Dikuch/iStock through Getty Pictures

Oil Market

I feel the important thing level is we aren’t shedding 5M barrels per day of Russian oil exports, as a result of the forecast was for a world surplus (IEA, OPEC, EIA), so the quantity wanted to be produced exterior Russia for provide and demand to stay in stability is far lower than the misplaced 5M barrels per day of Russian exports. I feel the explanation costs skyrocketed like it is because the inducement to delay restocking primarily based on the expectations of decrease future costs making a suggestions loop between declining near-term inventories and backwardation of the futures curve.

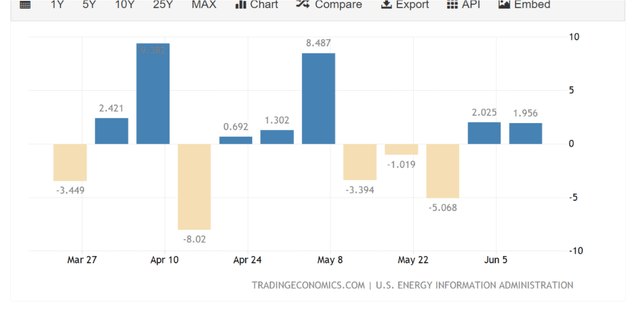

I don’t suppose there’s a international manufacturing capability scarcity proper now in any respect. The 1Y EIA stock change chart is proven beneath. Discover it is not fully one-sided attracts.

US Oil Stock Change (tradingeconomics.com)

The traditionally low inventories are primarily an unwillingness to pump as a result of the futures curve continues to point out future oil costs decrease at longer dated contracts often called backwardation which is the alternative of contango.

I feel the good transfer for a US shale govt is to hedge in my view locking in costs above $100 a barrel and ramping manufacturing. There may be loads of OPEC capability additionally particularly amongst UAE, Iraq, Kuwait, Saudi and the center jap nations. I feel international demand won’t maintain up proper as inventories are restocked. I imagine in a restocking atmosphere at low costs which causes stock builds and pushes costs decrease proper as issues about international demand turn out to be vital.

One of many issues for oil quick sellers is and partially why oil costs are literally so excessive is producers do not need to ramp considerably and push the market again into oversupply and subsequently have been holding again. At this worth degree although I might anticipate elevated manufacturing particularly from shale as rig counts have been steadily rising the truth is.

Inventories are round decade lows. As these are rebuilt and extreme quick run shortage fears are alleviated, by OPEC+ ramping, US shale and remainder of world non-OPEC and non-Russian provide, in addition to probably Iran/Venezuela and huge SPR releases globally, I might suppose oil costs come again down from the stratosphere. Bear in mind there isn’t any OPEC of US shale (that means coordination among the many US shale business) proper now and there’s a big revenue incentive to hedge and pump.

I’ve written extensively on contango oil trades in lots of articles. Contango trades revenue from storing oil by locking into two contracts on a futures curve and incomes the unfold (revenue if the curve slopes upward) by holding oil. Contango can happen in rising costs environments or falling. It’s a matter of whether or not the market expects costs sooner or later to be larger.

I really feel the again finish of the WTI curve is the worth play in comparison with the costly entrance finish if you wish to be lengthy oil. When costs at these completely different future dates converge or invert (i.e., oil for close to time period supply turns into inexpensive than oil for supply in 6 months) it encourages restocking as all potential unfavorable carry worth draw back will be hedged and profited from by a locking into the next future promoting worth and simply storing the bodily oil. Massive oil buying and selling corporations do that when the curve permits it, that’s, so long as costs alongside the curve slope upward.

A contango restocking atmosphere usually strikes costs decrease thereby self-reinforcing the cycle the opposite method as inventories fill again up creating a major oversupply of oil for close to time period supply and decrease costs in comparison with the longer dated contracts. It is a way more nuanced state of affairs than many imagine which is why I really feel the oil rally is within the ninth inning at this level. If commodities come down, I feel this may push US inflation down simply via decrease enter costs but in addition will put strain on rising market commodity currencies and economies akin to Brazil and Russia. US demand, progress and employment needs to be robust as ought to the US greenback, which inserts with a decrease oil worth atmosphere.

Massive oil buying and selling corporations, and refiners who’re patrons of oil, should not restocking as a result of the futures curve is signaling costs can be decrease sooner or later (unfavorable stick with it holding oil) and in addition there may be an incapability to hedge this unfavorable carry as a result of longer dated oil futures costs are decrease than close to time period or spot costs. This implies patrons of oil have basically no selection however to attract down inventories and delay restocking. When this issue adjustments – that means oil for supply in 3-12 months is the next worth than close to time period supply costs (1 month or spot) it would permit restocking and better tanker utilization.

