Lisa-Blue

Ormat (NYSE:ORA) is a uncommon asset in that it is without doubt one of the few large-scale geothermal house owners that’s publicly traded, and principally targeted on geothermal. A lot of the different giant geothermal house owners are both state-owned, or half of a giant group the place geothermal represents solely a small share of their operations. That makes Ormat stand out, because the 2nd largest geothermal proprietor & operator on the planet. This explains to a big diploma its excessive valuation.

Geothermal is an attention-grabbing know-how in that it has the very best capability issue of any renewable useful resource, and due to this fact enhances properly with different extra intermittent renewable vitality applied sciences, equivalent to photo voltaic and wind. It might contribute base-load energy with excessive reliability. In Ormat’s case, it owns & operates a mixed ~1.1GW of geothermal energy, storage, photo voltaic PV & Recovered Vitality Era. Ormat operates three most important companies, Electrical energy, Product and Vitality Storage. The Electrical energy enterprise generates electrical vitality and is chargeable for about 88% of income, Product sells geothermal know-how and providers to 3rd events, representing about 8% of income. The Vitality Storage enterprise makes a speciality of storing electrical vitality and represents about 5% of income, it’s the phase anticipated to develop the quickest, nonetheless. Roughly 72% of Ormat’s income comes from the US, with the remaining 28% from worldwide markets.

Market Measurement

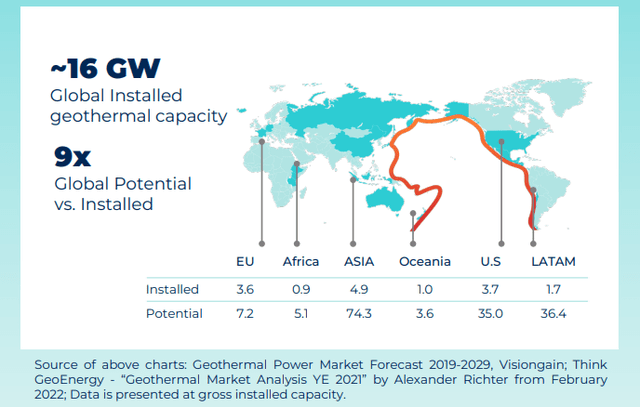

There are at present ~16GW of geothermal put in all over the world, however the potential is huge, estimated at 9x versus what at present exists. Simply within the subsequent two years ~1,250 MW of geothermal binary capability is predicted to be launched. This development is what makes Ormat attention-grabbing, as it’s anticipated to learn considerably.

Ormat Investor Presentation

Financials

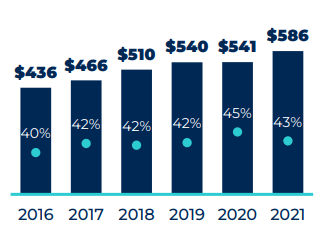

To date, the corporate has delivered some income development and modest gross margin growth. In 5 years, income grew from $436 million to $586 million, a ~6% CAGR. In the meantime gross margins improved ~300bps to round 43%.

Ormat Investor Presentation

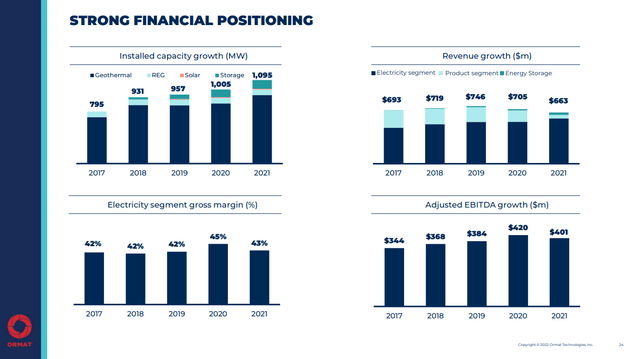

We discover these outcomes a little bit disappointing provided that the corporate grew its put in capability throughout the identical occasions interval from ~795 MW to 1,095 MW. What appears to have occurred is a pointy decline within the Product phase, the one which sells know-how and providers to 3rd events. This phase was once very important round 2017, however its contribution was considerably lowered in 2021. From the corporate’s commentary, their development ought to come primarily from Vitality Storage and Electrical energy, we due to this fact should not anticipating a rebound from the Product phase.

