are at high risk of defaulting on their loans. This improvement is measurable and repeatable. Upstart aims to not carry the credit risk themselves, has partners that originate and hold the loans, paying Upstart a fee for use of their algorithm. It is supposed to be a capital-light business model that allows them to leverage their tech to make better loans while not carrying the risk of defaults on their own books.

The AI works

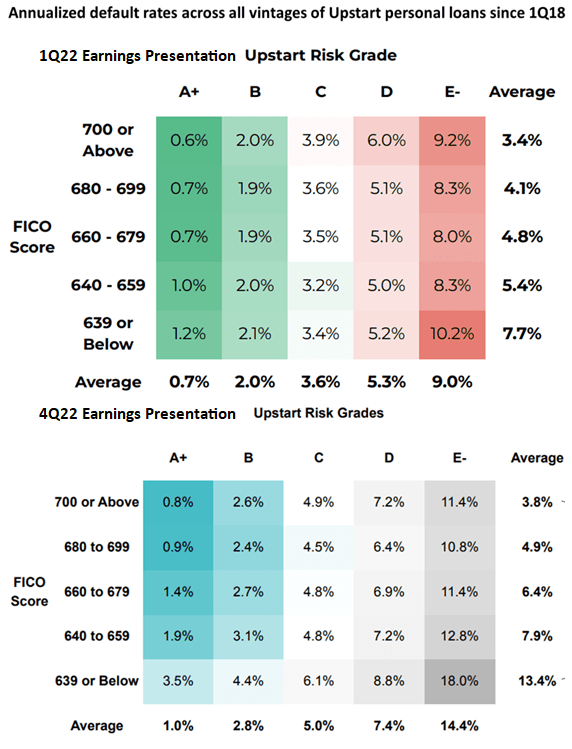

The fact that their model is more predictive than traditional credit checks is verifiably true. Upstart models are still more accurate and have better outcomes than FICO scores. However, if you view their model’s performance before and after the rate hike cycle, a couple of things become immediately clear. Upstart publishes a comparison slide of its Upstart Risk Grade to a standard FICO score. I will post the first version of this graphic that I used in a previous article above the one from Upstart’s most recent earnings report.

Annualized default rates of Upstart personal loans (Upstart)

Both of these graphics include vintages starting from 1Q18. The top table includes only vintages through 3Q21 while the bottom one includes additional vintages through 2Q22. Two things immediately jump out when I look at this data. First, delinquencies are up across the board across every FICO Score range and Upstart Risk Grade. This is not surprising as unsecured personal loans delinquency rates were uncharacteristically low across the board in 2021 and the first part of 2022 because of pandemic stimulus. Delinquencies were expected to rebound to at least pre-pandemic levels, and that is evident in the data shown here.

However, the difference in default rates is especially pronounced in the lowest FICO Score range. Borrowers with credit scores at 639 or below have almost doubled their default rates from 7.7% to 13.4%, and that’s a much bigger increase than other credit tiers. Keep in mind that this is on all loans since 2018, so the older loans in this data set are already seasoned and have already seen most of their losses. A degradation that big across the board even on their seasoned portfolios is a big deal and it means the newer vintages must really be struggling.

This is a big deal for Upstart because this is their core borrower cohort. Upstart targets those who have not been served by the traditional lending industry but who nevertheless have low credit risk. People with higher FICO scores have access to credit via more traditional routes, meaning Upstart typically serves borrowers with low FICO scores.

Why did the business model break?

If Upstart’s model works better, why have their originations, and therefore revenues and profits, dropped off a cliff? Better technology may lead to better outcomes, but Upstart did not position itself well for 2022, their growth is not completely in their hands, and their execution on some key elements that were under their control was poor.