Additionally, with oil costs anticipated to be decrease sooner or later because the curve is signaling now, there may be additionally the query of why restock now at a excessive worth? Many merchants and patrons of oil are deferring restocking and sure simply buying hand to mouth or small quantities of what’s solely wanted on the time.

What might trigger or catalyze this shift into contango from backwardation?

1) Longer dated futures rise above near-term costs on the expectation of a continued or worsening scarcity this yr.

2) Close to-term costs fall at a sooner price than the longer dated future costs.

I feel this backwardation of the curve (downward sloping) will flip to contango (upward sloping) as a result of both the discounted back-end rises at a sooner tempo than the costly front-end or the front-end is extra oversupplied than individuals imagine, inventories begin to rise, and near-term/spot costs fall at a sooner price than the again finish of the WTI futures curve.

As soon as this happens it turns into self-reinforcing in the wrong way the place restocking causes extra spot/near-term provide in comparison with supply at a later date and an ever-larger contango curve construction. We noticed this in March 2020 the place the curve blew out to super-contango in what finally turned a unfavorable oil worth atmosphere, then subsequently blew out the alternative method into super-backwardation. Which is why really feel it’s a self-reinforcing cycle in both path.

Tankers

On account of the Russia/Ukraine battle, tanker ton-mile demand is about to extend in my view and the preliminary response of the market in tanker charges to the conflict in Ukraine has confirmed that. Tanker charges have just lately stabilized for now at the next but nonetheless traditionally low degree. I feel the transfer in tanker charges continues upwards and the preliminary knee-jerk response to the conflict is appropriate and but to be absolutely realized.

Russian oil can be despatched to China or Venezuela as a substitute of Europe including to ton-miles. Whereas Europe will probably fulfill demand via imports from North and South America and Africa somewhat than Russia – additionally including ton miles.

Additionally, an Iran nuclear deal and return to the JCPOA would require a big enhance in authorized tanker utilization. Iran has been exporting on unlawful tankers. With compliant manufacturing, comes the necessity for compliant, registered tankers from authorized and environmentally regulated tanker corporations.

In 2020 on the peak of the pandemic and surge in tanker charges, Euronav CEO mentioned through Freight Waves:

The opposite potential headwind for (tanker) equities includes the speed hangover to inevitably comply with the “tanker get together.” In keeping with De Stoop, “Everyone knows that when oil is saved, in some unspecified time in the future will probably be consumed, and when it’s, demand for transportation can be decreased and oil manufacturing can be decreased.”

That’s precisely what occurred, and why tanker charges subsequently crashed following the pandemic growth which even rivaled pre-2008 tanker charges. Now although, inventories have been drawn down beneath historic norms and if the restocking frenzy at first of the article takes maintain, the tanker sector can be an enormous beneficiary as tankers are utilized to move alongside longer routes than beforehand and in addition to retailer oil for revenue of buying and selling corporations.

Might this result in one other hangover? Probably, however not earlier than big income and the next tanker fairness share worth vary repricing. It might even be of much less magnitude and a little bit of a smoother cycle in my view than the very quick and risky tanker pandemic growth/bust tanker cycle.

One motive is even when I really feel the worldwide financial system will sluggish, it won’t be turned off utterly, so the whole stock builds will not be as giant (although inventories are developing off a decrease base than earlier than which is optimistic for tanker demand comparatively), and subsequently the following eventual draw part (unfavorable impact on tanker charges) can be much less extreme for tanker equities. Primarily, I imagine a future backside in tanker charges and share costs after a possible vital tanker price run-up is at a structurally larger degree than the unprofitable atmosphere for tankers just lately.

So, I feel we’re going up, and even any unfavorable after-effects because of long run stock attracts that might ship tanker charges and tanker equities decrease in some unspecified time in the future can be coming down from a considerably larger start line and unlikely to achieve the rock-bottom ranges we’ve got seen.