Ormat Investor Presentation

Progress

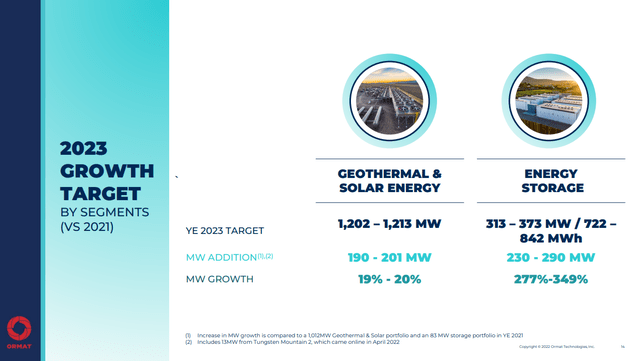

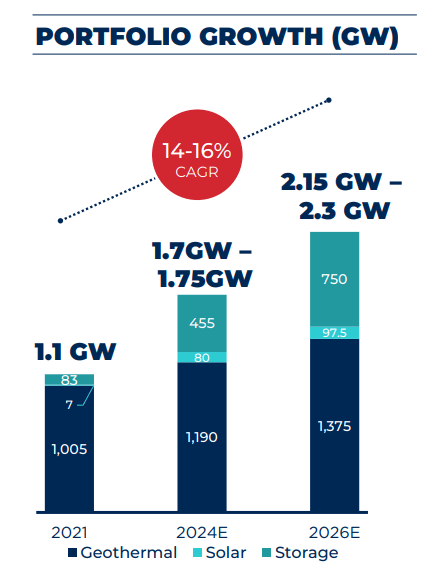

Ormat is anticipating a big enhance in Photo voltaic and Geothermal capability and explosive development in Vitality Storage. It’s focusing on a year-end 2023 portfolio of 1.5GW to 1.6GW, which might signify development vs 2021 of between ~38% to 45%.

Ormat Investor Presentation

The corporate doesn’t count on to cease there, however as a substitute to proceed rising at a 14-16% CAGR, which might translate right into a portfolio of near 2.3 GW by 2026. That might mainly double the dimensions of the corporate’ property in 5 years. As may be seen, a lot of the development is predicted to come back from Vitality Storage.