Macro Headwinds

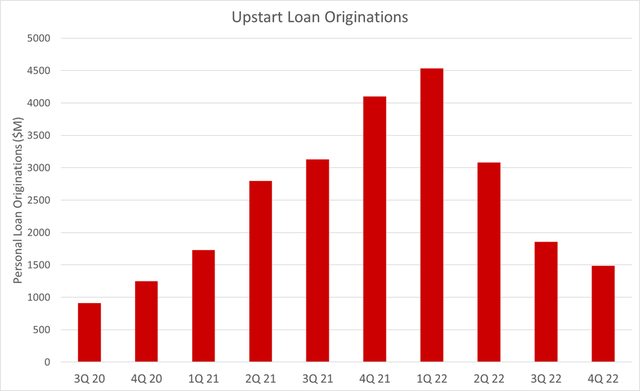

The data above lead to a logical explanation for Upstart’s rapid decrease in originations and therefore revenue. When the credit gets tight, lenders pull back on the highest risk loans first because delinquency rates for these borrowers skyrocket when the economy slows. The very highest risk loans in debt portfolios are unsecured personal loans to low FICO borrowers. When debt investors go risk off, the type of loans that Upstart specializes in are the first ones they stop buying.

Upstart loan originations by quarter (Author)

The cracks started to show in 1Q22, when Upstart increased the amount of loans they hold on their own balance sheet from $261M at the end of Q4 to $604M at the end of Q1. Rather than stay true to their capital-light model, they used their own cash to originate loans that otherwise would have gone unfunded. The pull back from debt investors was a bellwether for what would happen to originations throughout the year.

The tale of 2022 was that of the fastest rate hike cycle in the history of the USA. The ABS markets and hedge funds that had been greedy buyers in the fast and loose capital regime of 2020 and 2021 pulled back and starved Upstart of the capital it needed to continue its growth story. Upstart could not continue to supplement origination volumes with its own balance sheet. Their banking partnerships could not and did not make up the difference. Originations cratered, as did revenue and profits.

Holding unhedged loans was a big mistake

After they began using their own balance sheet as a makeweight in 1Q22, I wrote about about a risk that I didn’t feel was getting the attention it deserved – fair value adjustments. This idea has come to the forefront in the wake of the Silicon Valley Bank (SIVBQ) collapse, and is now much better understood by most investors. What I wrote in that article turned out to be particularly prescient:

If rates rise slowly, the increasing interest income from the loans held makes up for the change in the fair value. However, when rates rise fast, the decrease in fair value can overwhelm the net interest revenue. Fair value adjustments were a tailwind for all of 2021, contributing positive revenue to every quarter last year. However, the winds have turned, and these adjustments represent an $18M revenue loss in 1Q22 […] Interest rates are expected to move faster in the second, third, and fourth quarters of 2022 than they did in the first quarter. So the fair value adjustments are a significant headwind moving forward.

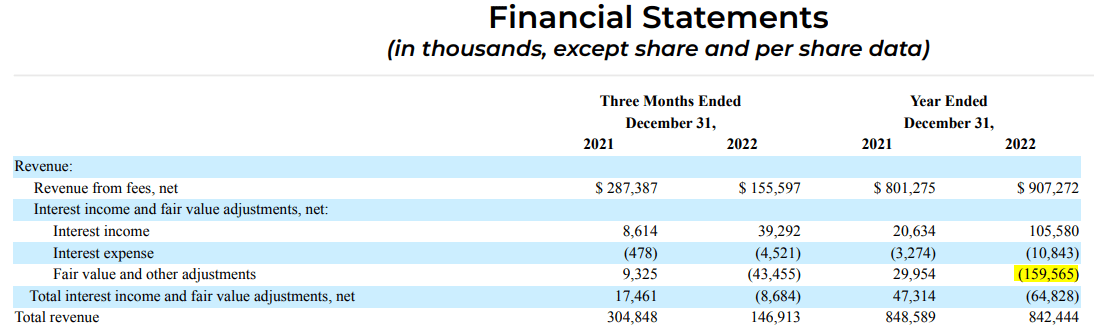

How much did fair value and other adjustments end up hurting Upstart in 2022? Way more than management planned for and more than even I anticipated when I wrote that article last May.