Publish-2008, there was an enormous crash in tanker charges and that’s the longer-term cycle which has additionally healed. Within the very high-rate tanker sector revenue growth days previous to the 2008 International Monetary Disaster, tanker house owners ordered a really giant variety of new builds ships. When the worldwide financial system weakened oil demand fell off, whereas the newbuilds continued to reach and this led to an oversupply of ships. The orderbook for brand new oil tankers seems to be a lot better now and constructing capability is basically taken up by container ships and dry bulk vessels. The fleet is previous and continues to be scrapped, particularly ships that are shut to twenty years previous and haven’t been outfitted with costly environmentally pleasant scrubber know-how. These are prime for scrap, which might decrease provide. We’re completely not seeing the identical potential tanker oversupply points that we’ve got seen with the business prior to now.

Macro Backdrop

I feel the US CPI will show extra responsive and probably simpler to carry to focus on worth stability with out derailing GDP progress in the US in comparison with different international economies. I stay steadfast with a protracted US greenback theme operating via the portfolio. The USD is supported by a mess of things. These embrace a major $13T determine of world USD denominated debt, relative financial power, fundamentals, resilience, and efficiency of US information versus practically each different financial system on the planet resulting in divergent financial insurance policies (the place one other central financial institution lowers or holds charges whereas the Fed tightens coverage and sends yields larger). This creates comparatively larger actual yields and strengthens a forex (the USD). Intuitively this is smart as traders need to maintain a low inflation forex that may earn a risk-free lending yield larger than different sovereign bond markets in what is named a carry commerce.

In one in every of my earlier articles, I defined carry trades. I mentioned:

Carry trades are one of the crucial vital forces in international alternate markets. An instance is borrowing yen at round 0% yield and investing in Russian bonds yielding round 7%, capturing the distinction and in addition standing to achieve on any appreciation within the RUB in opposition to the yen. It may be a worthwhile technique particularly when utilizing leverage, however carry trades collapse when the funding forex (decrease yielding) appreciates in opposition to the asset forex (larger yielding). This FX appreciation of the funding forex in opposition to the asset forex wipes out good points on the rate of interest differential when transformed again.

Japan:

In keeping with Reuters:

Financial institution of Japan Governor Haruhiko Kuroda mentioned on Monday the central financial institution’s prime precedence was to assist the financial system, stressing an unwavering dedication to sustaining “highly effective” financial stimulus.

Not like its U.S. and European counterparts, the BOJ doesn’t face a trade-off between the necessity to tame inflation and assist the financial system, as Japan’s inflation stays modest and pushed by momentary components akin to rising uncooked materials prices, Kuroda mentioned.

“Japan is totally not in a state of affairs that warrants financial tightening, because the financial system continues to be within the midst of recovering from the pandemic’s influence,” Kuroda mentioned in a speech

In an occasion organized by Kyodo Information, Financial institution of Japan chair, Kuroda, additionally commented on the consequences of yen depreciation and mentioned:

It’s extremely probably that steady strikes towards yen weak spot, not speedy strikes, are optimistic for the Japanese financial system as an entire. What’s essential for the financial system is that corporations which have reaped the advantages (export competitiveness) of yen weak spot and seen their income get better will enhance capital spending and lift wages, and there can be a stronger cycle within the financial system for extra earnings and spending.

This is smart and I agree with Kuroda right here. The emphasis is he believes the inflation in Japan whereas nonetheless low is nearly purely pushed by cost-push pressures, not demand pull. Japan inflation has repeatedly lagged and undershot the central financial institution’s goal price for years. At a 2.1% core price and a couple of.5% yr/yr headline price it’s far beneath Europe, the US and most rising markets.

Kuroda made clear he isn’t about to tighten. Actually, I feel a sustained interval of yen depreciation is precisely what he is been ready for so as to sustainably transfer Japanese inflation and expectations larger and he is not about to pour chilly water on the escape route from Japan multi-decade zero decrease rate of interest sure, and secular stagnation downside.

Europe:

The hawks and doves inside the ECB have been debating and ECB chair Lagarde has gone on board with the hawks, for now. In keeping with former ECB chief economist who may be very effectively revered mentioned through Bloomberg:

What actually annoys me within the communication first is that Christine Lagarde deviated from what she mentioned a number of weeks in the past

In it, she dedicated to a much less aggressive path of price hikes than the one the ECB laid out on Thursday and mentioned there was a scarcity of extra demand within the euro space. The newest ECB motion contradicts that supposition, he mentioned. When you use rates of interest to compress demand, I feel it was not likely clear what she was making an attempt to realize by this sequence of interest-rate hikes and what kind of extra demand you’re coping with… If you wish to be a hawk, then it’s important to be constant and say what you need to obtain.