Ormat Investor Presentation

Steadiness Sheet

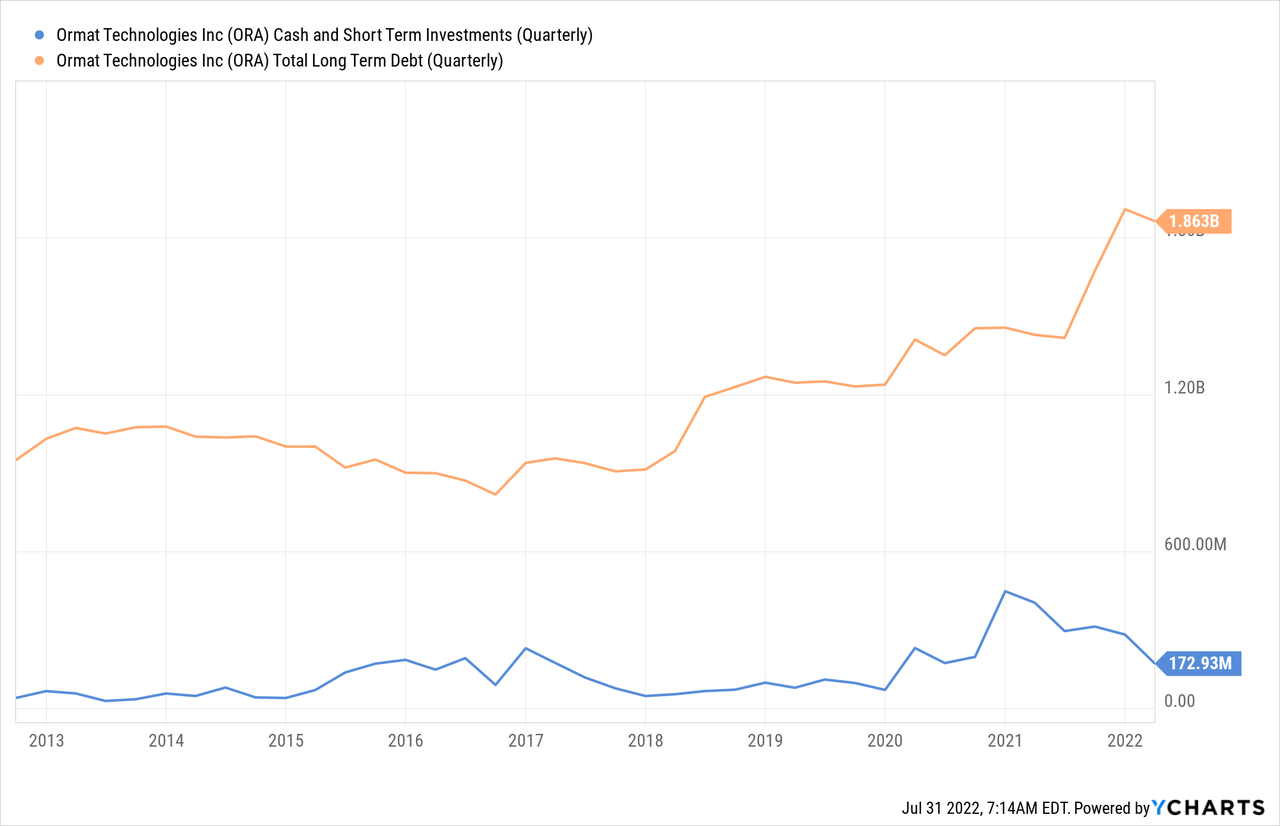

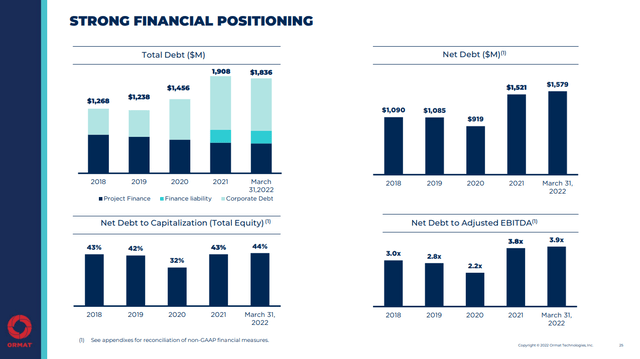

Ormat has been leveraging its steadiness sheet to finance its development, and that has resulted in long-term debt approaching $2 billion.

That is nonetheless very manageable for the corporate because it leads to a web debt to adjusted EBITDA of ~3.9x. Nonetheless, provided that a lot of the debt enhance was company debt we might not need this to broaden a lot additional, particularly since web debt to capitalization is already ~44%.

