The Debasement Commerce is the brand new buzzword on the town. As not too long ago as final Thursday, legendary investor Ray Dalio and founding father of Bridgwater associates, one of many world’s largest and most-famous hedge funds, termed gold because the “most secure cash.” A month in the past, he had additionally defined why present instances are just like the early Seventies and traders should maintain extra gold than common. Morgan Stanley’s CIO Mike Wilson additionally mentioned a month in the past that he now prefers a portfolio allocation of 60 (equities)/20 (mounted revenue) / 20 (gold) portfolio versus the long-established 60/40 portfolio of 60 per cent in equities and 40 per cent in mounted revenue. He phrases gold because the “anti-fragile asset to personal, fairly than Treasuries.” The listing goes on.

And all these shifts in views are taking part in out after gold has already been the outperformer this decade vs different asset lessons, together with equities. Their feedback additionally sign that their a part of the world is comparatively underinvested in gold.

However for the gold bugs and the macro purists, this might be hardly stunning in any respect. In spite of everything, the only resolution is all the time the most effective! The Occam’s Razor or Precept of Parsimony, as it’s referred to as, would have labored brilliantly as in different instances too, if one had utilized this logic in investing throughout the throes of the Covid assault 5 years in the past. Exponential period of time, cash and efforts have been expended in making an attempt to forecast which shares would do effectively over the subsequent few years. Whereas a few of these forecasts labored, some failed spectacularly, and lots of have underperformed gold. A gush of cash printing and financial uncertainty then have been clear structural components that may have made gold the only resolution for funding. Complication of geopolitics, for the reason that begin of the Russia-Ukraine struggle and US-China rivalry/tensions, added extra momentum to the beneficial tide.

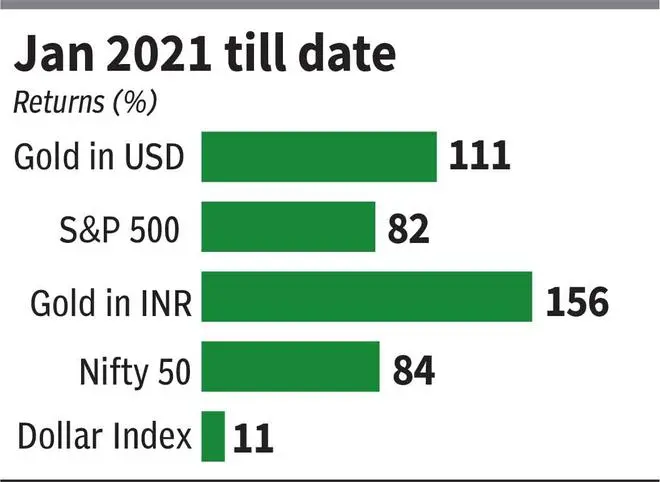

The query that many have now although is, whether or not the 12 months so far run-up in gold (in USD) of 53 per cent, following a 48 per cent upside in 2024 is rational? Whereas after such a run, there will likely be excessive volatility and corrections, as now we have seen within the final two weeks, our take is that the run-up is essentially rational. In our article titled ‘Goldilocks Second for Gold’ in bl.portfolio version dated March 17, 2024, we had laid out threadbare why the outlook for the yellow metallic was rosy and it remained a gorgeous funding for long-term traders even supposing it was buying and selling at its all-time excessive of $2,182 at that time limit. With 83 per cent returns in USD phrases within the 20-month interval since then, we consider whereas the most effective entry level is clearly behind, the case nonetheless exists that gold is more likely to outperform equities when one takes two-three 12 months perspective from right here – whichever the route of the asset lessons. This suggests that on a relative foundation, its attractiveness vs equities stays and traders who need to stay closely invested can contemplate rising allocation to gold as in comparison with equities of their portfolio.

In a two-part collection (within the present and subsequent bl.portfolio editions), we’ll clarify why the case for gold’s outperformance over equities exists.

Historical past of gold within the up to date period

There may be few fields of human endeavour wherein historical past counts for thus little as on this planet of finance. Previous expertise, to the extent that it’s a part of reminiscence in any respect, is dismissed because the primitive refuge of those that don’t have the perception to understand the unimaginable wonders of the current. – John Kenneth Galbraith

To know the place gold is headed within the present decade, it is very important perceive the historical past of gold within the up to date period. That gold is a superb retailer of worth is effectively borne by 5,000 years of historical past, however the pulls and plugs that affect its efficiency may be understood by analysing its decadal efficiency vs different asset lessons within the up to date period.