I agree with Praet right here – the ECB’s communication and flip-flopping has been a multitude. A coverage mistake is signaled by the necessity to reverse course shortly after and I really feel the ECB with their hawkish shift and plan to transferring into optimistic charges can be rapidly unwound and reversed as the consequences of Fed tightening are felt.

Additionally it is fascinating the euro has not likely caught a bid with the hawkish shift that means the FX market is both 1) doubting that tightening will really happen or 2) thinks will probably be reversed shortly after or 3) will result in stagflation in Europe and a weak forex.

Extra demand shouldn’t be the issue for Europe’s financial system. It’s once more a value push somewhat than demand pull concern and commodity worth pushed inflation and rather more of a headline CPI downside somewhat than core CPI in Europe because the latter stays comparatively subdued.

In my view, by the ECB slowing Eurozone mixture demand and nominal progress and permitting larger yields and elevating charges it would solely serve to chill nominal GDP and have little impact on inflation resulting in unfavorable actual progress in Europe (stagflation).

My opinion is the ECB ought to let the Fed do the heavy lifting with charges and international inflation and have a powerful greenback. There isn’t any sense in making an attempt to sluggish mixture demand in Europe with larger charges as it’s being largely pushed by meals and vitality costs because of proximity of and dependence on Russian exports. Commodities would reply extra vastly downward to a powerful greenback/weak euro than making an attempt to lift charges and funky off not nice already mixture demand into a world downturn and weaker Eurozone financial system.

What can be more practical in bringing down Euro space CPI with out risking the financial restoration and nominal progress is to diverge from the Fed, preserve charges low and let the euro fall beneath parity. It might push up import worth inflation for Europe although vitality and commodity costs would fall probably fall on a particularly robust greenback and weak rising market demand, and a weaker euro would supply a lift to exports which the German financial system amongst different Eurozone nations are closely depending on and low charges can be maintained. So general I feel that’s the greatest transfer because it retains nominal progress on monitor. I am unable to promise the ECB will not make a mistake right here, however I really feel assured I do know what they need to do which is sustained low charges. Bear in mind Euro space core (ex meals/vitality) CPI is round 3.8% in comparison with 6.0% in USA so there may be a lot much less of an financial overheating downside in Europe.

China:

China faces a distinct downside than most rising markets within the sense it is extremely a lot “the Japan” of rising markets with slowing nominal progress and far decrease inflation than different EM economies.

China’s financial system I feel can be very a lot the epicenter of a world downturn given its dimension and international significance. I feel the yuan will come underneath vital strain as Chinese language banks will must be recapitalized by the PBOC printing RMB because of a company and native authorities non-performing mortgage downside for the key banks in China. The housing market has weakened and I nonetheless really feel the Chinese language financial system has not but bottomed out that means decrease charges can be required for China to keep away from recession, not to mention attain its progress goal. I beforehand wrote:

I imagine as China’s near-term financial descent continues and defaults/NPLs in addition to unemployment rise, Chinese language banks will turn out to be the issue. Chinese language banks have prolonged giant quantities of credit score and are very leveraged. The banking system is round 200% the scale of the financial system in comparison with round 65% for the USA. This China laborious touchdown would require decrease charges and sure printing of RMB by the PBOC to recapitalize banks for dangerous loans so as to navigate via it whereas awaiting a shopper rebalancing. One of many principal points can be stopping unemployment from rising thereby stymieing the Chinese language shopper demand rebalancing away from the supply-side pushed building mannequin. China will probably should depend on robust exports to the remainder of world, to maintain their labor markets working at a great degree

If Chinese language charges are lowered additional and anticipated to remain low, the yuan might turn out to be a well-liked funding forex for carry trades that means it’s borrowed at a low Chinese language sovereign yield, transformed into the next yielding forex such because the USD or BRL (as US Treasury yields have now surpassed Chinese language 10Y bond yields and Brazil yields are north of 10%). The commerce good points on appreciation within the USD or BRL in opposition to the yuan in addition to the rate of interest differential. This may result in downward strain on the yuan in opposition to the USD or BRL when completed in mass, as a pair examples.

Petrobras

Petrobras (NYSE:PBR) trades at a reduction and has the next dividend yield than different oil majors, but there are causes markets have assigned this low cost and that’s as a result of it includes elevated danger. Petrobras is foremost a Brazilian firm although additionally trades within the USA underneath an ADR and there are completely different dangers such probably decrease rising market fairness valuations in addition to forex danger affecting an organization’s debt service functionality when investing in international markets.