Upstart revenue breakdown highlighting fair value losses (Upstart 10-K)

The fair value adjustments absolutely overwhelmed the net interest income. The $30M gain in fair value from 2021 turned into a $160M loss in 2022. Despite raking in $95M in net interest in 2022 compared to only $17M in 2021, their total net interest and fair value adjustment revenue went from a gain of $47M in 2021 to a loss of $65M in 2022. That $100M swing was a huge contributor to them missing their guidance all year long.

That loss is on management

The worst part about that loss is that it was entirely preventable. When a financial institution holds a large amount of fixed rate assets on their books, like Upstart’s fixed rate personal loans, there are financial derivatives like interest rate swaps that they can use to offset the risks of rate hikes. A competent risk management team should have identified this.

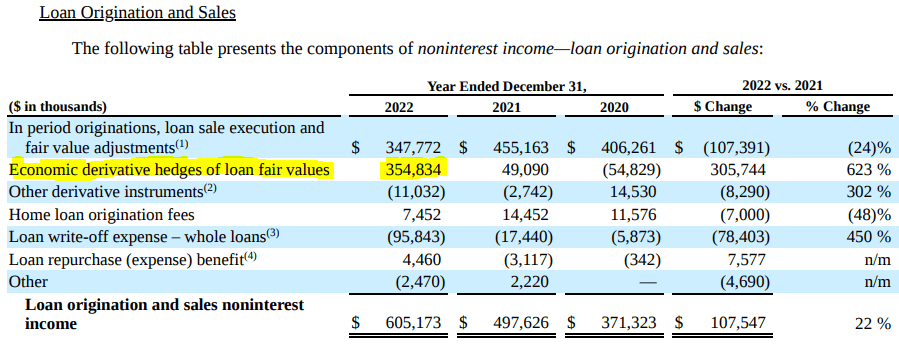

This is precisely the type of oversight that led to SVB’s collapse. Upstart should have created a hedging strategy to keep them insulated from rate volatility. Instead, they did nothing and the result is that the unforeseen rapid rate hikes had a huge drag on their top and bottom lines. Fintech competitor SoFi Technologies (SOFI) also significantly increased the amount of loans they held on their books in 2022. However, SoFi’s comprehensive hedging strategy brought in $355M of revenue in 2022, effectively offsetting the decline in fair value of the personal loans they hold on their balance sheet, as seen from this table taken from the SoFi 10-K

SoFi non-interest income breakdown highlighting gains from hedges (SoFi 10-K)

It is worth mentioning that as rates come down, if Upstart’s personal loan portfolio remains unhedged (which it probably will), the opposite effect occurs. If all else remains equal, fair values will increase as rates decrease. However, part of the “other adjustments” that are included in the line item are charge offs of delinquent loans. If delinquencies continue to rise, it will offset the fair value gains they will have from decreasing rates. Default rates will most likely be heavily tied to unemployment, I’ll discuss this more below.

Funding Sources

Upstart has recently stressed that they are working hard to fix this liquidity crisis from their loan buyers. They’ve highlighted three areas where they are focused: building out their bank partnerships, increasing auto dealer rooftops, and securing reliable and consistent funding partners.

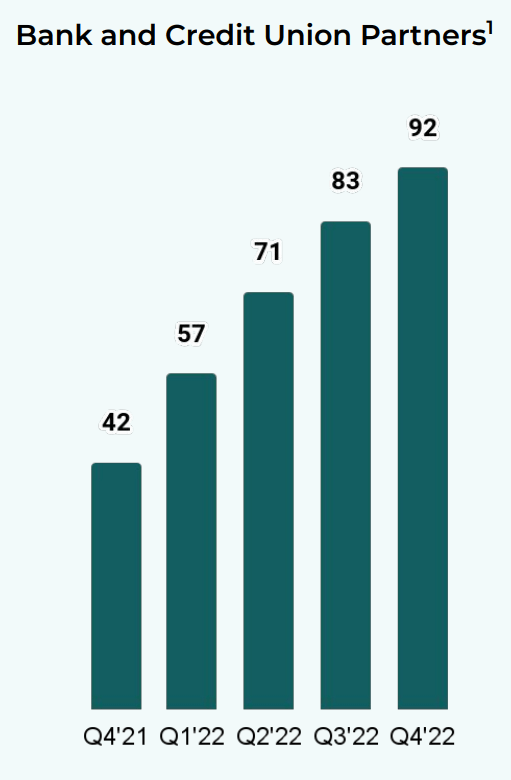

Bank Partners

Upstart has done a great job of securing bank partners to use their platform. This is a consistent source of funding and many of these partners have completely dropped FICO scores from their risk analysis, showing full trust in Upstart’s AI platform.

