We could blame the current market downturn, especially in tech stocks, on a lot of things. SPACs. Russia’s invasion of Ukraine. The Rona and supply chain issues. Inflation. But we prefer to make Lenin-look-alike Jim Cramer our scapegoat. The list of controversies surrounding this former hedge fund manager makes up the bulk of his Wikipedia entry. About a decade ago, Cramer famously gave us FAANG, an acronym that refers to the five biggest tech companies in the world (now deFAANGed as MAMAA by Cramer). Ever since, investors have had a somewhat unhealthy obsession with this pantheon of corporate tech gods. This unholy obeisance has surely helped unbalance the stock market, as these five stocks accounted for nearly 20% of the value of the S&P 500 at one point. Even as recently as mid-2022, they represented about 15% of the total value.

The “N” is (was?) for Netflix (NFLX). In case you haven’t been paying attention because you have better things to do than stream Season 3 of “Too Hot to Handle” – like generate alpha – the OG of streaming services hit the skids this year. The stock is down more than 60% year to date after reporting “significant” losses in subscriptions. We use the quotation marks because the drop in subscribers amounted to about 0.5%. In addition, the company has still generated more than $3 billion in earnings on more than nearly $16 billion in revenue in the first half of this year. We can attribute the drop to real concerns about the rise in rival streaming services, but also to the totally unrealistic fantasy fueled by FAANG fandom.

Say that five times real fast while we introduce you to Roku (ROKU), a sort of pure-slash-pick-and-shovel play that many of our readers think should be in any self-respecting tech portfolio.

About Roku Stock

Roku is something of a hybrid in the streaming services industry. It originally started life as a Netflix project to build a device to enable users to stream the company’s content directly on their TVs, similar to the old-fashioned cable box. The story goes that Netflix thought this little piece of hardware would cause licensing problems and keep its service off of similar platforms when they eventually emerged. So Netflix spun off the idea into a separate company called Roku, which sold its first device in 2010. About four years later, it began integrating its Roku functionality into smart TVs. In effect, Roku is an operating system (OS) for smart TVs, similar to Android or iOS for smartphones. And, about five years ago, the company added its own free, ad-supported streaming channel. That same year, in 2017, Roku IPO’d. Revenues have been rising rapidly ever since:

Roku entered the Rona hype cycle in March 2020 with a market cap of about $9 billion or so. At its peak a little more than a year ago, the company was worth north of $60 billion. Today, Roku stock is trading down nearly 80% year to date, with a market cap of about $7.5 billion. Is now a good time to buy? If so, what is our investment thesis?

Roku is the Leading OS for Smart TVs

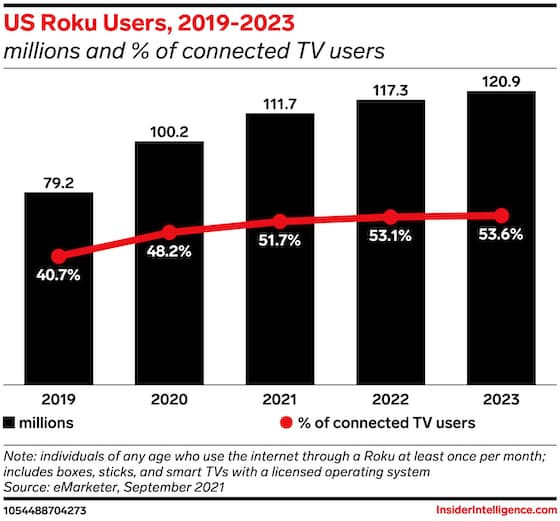

The title says it all, right? The idea driving the Roku bulls to slaughter to its side is that the company is the leading OS for smart TVs in the same way that Android is the main OS for smartphones outside of Apple iPhones and Microsoft Windows for PCs not built by Apple. In fact, Roku OS has held the title as the No. 1 smart TV OS in the United States for the last two years, according to NPD’s Weekly Retail Tracking Service. The company crossed 50% of the market of total users of smart TVs last year:

That’s certainly the trend one would want to see if betting on the long-term dominance of the Roku OS. After all, Microsoft has done pretty well for itself and its shareholders. If you had enough pocket change to first invest back in 1986 at the IPO price, you would have realized a +30,000% gain. Google’s dominance in the smartphone market has helped propel it to a $1.3 trillion market cap today. However, we would not be the first to note that the smart TV industry may not be ready to cede the market to Roku, with major manufacturers like Samsung featuring their own OS, advertising platform, and even free ad-supported channel.