The Seventies

The ‘Me’ decade was well-known and notorious for a lot of issues — the cultural shift in US to self-focus and individualism over social activism, finish of the Vietnam struggle, the Watergate scandal and extra. However probably the most defining components from an financial standpoint have been the Nixon Shock, Federal Reserve mis-steps, West Asian conflicts, oil embargo and the Iran revolution.

All these mixed created an ideal financial storm and a decade of stagflation within the US that resulted in gold returning a staggering 1,475 per cent returns. Evaluate this to S&P 500 returning simply 47 per cent and underperforming mounted revenue!

Beneath the Bretton Woods system, established in 1944, the US greenback was adopted as the principle international reserve foreign money and was pegged to gold at a hard and fast worth of $35 per ounce. Different main economies that have been a part of the system pegged their foreign money to the US greenback, whereas permitting to fluctuate in a slim band. Because the US financial system underwent some pressures within the late-Sixties and early-Seventies and funds deficits elevated, the strain on the USD elevated. Different nations holding {dollars} as reserves, therefore, had an incentive to transform their greenback holdings into gold as a safer possibility. Extra nations shifting on this route would have resulted in a run-on-the-bank sort of scenario, as greenback peg to gold was based mostly on a fractional gold reserve system and there wasn’t sufficient gold to again all of the {dollars}. Beneath strain, Richard Nixon suspended the gold commonplace on August 15, 1971 and made the USD a fiat foreign money in what’s infamously generally known as the ‘Nixon Shock’.

This brought on the greenback index (DXY) to plunge over 10 per cent within the subsequent few months after being steady at round 120 for a few years until then. Gold costs greater than doubled within the subsequent two years. This was adopted by Yom Kippur Warfare in West Asia and the oil embargo by some Arab nations on these supporting Israel, which included the US. Throughout the round five-month interval of the oil embargo, gold costs shot up by one other 70 per cent, successfully going up practically 400 per cent from the degrees earlier than the Nixon shock. The compounding was effectively on its method and solely accelerated because the US financial system endured a decade of stagflation — sluggish progress/recession and excessive inflation. This was sophisticated by US Fed’s mis-steps. Throughout the early a part of the last decade, the Federal Reserve Chairman at the moment, Arthur Burns, prematurely decreased rates of interest, apparently beneath political strain, which resulted in a resurgence in inflation. With the Iran Revolution of 1978-79 and one other oil shock and better inflation, and after a decade of persistently-high inflation, public confidence that inflation could be introduced beneath management was eroded.

Gold going up 15 instances in that decade was the result of all this mess. Gold’s efficiency in its nice bull-run in that decade may be break up into three elements — 1971 to 1974-end when it was up 400 per cent; 1975 to 1977-end when it was down 6 per cent throughout which it additionally entered bear market territory; and 1978 to 1980-end when it was up 235 per cent.

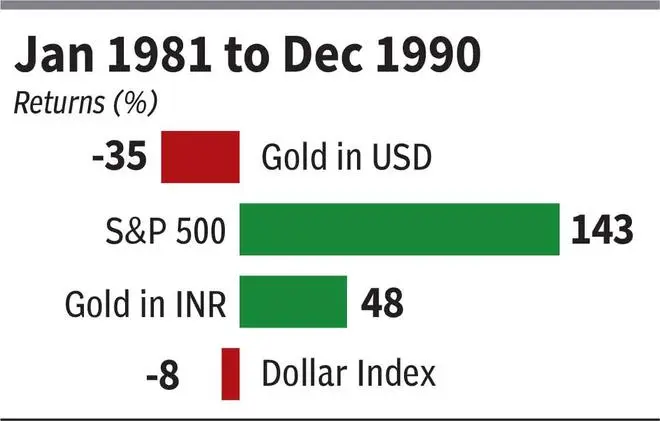

The Eighties

If it took the ‘Nixon Shock’ to ignite the hearth of the gold bull-run, it required a ‘Volcker Shock’ to douse the hearth and restore public confidence in fiat foreign money.