Ormat Investor Presentation

Valuation

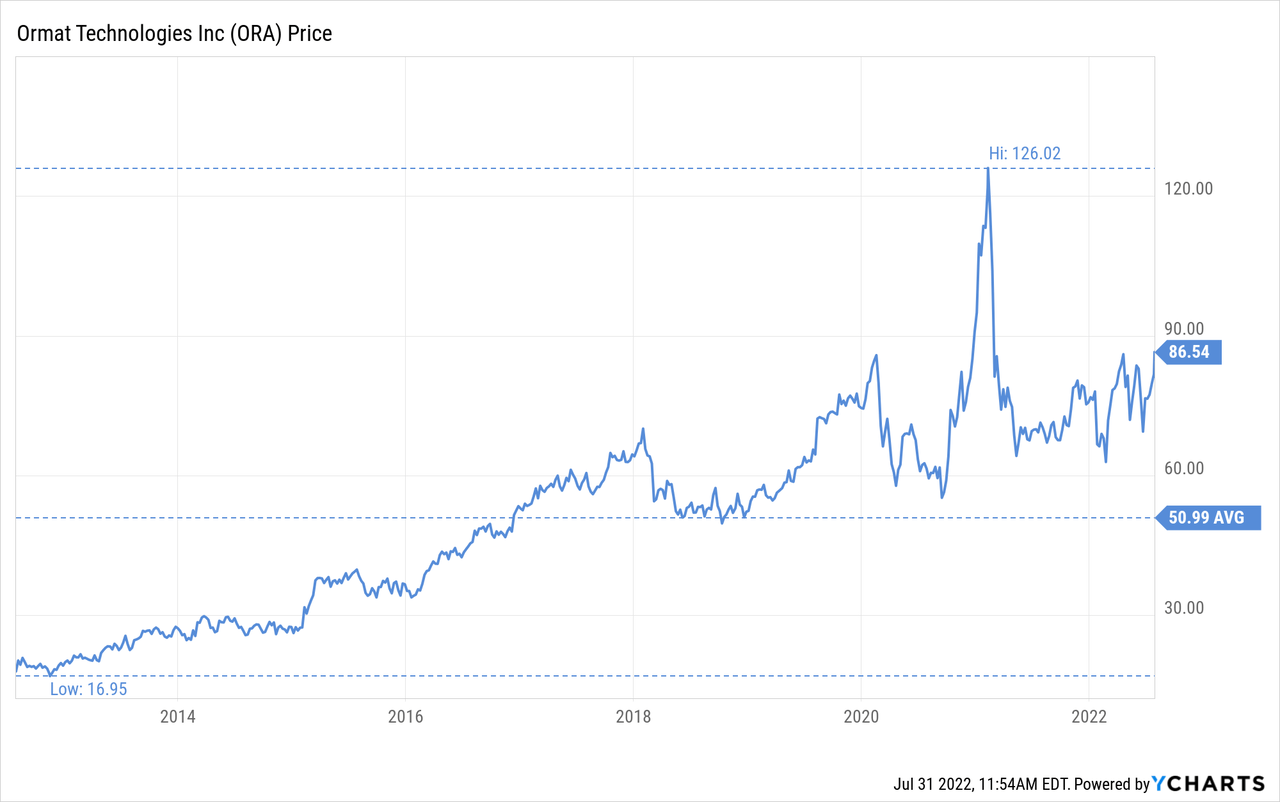

Shares have considerably elevated within the final ten years, from a low of ~$16 to a present share worth round $86.