How Does Roku Make Money?

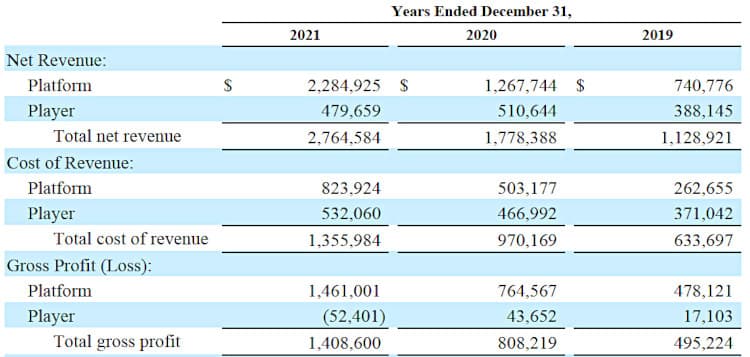

Obviously, one of Roku’s money making schemes is licensing its software to TV manufacturers. The company splits its revenues between two segments – platform and player. The former is basically software and services. In addition to licensing its Roku OS to TV brands, the company also generates money from the sale of digital advertising and other services related to its OneView ad platform, which enables advertisers to set up, change, and measure ad campaigns entirely on their own. Of course, machine learning helps with precision advertising, and Roku also uses AI as part of its content distribution services to help publishers target new audiences that are more likely to subscribe to their services. That stream of revenue also includes things like selling branded channel buttons for content companies like Netflix on Roku remote controls. The player revenue is primarily from the sale of streaming players and audio products.

As you can see, hardware sales are becoming less and less relevant, as more and more smart TVs displace dumb legacy ones. This is not a surprise to Roku, which is increasingly emphasizing its own channel offerings (more on that shortly) to ensure more traffic flows (along with ad dollars) through its platform ecosystem. Unfortunately, Roku does not drill more deeply into platform revenue, so we don’t know how much money comes from advertising versus OS licensing agreements. That’s annoying, especially if we want to track progress in ad spend or changes in OS dominance. Instead, we have to rely on other proxies for performance.

Roku Key Performance Metrics

The company touts for key performance measures:

- Gross profit. This is a no-brainer. Roku’s gross profit grew 74% between 2020 and 2021, from about $808 million to more than $1.4 billion. Based on gross revenue against the cost to produce that revenue, gross margin jumped around 6 points to about 51%. One would expect that number to continue to improve as the shift away from hardware becomes less of a drag (see chart of quarterly revenues and metrics below).

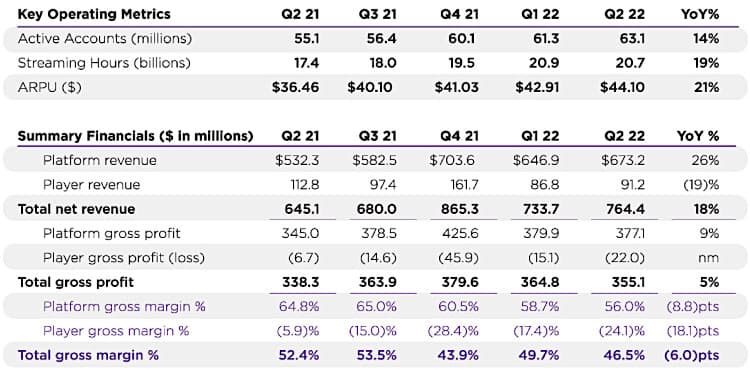

- The other way Roku measures monetization of its platform is average revenue per user, which increased from $28.76 in 2020 to $41.03.

- Roku tracks active accounts to gauge the size of its user base that has streamed content on its platform, even though you don’t need an account to watch such gems as Naturist Cleaners (NSFW) on your browser. So the 60.1 million active accounts as of the end of 2021 does not include streaming on non-Roku platforms. The number of active accounts increased 17% compared to last year.