When Paul Volcker took over because the Federal Reserve Chairman in August 1979, inflation within the US was raging at 9 per cent and was trending up over the subsequent 12 months regardless of the central financial institution’s makes an attempt to regulate cash provide. A part of the issue was inflation expectations. By the tip of the Eighties, inflation expectations have been excessive and remained unanchored — after a decade of excessive inflation, it had received into public psyche that top inflation was a everlasting phenomenon they usually had no confidence that financial coverage would rein it. Beneath such circumstances, staff demand greater wages, folks advance shopping for selections beneath the belief that costs could be greater weeks or months later, and firms attempt to elevate costs. Successfully, this behaviour of people and corporates accentuated and exacerbated the inflationary pattern. To quell this and restore public confidence in financial coverage, Volcker delivered a collection of rate of interest will increase, taking it as much as 18 per cent within the Eighties. After modestly reducing it to 16 per cent and never getting the specified consequence, he elevated the rates of interest to twenty per cent in Could 1981, taking the actual rate of interest (Fed Funds Price – CPI inflation) to an unprecedented 10 per cent. This was a placing blow to the financial system. However it was the short-term ache that Volcker felt was required to conquer inflation and restore public confidence in financial coverage. Brief-term ache for long-term good was the commerce he took.

Put up the Volcker shock, throughout 1981-82, the US financial system endured certainly one of its most-severe recessions within the post-World Warfare II period. Unemployment charge went as much as 10.8 per cent in 1982 — the very best for the reason that Nice Despair.

However the good factor: Occasions turned out effective, as Volcker anticipated, on the different finish of the tunnel. Inflation fell from a excessive of 11-12 per cent in 1981 to beneath 4 per cent in December 1982. From then until the tip of the last decade, month-to-month CPI inflation within the US averaged 3.9 per cent versus 8 per cent within the earlier decade.

Along with his measures, Volcker put an finish to the good gold bull-run for the subsequent 20 years. When actual rates of interest are taken as much as as excessive as 10 per cent, prefer it was for some time in 1981, mounted revenue is way more engaging than gold or equities. Within the 12 months of the Volcker Shock alone, gold fell 33 per cent; S&P 500 fell 10 per cent.

A couple of months later in 1982 is when a terrific bull market began for US equities that prolonged for practically 18 years and culminated within the dotcom bubble of 2000.

One exception to the reversal of the pattern on this decade was the greenback index, which truly fell 8 per cent. This was due to Plaza Accord — the US negotiated an settlement with a couple of different nations corresponding to Germany and Japan, beneath which their currencies would admire towards the greenback. This was accomplished to cut back the US’ excessive commerce deficit, one thing that Trump is making an attempt to repair immediately with tariffs.

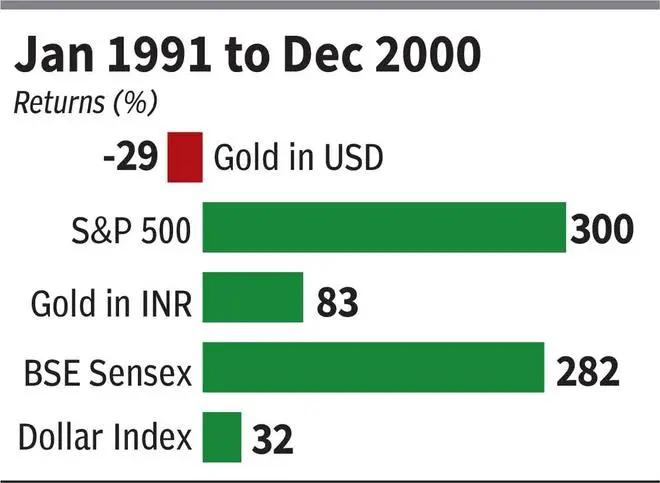

The Nineteen Nineties

The defining occasion that additional led to gold underperforming on this decade was the tip of the Chilly Warfare in December 1991. The best geopolitical risk of the earlier 45 years was eradicated with this, heralding the beginning of a brand new period of an unipolar world with the US as the only real superpower.

It was a horrible decade for gold, throughout which it fell 29 per cent atop a decline of 35 per cent within the prior decade. Low inflation (common month-to-month CPI of two.8 per cent for the last decade), decrease rates of interest, the dotcom revolution and US hegemony, and, in fact, euphoric traders — all contributed to a stellar decade for US shares, wherein the S&P 500 was up 300 per cent.

The opposite essential side of this decade that must be strongly famous is one thing that’s apparently anathema to developed market governments in current instances — balancing the funds. By the tip of the last decade, the then US President Invoice Clinton truly balanced the funds and raked in a surplus! Sure, he truly did that! Accountable authorities spending and low inflation – the type of issues that strain gold costs, mirrored in its underperformance. The greenback index surged 32 per cent within the decade.