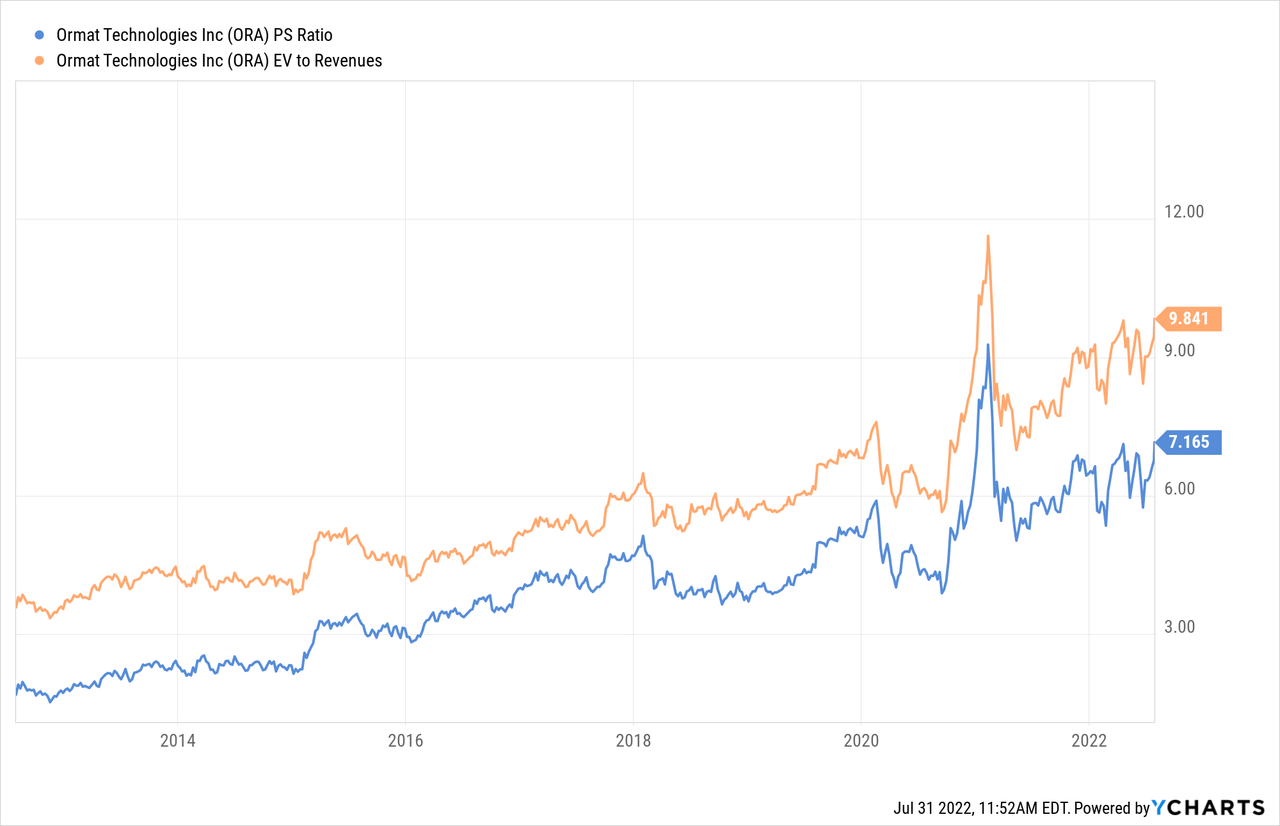

The issue we’ve got is that quite a lot of that development has merely been a number of growth. For instance, EV/Revenues have expanded from a little bit over 3x, to greater than 9x at present.

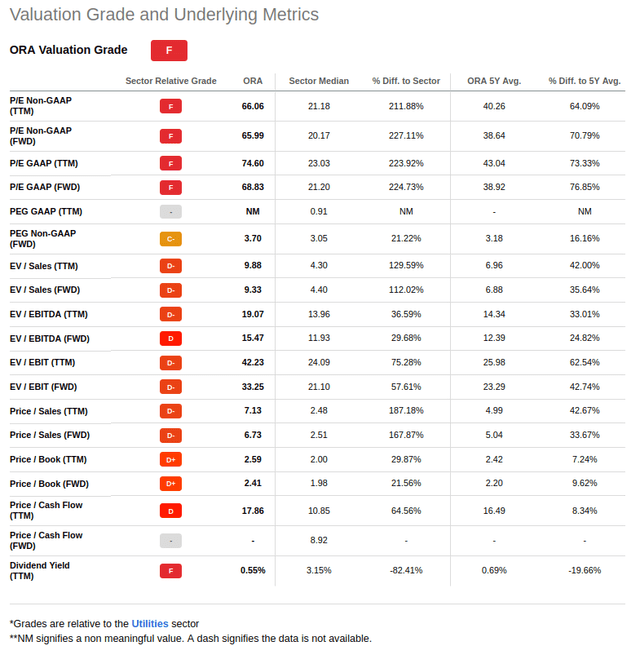

Taking a look at most valuation metrics for the corporate on In search of Alpha we are able to see that they inform the identical story. We imagine a number of the extra related ones are worth/money move, which at 17.8x is about 64% above its utility sector common, and EV/EBITDA which at ~19x is about 36% increased than the utility sector common.

In search of Alpha

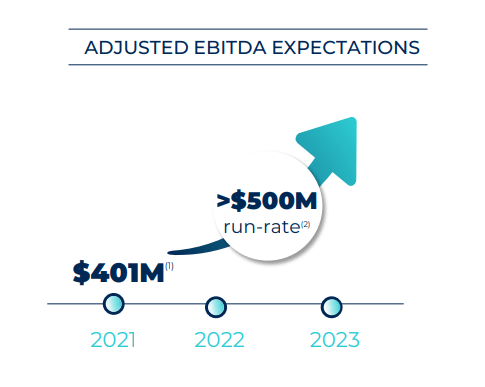

Ormat has a pleasant development story, and EBITDA is certainly anticipated to broaden considerably, however we don’t imagine such premium to different utilities is warranted. On the optimistic aspect, adjusted EBITDA is predicted to succeed in an annual run-rate of greater than $500 million by the top of 2022.

Ormat Investor Presentation

So how a lot do we expect shares needs to be value? We estimate a web current worth of the earnings stream of $65, which might put the shares at ~20% overvalued at present. Discover we’re estimating robust earnings development, and we’re utilizing a comparatively low low cost price of seven.5%, so we imagine we’re being comparatively optimistic with our assumptions.