Not like China, inflation charges are usually excessive in rising markets and EM forex depreciation in international alternate markets is related to this comparatively larger rising market inflation price. A weak forex will increase import price pressures which present account deficit economies (web importers) are most affected by. So, to defend the forex and stop capital outflows a given rising market central financial institution would elevate charges so as to defend their relative yield benefit from different central banks such because the Fed tightening and transferring their financial system’s yields larger. This disincentivizes promoting strain within the forex because of it being larger yielding, lowers import prices and cools demand within the financial system all exerting downward strain on inflation. The issue is the trade-off between nominal progress and employment in opposition to inflation or the query might be posed as how a lot ache a central financial institution is keen to endure on GDP progress, asset costs and employment so as to preserve the CPI in verify and alternate price steady?

For instance – Brazil has moved their central financial institution coverage price up from round 2% to over 12% during the last couple years. The importance of the transfer in charges has not led to equally vital upward strain within the Brazilian forex, the BRL. I ask, if not even a 1000 foundation level transfer within the Brazil coverage price can ignite power within the BRL, the trail is probably going downwards for the forex as excessive charges start to weigh on the Brazilian financial system and a pause is warranted. If the robust USD, tighter Fed coverage, and a slowing China trigger commodity markets to say no from very excessive ranges presently, it might nearly undoubtedly have an effect on Brazilian commodity exports which the Brazilian financial system may be very depending on, and this could weigh on the Brazilian GDP and employment image and issue into the central financial institution of Brazil’s rate of interest selections.

Whereas Brazil’s central financial institution has been most excessive of their rate of interest actions and gaining a relative yield benefit, it’s a widespread theme amongst rising market financial coverage with many different central banks doing the identical to a lesser diploma.

How does this have an effect on Petrobras, a big Brazilian oil producing firm?

First in a restocking and contango sort oil market as described above, oil costs would probably transfer decrease instantly affecting income and profitability.

Secondly, this decrease oil worth atmosphere would additionally happen alongside a powerful US greenback. Petrobras has a major determine of USD denominated debt, that means a weak BRL and robust USD would have an effect on the corporate’s profitability via the next actual burden of debt compensation. There may be additionally an incredible diploma of political interference within the firm, which is topic to dangers.

Petrobras has $12.25B in USD denominated debt due earlier than 2030 together with different debt. I’m solely specializing in the shorter-term USD-denominated determine. Suppose the BRL forex depreciates 10% in opposition to the USD over the short-intermediate time period. This provides over $1.2B in actual debt expense to the primary determine.

Petrobras has a money and short-term funding stability of 745B BRL or $14 billion when transformed on the present alternate price of round 5.21 USD per BRL. It has a complete present asset place of 154B BRL or round $29.5B USD. Present liabilities akin to accounts payable and short-term debt is round 124.5B BRL or $23.89B USD.

The present liquidity or present asset to present legal responsibility ratio is round 1.24 although if the BRL had been to return underneath extra extreme strain whereas oil costs fall, the ratio might fall beneath 1.00 and liquidity might come into query and the massive dividend being paid to Petrobras traders might be decreased or lower. Fitch and S&P price Petrobras’ debt at BB- whereas Moody’s charges it at Ba1 which all place in high-yield or riskier territory.

DHT

DHT (NYSE:DHT) owns fully VLCC tanker ships also called very giant crude carriers, and I feel that’s the principal draw to investing in DHT versus different tanker corporations proper now. In keeping with the most recent DHT convention name:

To the sanctions and ensuing trades commerce disruptions popping out to the remainder of the Ukraine battle appears to be growing transportation distances. To date, most seen to ships smaller than VLCCs. If freight differentials turn out to be too large, freight are likely to circulation up and down between the completely different ship sizes. We noticed a few of this on the outset of the battle and will regulate trades see these differentials come again the speculation that the tide lifts all boats to carry true.

The pop in freight charges for VLCCs that you just noticed a number of weeks again is an efficient indicator that underlying stability shouldn’t be as dangerous as the present charges are indicating. Take into account that VLCCs usually transport nearly 45% of all seaborne crude oil volumes, that nearer to 60% on a ton mile foundation. That is really the workhorse of the oil business.

The commerce disruptions are altering sourcing of refined oil merchandise, elevating freight charges for product tankers. As this occurs at a time of low inventories of each crude oil and refined merchandise, it backs the query whether or not product tankers are entrance operating crude tankers suggesting the quantity for feedstock and thus crude oil transportation to return subsequent.