- Finally, the company tracks streaming hours on its platform – how long people are staring at screens. Streaming hours grew from 58.7 billion hours in 2020 to 73.2 billion hours in 2021, a 25% increase. For a little perspective, Americans working full time put in about 230 billion hours at their jobs last year, based on data from Statista. Just think how much time they can be spending on the Roku platform!

Should You Buy Roku Stock?

In an effort to do just that, Roku has invested in its own content, in addition to selling subscriptions to other streaming services and leasing programming for its free ad-supported channel. In May 2021, for example, it launched Roku Originals, based on the content library it bought for less than $100 million from Quibi, the $1.75 billion disaster that involved streaming short-form programs on mobile devices. This salvaged such Emmy-worthy shows as Murder House Flip, a home renovation show focused on houses where grisly homicides took place. Kids, gather round! Last year, it also acquired the rights to This Old House, a slightly less dark take on home improvement. Roku’s magnum opus, a fictionalized biopic of Weird Al Yankovic, will be out next month.

Content may be king, but you’d have to be a fool to invest the sort of money that Roku and others are pouring into the disposable distractions that pass as entertainment today. Maybe our bias is blinding us to the potential of just piling on show after series, but ad dollars can only support some much fluff. To our point: Roku’s most recent Q2-2022 report noted “there was a significant slowdown in TV advertising spend.” The company also lost nearly $140 million so far in 2022, and has most often ended most years in the red.

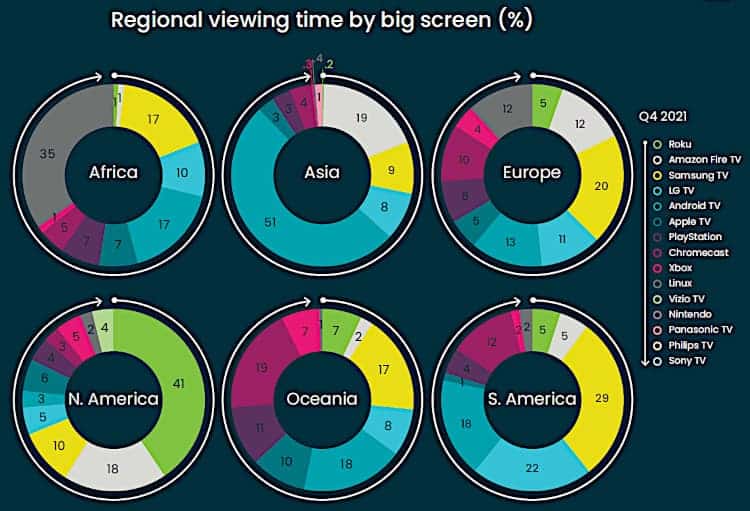

We should also note that most of these financials refer to Roku performance in the United States. Currently, its products are used in more than 20 countries, while the Roku OS is available in six countries. Everywhere but North America, however, Roku has single-digit market share in viewing/streaming time, according to Conviva, an online video analytics and optimization firm.

Roku has yet to consistently find profitability. Advertising dollars are down, meaning less money (or bigger losses) to spend on questionable content to drive engagement. Long-term dominance of its Roku OS in the United States isn’t exactly assured, and the company is struggling to expand internationally in a meaningful way so far. It’s a drama we would not pay to watch.

Conclusion

At the end of the day, does anyone buy a laptop, a smartphone, or even a smart TV for its operating system (aside from the Steve Jobs turtleneck posse)? We want our devices to do cool stuff and not give us the blue screen of death. Television remains a mostly passive pastime, with an endless amount of ways to waste time. Roku should focus on its core competencies – continuous improvement of its OS; innovative ways to generate ad dollars, like its new partnership with Walmart featuring shoppable ads – and ditch the cheesy content. After the Weird Al movie. It actually looks pretty funny.

Tech investing is extremely risky. Minimize your risk with our stock research, investment tools, and portfolios, and find out which tech stocks you should avoid. Become a Nanalyze Premium member and find out today!

")

{kind=link}