| EPS Estimate | Discounted @ 7.5% | |

| FY 22E | 1.31 | 1.22 |

| FY 23E | 1.90 | 1.64 |

| FY 24E | 2.25 | 1.81 |

| FY 25E | 2.59 | 1.94 |

| FY 26E | 2.98 | 2.07 |

| FY 27E | 3.42 | 2.22 |

| FY 28E | 3.94 | 2.37 |

| FY 29E | 4.53 | 2.54 |

| FY 30E | 5.20 | 2.71 |

| FY 31E | 5.99 | 2.90 |

| FY 32 E | 6.88 | 3.11 |

| Terminal Worth @ 3% terminal development | 98.33 | 41.28 |

| NPV | $65.82 |

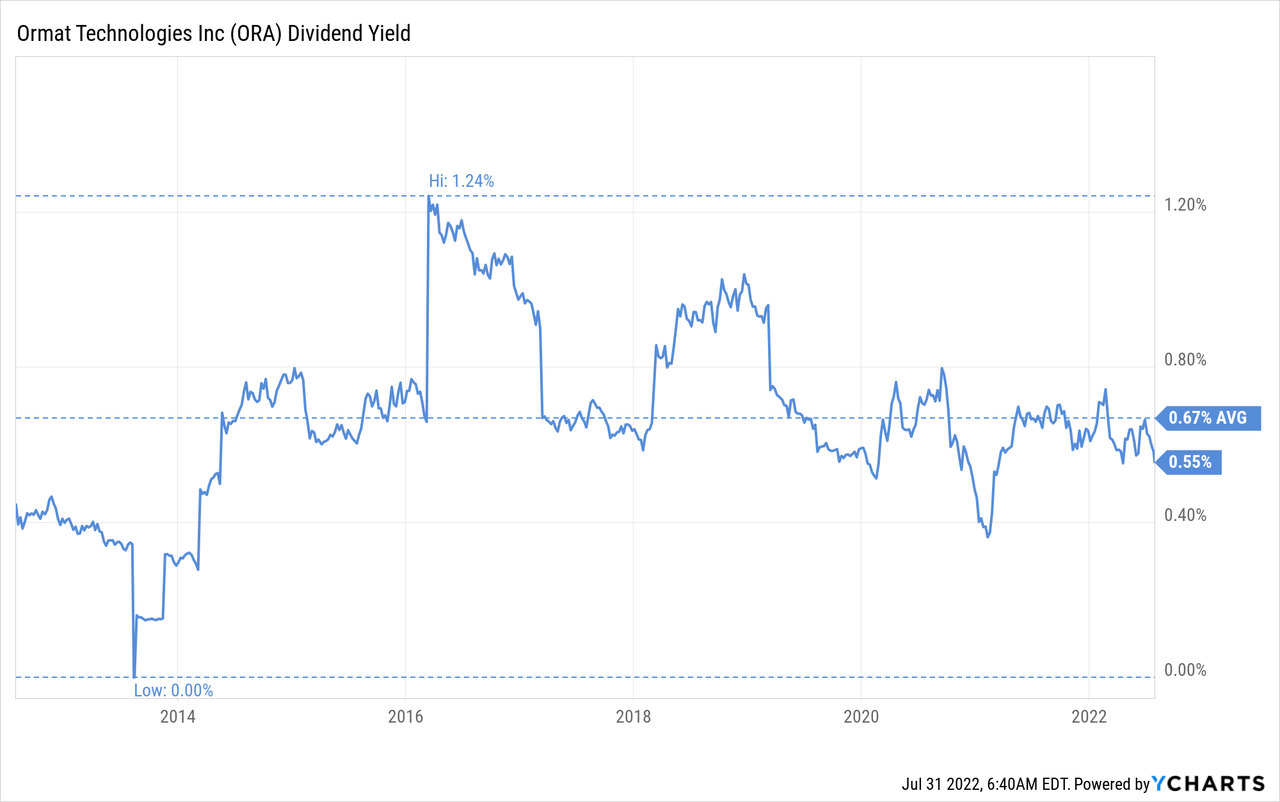

The corporate does pay a small dividend, however given the low payout and excessive share worth, the dividend yield is tiny, at present ~0.55%.

Dangers

We imagine that the principle threat from an funding in Ormat is the excessive valuation, which may considerably right if development disappoints even barely. There may be additionally steadiness sheet threat given the rise in long-term debt, however at this level we imagine it’s nonetheless fairly manageable. Thankfully, the know-how threat is low given how lengthy Ormat has been growing and working these kinds of property.

Conclusion

We like Ormat’s development story, particularly the explosive development that the corporate is anticipating in its Vitality Storage phase. That mentioned, we aren’t ready to pay an enormous valuation premium to the utilities sector. We estimate shares to be about 20% overvalued at present and would want to see a wholesome worth correction earlier than contemplating the shares. We plan on persevering with to comply with the corporate, see how its development develops, and hopefully there might be a horny entry worth sooner or later.

")

{kind=link}