Upstart bank and credit union partners (Upstart)

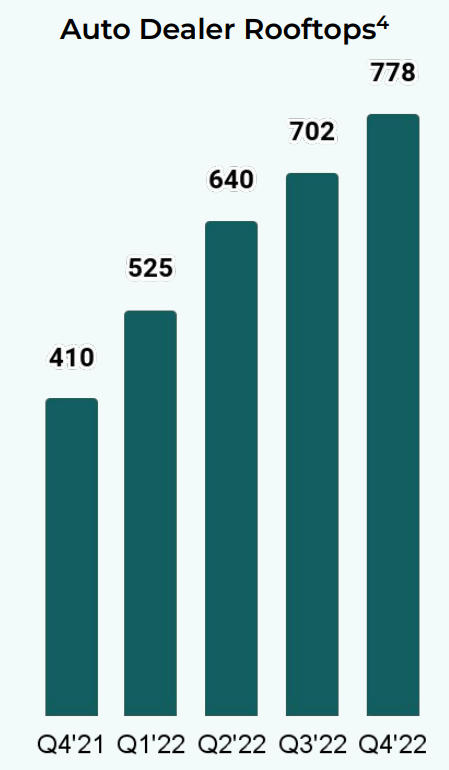

Auto Dealer Rooftops

Upstart is expanding their TAM by launching auto loans. This is a new vertical for them and should help them to reaccelerate growth. They are quickly expanding their partnerships inside the auto sector as well. There appears to be rapid adoption in the industry, and their recent partnership to be Acura’s preferred provider is a boon that was only just announced at the beginning of March. The more dealers they persuade to use their technology, the greater their origination revenues will be.

Upstart auto dealer rooftop partnerships (Upstart)

Reliable and Persistent Funding Partnerships

Upstart has been looking for a more reliable funding source that they can maintain even during macroeconomic turmoil. Management began discussing this in the 2Q22 earnings call and CEO David Girouard had this to report in their 4Q22 call:

In our earnings call in August, I told you that we would begin to investigate partnerships that could provide more reliable and persistent funding to the Upstart platform. I’m happy to report that we’re in late-stage discussions with multiple potential partners in support of this goal.

Upstart will never control their own destiny

All of these partnerships show excellent progress and allow for greater flexibility and better access to funding. However, the cold hard truth is that all of these funding sources remain out of Upstart’s direct control. That has demonstrably changed the thesis in my eyes. Upstart will always be at the mercy of its funding sources, and will therefore always ebb and flow with the credit cycle.

Let’s say they secure a large funding source that guarantees them $5B in funding. By the time the top of the next credit cycle comes around, that line will most likely be drawn in excess of $4B. Their originations dropped from $4.5B to $1.5B in a matter of three fiscal quarters. Their large funding source will never be enough to make up that difference. In the Q&A session during the last earnings call, there was a back and forth between analyst Arvind Ramnani and CEO David Girouard that highlighted this problem (I added the emphasis):

Arvind: Let’s say, a few years from now, we go through another kind of tough economic cycle and then you are sitting with the base of maybe 500 or more lenders. Will that kind of make this situation a lot easier?

David: I would say, it’s one of several things that we would like to put in place before the next cycle, if you want to put it that way. Having a lot more lenders on the platform is great, but if they all act and behave the same, then it doesn’t help all that much. But in reality, the lenders that are on the platform today, they will look back at this time and say, well, it turns out the Upstart loans performed all the way through that.