A lot of the main focus of the most recent tanker earnings name transcripts is in regards to the impact of Russian sanctions on ton-mile demand (distance) in addition to vessel provide. Little is talked about in regards to the continued drawdown in crude inventories in addition to from Scorpio Tankers’ Lauro who mentioned, “supplying incremental oil demand with stock attracts shouldn’t be sustainable in the long term”.

Not solely is DHT’s tanker class specialization poised to learn for my part from elevated international transportation because of re-routing of Russian oil and restocking of oil, because the business “workhorse”. VLCC’s are additionally essentially the most used to retailer oil in contango trades the place giant oil buying and selling corporations lock into promoting oil at a future date at a excessive worth and achieve the futures curve differential throughs storing the bodily oil. Once more, this could solely occur when the futures curve slopes upward which is what I’m anticipating.

I additionally need to make the purpose we’re seeing divergences amongst vessel sizes and provider sorts with spikes occurring in smaller sized aframaxes in addition to refined product tankers. Product tankers which carry refined oil merchandise and smaller sized aframaxes have outperformed very giant crude carriers.

DHT and the VLCC tanker class charges have underperformed different tanker corporations and vessel courses making it a worth play among the many already low-cost tanker sector.

For instance, Scorpio Tankers, which is a product tanker firm is up round 200% YTD, Teekay Tankers which owns principally smaller vessels is up round 54% TYD, with DHT solely up 18% as a pure-play VLCC class funding.

DHT has a present asset to present asset to legal responsibility ratio of two.86. This makes it much less dangerous from a debt service perspective than Petrobras the place the present ratio is 1.24 as said within the above part. Tankers are additionally extra versatile with the ability to carry out in bullish and bearish oil worth eventualities whereas additionally offering loads extra upside firepower than larger priced vitality producers in my view.

Valuations for tanker equities and tanker charges are nonetheless traditionally very low. DHT has a market capitalization of $1.07B and during the last 5 yr has generated income at a median of round $450M yearly. For comparability, the identical statistic for Apple is a median 5Y annual income of round $280B but Apple’s market cap is roughly 8 occasions the 5Y common annual income in comparison with round simply 2.3X for DHT. Petrobras’ market cap to 5-year common annual income ratio can be within the excessive single digits that means an investor is paying considerably extra for income earned by Petrobras in comparison with DHT.

Conclusion

Sooner or later the expectation of a worsening oil scarcity might trigger elevated oil buying and tanker demand as patrons rush in to compete for restricted oil provide. This may contain robust international progress and vitality demand in addition to transportation of oil to the good thing about tanker corporations.

Or the alleviation of oil shortage worries because of stock builds (SPR releases, OPEC ramp, US shale rising rig counts, elevated international provide with weak China and rising market demand) will trigger the futures curve to shift to a contango setting – that means costs for later supply are larger than spot or near-term supply costs. As soon as this happens, oil can be transported in mass again into tanks world wide resulting in very excessive utilization of tanker ships. Once more, this larger utilization of tankers both from satisfying international demand or restocking of oil can happen in two eventualities (bullish oil costs OR bearish oil costs).

The rationale a contango curve construction – that means larger anticipated future costs than near-term or spot costs permits restocking is – an oil refiner or dealer can lock into promoting oil at a specified worth at a specified date. If the futures curve permits this specified worth at a future date to be larger than the present worth, the dealer or refiner can restock now. Because it stands presently, they can’t, because of a downward sloping futures curve that means costs are anticipated to be decrease in 1, 3, 6 or 12 months from now.

With costs anticipated by the futures market to be decrease in a number of months, it begs the query, why restock now particularly if one can not hedge into the next promoting worth? And that’s exactly why you will have seen big oil stock attracts over 2021 and into 2022 and contributed vastly to continued excessive costs. I’m fairly actually shocked the draw part has been so extended, as finally even these bullish oil should look to the discounted again finish of the WTI futures worth curve as a deep worth play which would chop the backwardation as shopping for longer-dated futures pushes up the back-end relative to the near-term supply or front-end.

Lastly concerning sanctions not regarding Russia, however to Iran and Venezuela, if both are relaxed or lifted (and there have been optimistic developments on Venezuela, much less so just lately with Iran), it might contain elevated scrapping of older and non-compliant or unlawful tonnage/ships in addition to extra provide to be transported through regulated and authorized vessels akin to these owned by main tanker corporations.

In conclusion, I price Petrobras a promote and DHT a powerful purchase.

")

")

{kind=link}