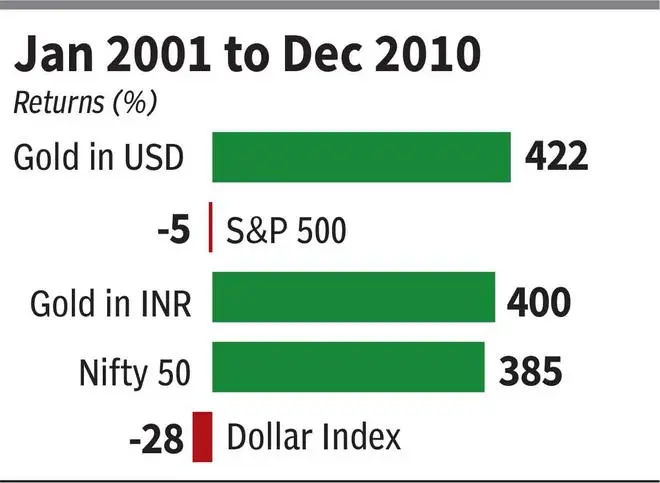

The 2000s

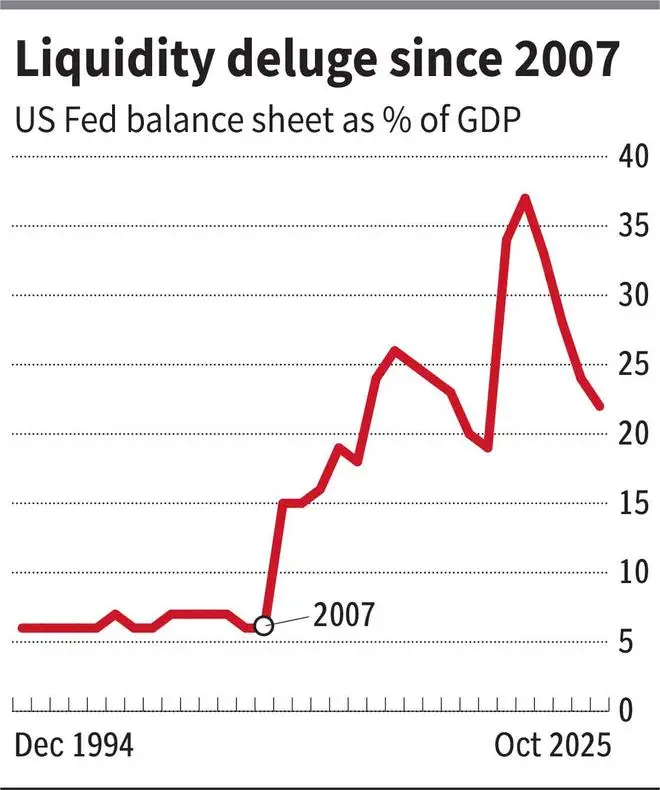

After a two-decade lull, this was the last decade that sowed the seeds for the present gold bull market. After the dotcom bust and recession that adopted, the US Fed, beneath Alan Greenspan, launched into a brand new period of straightforward cash to stimulate the financial system. Extremely-low rates of interest, vital deregulations and unfastened lending requirements within the monetary sector that brought on a credit score growth, and the beginning of a brand new authorities spending binge offered the right gasoline to ignite a brand new gold bull-run. Later within the decade, international central banks embarking on a brand new period of quantitative easing (QE) was jet gasoline for the yellow metallic.

Mainly, this decade noticed the reversal of the accountable authorities spending applied by Invoice Clinton within the Nineteen Nineties and accountable central banking applied by Paul Volcker. There must be no shock that gold was in favour once more. The stellar run of gold, which returned 422 per cent within the decade, may be break up into two elements: Pre-QE interval (2001-07) and post-QE interval (2007-10) throughout which it returned 206 per cent and 70 per cent respectively. The entire interval was a washout and a misplaced decade for US equities with the S&P 500 returning damaging 5 per cent.

The restoration from the lows of the dotcom bust was totally overturned with the onset of the worldwide monetary disaster, like in a snake and ladder recreation.