It is great to say that having this time as a proof of concept for Upstart’s model helps, but the truth is that lending and credit cycles are extremely cyclical. They go through a repeating boom and bust cycle. I had hoped that Upstart’s technology was revolutionary enough that it would allow them to become a secular grower. I thought there was a chance that the technology was differentiated enough to allow them to grow even in a tough environment. The full 2022 annual results disabused me of that notion, and this response from the CEO was the nail in the coffin for that theory. Upstart is a cyclical, it is not a secular growth company, and that means the investing strategy changes.

My Plan for Upstart

I like to identify and invest in companies that I believe can grow and thrive through an entire economic cycle. I like to pick companies that I can see myself holding for at least 5 years and in most cases for decades. Upstart is not that kind of company and it never will be. However, it’s a company that I have spent a lot of time following in a space that I will continue to monitor moving forward. I have a long-term plan for when I will buy Upstart shares and a short-term trading strategy.

Long-term Plan

It seems counter-intuitive, but you want to go long on cyclicals when their valuation has cratered but the new boom cycle is about to start. You then want to unload the shares when the valuation looks like a bargain, but the credit cycle is about to bust. If you are a believer that the Fed is going to pull off a soft landing, then right now might be the time to buy Upstart.

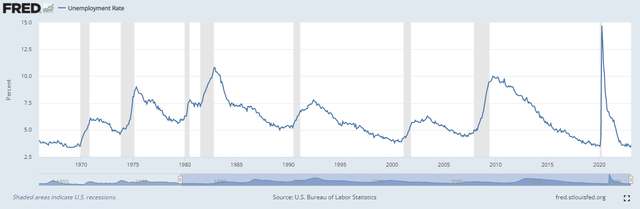

I don’t believe that is going to be the case, and even if it is, I still believe it is a little early to buy shares. I cannot time the bottom or the market, but Upstart’s main revenue driver is personal loans, and the performance and appetite for personal loans is very tied to unemployment. As such, I do not believe we have seen the trough for this credit cycle. Go back to the very first graphic I put in this article. Delinquency rates have already spiked as stimulus money has dried up, but the US is still at 50-year low unemployment rates.

Unemployment Rate (FRED)

If we are due for a recession, unemployment will increase. If unemployment increases, heavy demand from debt investors is not coming back any time soon. Even if there is no recession or a mild one, a reversion to the mean in unemployment seems almost inevitable, and that would mean delinquencies have not seen their trough. My long-term plan for Upstart is to buy it once unemployment peaks, stabilizes, and begins to come down. This will almost definitely mean that I will miss the bottom and will miss some of the gains. It also means that I have a high chance of missing a catalyst if they do secure a large funding source sometime this year or as they scale the auto lending business.

I am ok with that because I don’t want to own a cyclical until I am certain that we are out of the trough. Unemployment to me is the easiest and most visible signal to follow for Upstart. Others may feel differently and I respect them and their investment decisions. I love discussing dissenting opinions and encourage anyone who disagrees to share their thoughts in the comments.

Short-term Plan

One of the benefits of Upstart stock is that it is incredibly volatile. Implied volatility (IV) on Upstart options is really high, which results in excellent premiums for selling options. Upstart is therefore one of the best stocks that I know of to sell cash-secured puts and covered calls on. The extremely high IV coupled with large options volume leads to not only good premiums, but very tight spreads between bid and ask prices, and makes rolling positions very easy when necessary. While my main investment strategy is to buy and hold excellent companies for years, I do use a portion of my portfolio (less than 10%) to run the wheel options strategy. Upstart is one of my favorites for this strategy, and it is one of the stocks I will continue to sell options on.

Conclusion

I originally thought that Upstart would be a company I can buy and hold for decades. However, its performance during the last year has, for me, definitively proven that it belongs in the cyclical basket and not the secular growth basket. That will make it an excellent turnaround play when the time is right to invest. I do not believe that time is now. I will be keeping an eye on unemployment and will keep a pulse on the company and continue to review quarterly results. While I am bullish on their underlying technology, I am neutral on the company for the time being.

[ad_2]

Source link