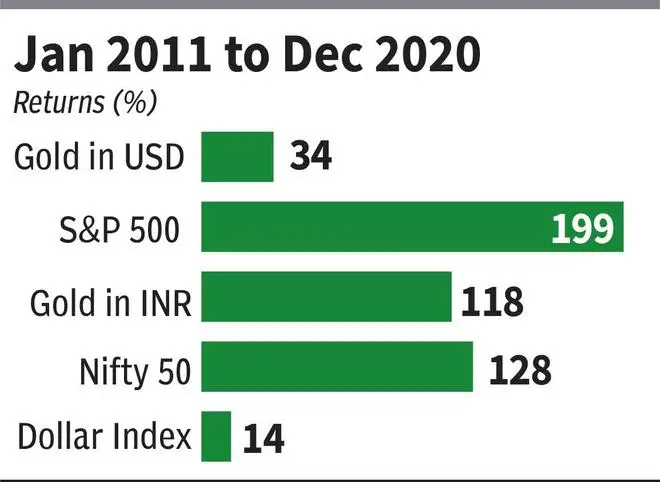

The 2010s

From a macro-economic perspective, one of many most-defining traits of this decade was the confoundingly-low rates of interest regardless of unfastened central financial institution insurance policies and expansionary fiscal insurance policies. Low long-term bond yields as a consequence solely emboldened governments to tread additional on the spending binge. Whereas there isn’t a clear rationalization for this, causes attributed are improvements made attainable by technological developments, international commerce and exports from low-cost locations, a requirement shock to elements of economies because of the international monetary disaster and the eurozone disaster.

Therefore, this was an uncommon decade the place despite a deluge of liquidity, inflation was low. It was a wonderful decade for equities, whereas gold underperformed in USD phrases though beating inflation solidly with its 34 per cent returns.

The present decade

Because the saying “You’ll be able to run, however you can’t disguise” goes, cash printing can go on for a decade with out penalties, however finally it catches up. That appears to be the message within the present decade after the fiscal profligacy following the onset of the Covid pandemic and the ultra-loose central financial institution insurance policies let the inflation genie out of the bottle. The issue seems to have gotten sophisticated extra because of the unwarranted prolonged fiscal and financial stimulus, even after economies had began recovering from the Covid shock. At this time, as in comparison with low rates of interest within the prior decade, developed market central banks are confronted with inflation persevering with to maintain above their targets. Within the US, inflation has trended above the Federal Reserve’s goal of two per cent for 54 consecutive months and is more likely to stay so for a lot of extra months. Whereas there won’t be any official acknowledgement, the US Federal Reserve has failed in its financial insurance policies —just like what occurred within the Seventies.

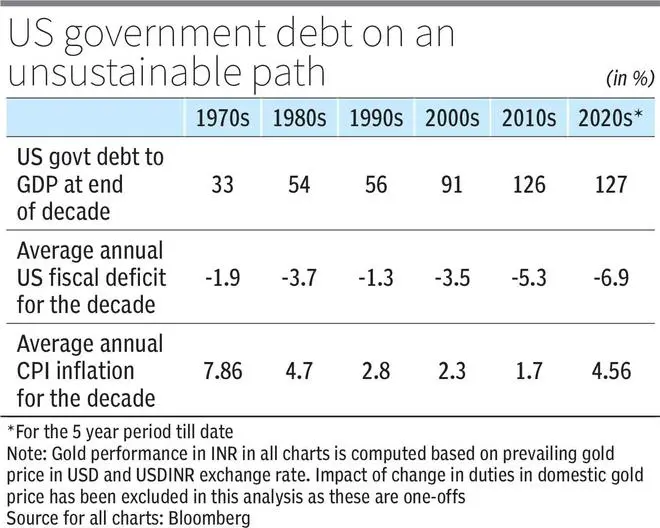

This is without doubt one of the major causes that has pushed the outperformance of gold within the present decade. Add to this, US authorities fiscal deficit at 6-7 per cent, when debt to GDP is at 127 per cent, implies authorities spending is on an unsustainable path.

As if this alone weren’t sufficient, immediately geopolitics is on the most uncomfortable ranges within the post-Chilly Warfare period – a key issue pushing central banks in China and Russia to extend gold holdings.

As Ray Dalio has mentioned, the traits within the present decade replicate a confluence of things just like what transpired within the Seventies.

The necessary factor for traders word right here from the charts – nice many years for gold have been poor many years for S&P 500 and vice-versa.

Nevertheless, unhealthy many years for gold in USD, has not been unhealthy for Indian traders in gold given rise in greenback index/rupee depreciation. This makes case to extend allocation to gold as in comparison with equities.

For the gold bull-run to finish, it requires governments and central banks to do the suitable factor. One thing like what Paul Volcker and Ronald Reagan did within the Eighties or Invoice Clinton did within the Nineteen Nineties with regard to authorities funds. It might not be too troublesome to conclude for now that Jerome Powell isn’t any Paul Volcker and Trump isn’t any Invoice Clinton in relation to authorities funds. In that context, whereas gold might transfer up or down or be range-bound, the bull-run stays intact for now.

Printed on November 1, 2025

")

")

{kind=link}