Up to date on October seventeenth, 2024 by Felix Martinez

The Keg Royalties Revenue Fund (KRIUF) has two interesting funding traits:

#1: It’s a high-yield inventory primarily based on its 7.5% dividend yield.

Associated: Listing of 5%+ yielding shares.

#2: It pays dividends month-to-month as a substitute of quarterly.

Associated: Listing of month-to-month dividend shares

You’ll be able to obtain our full Excel spreadsheet of all month-to-month dividend shares (together with metrics that matter, like dividend yield and payout ratio) by clicking on the hyperlink beneath:

The mix of a excessive dividend yield and a month-to-month dividend render The Keg Royalties Revenue Fund interesting to income-oriented traders.

However there’s extra to the corporate than simply these elements. Maintain studying this text to be taught extra about The Keg Royalties Revenue Fund.

Enterprise Overview

The Keg Royalties Revenue Fund is a limited-purpose fund that owns the Keg logos and associated property bought from Keg Eating places Ltd (KRL). Keg Eating places has constructed a premier steakhouse model in Canada and a longtime presence in the USA.

The fund owns the rights to the model and has granted KRL an unique license to make use of the Keg Rights in trade for a month-to-month royalty cost equal to 4% of the product sales of Keg eating places.

In return for including eating places to the fund’s royalty pool, KRL receives the precise to amass models within the fund. KRL’s efficient possession of the fund has grown from 10.00% on the time of the IPO in 2002 to over 33.%% as of the top of 2023. Therefore, the pursuits of the 2 entities are well-aligned.

The Keg Royalties Revenue Fund stands out as a “top-line” fund, with its income stemming predominantly from KRL’s restaurant gross sales and solely minor working and financing bills curbing its web earnings. Moreover, the fund advantages from a secondary supply of earnings – a $57.0 million Keg Mortgage, which generates curiosity earnings at a fee of seven.5% every year, paid month-to-month.

This distinctive construction shields the fund from the fluctuating earnings and bills related to truly operating the eating places. Consequently, the fund enjoys safety from inflation and a comparatively predictable stream of royalties and curiosity, amongst different advantages.

Progress Prospects

Just like different royalty funds of its kind that we now have analyzed, just like the Boston Pizza Royalty Revenue Fund and the A&W Income Royalties Revenue Fund, the fund’s progress prospects and total efficiency hinge on simply two key elements. The primary is the variety of franchised eating places in its royalty pool, whereas the second is the speed of progress in same-restaurant gross sales.

For context, at the beginning 0f 2004, the fund had 86 Keg eating places in its royalty pool. By the top of 2007 and 2013, this quantity had grown to 95 and 102, respectively. Since then, exercise within the royalty pool has been somewhat stagnant. On the finish of 2020 and 2021, the fund had 106 eating places in its pool, whereas by the top of 2023, it had added yet one more to its rely of 105.

We count on only a few annual additions to the fund’s royalty pool, because it seems the model has reached peak scaling potential. Compared to the Boston Pizza and A&W Royalty Funds, which primarily give attention to fast-food manufacturers and provide extra vital progress potential, Keg’s high-end eating expertise is extra tailor-made to a smaller and extra specialised demographic, leading to a extra contained enlargement functionality.

That stated, rising same-restaurant gross sales nonetheless poses a progress catalyst for the fund. In 2019, earlier than the COVID-19 pandemic, there have been 105 Keg eating places within the fund’s royalty pool, producing about C$623.7 million in product sales, or C$5.94 million per restaurant.

Consequently, the final six months, the fund recorded about C$14.257 million (purple field) in royalty, which is strictly 4% of the underlying gross restaurant gross sales within the royalty pool. It additionally recorded an extra $2.177 million in curiosity earnings from its 7.5%-yielding mortgage, as talked about earlier. You too can see the distributions paid to KRL comparable to its possession within the fund and different developments paid for upcoming restaurant openings.

Supply: Annual Report

Future value will increase in keeping with inflation ought to slowly however steadily add to the fund’s royalty-eligible product sales generated by KRL. In fact, foot site visitors within the firm’s eating places and/or restaurant openings and closings may sway outcomes, both.

The corporate reported its monetary outcomes for the second quarter and the primary half of 2024, displaying blended efficiency. Royalty Pool Gross sales elevated by 2.3% within the second quarter to $175.2 million, however decreased by 1.8% year-to-date, totaling $356.4 million. Equally, Keg Eating places Ltd.’s (KRL) common gross sales per working week noticed a 2.3% rise within the quarter, however dropped by 1.2% for the yr. Regardless of a decline in visitor visits, same-store gross sales have been up 1.7% within the quarter however down 1.9% year-to-date.

Royalty earnings for the quarter elevated by 2.3% to $7.0 million, although it fell 1.8% year-to-date. Distributable money, a key indicator of monetary well being, decreased by 4.3% to $0.282 per Fund unit for the quarter however rose by 8.9% year-to-date. The Fund paid out a particular money distribution of $0.08 per unit in January 2024, contributing to a payout ratio of 100.8% for the quarter and 82.1% year-to-date.

Regardless of these fluctuations, the Fund stays financially secure, with $2 million in money and a optimistic working capital stability of $3.7 million. Administration stays optimistic, attributing the optimistic quarter outcomes to operational efficiencies and a robust visitor expertise. KRL plans to give attention to advertising efforts and enhancing visitor demand by way of the rest of 2024.

Dividend Evaluation

Aligned with the fund’s intention to distribute all its income to unitholders, the payout ratio has constantly hovered across the 100% mark. In 2023, it stood at 87%, whereas in 2021, it was 121.5%, owing to the fund’s determination to disburse additional money that had been held again in 2020 because of the pandemic, which had resulted in a payout ratio of simply 85.9% on the time. Nonetheless, since its inception, administration estimates that 99.78% of distributable money has been distributed.

Buyers shouldn’t count on distribution will increase or distribution “cuts”, however as a substitute count on that every yr’s whole distributions per unit will differ primarily based on the underlying product sales of Keg-licensed eating places.

We see restricted distribution progress prospects transferring ahead, in keeping with our rationale relating to the fund’s total progress. Other than greater pricing through the years, we will see the fund producing roughly stagnant earnings and thus paying out somewhat stagnant distributions.

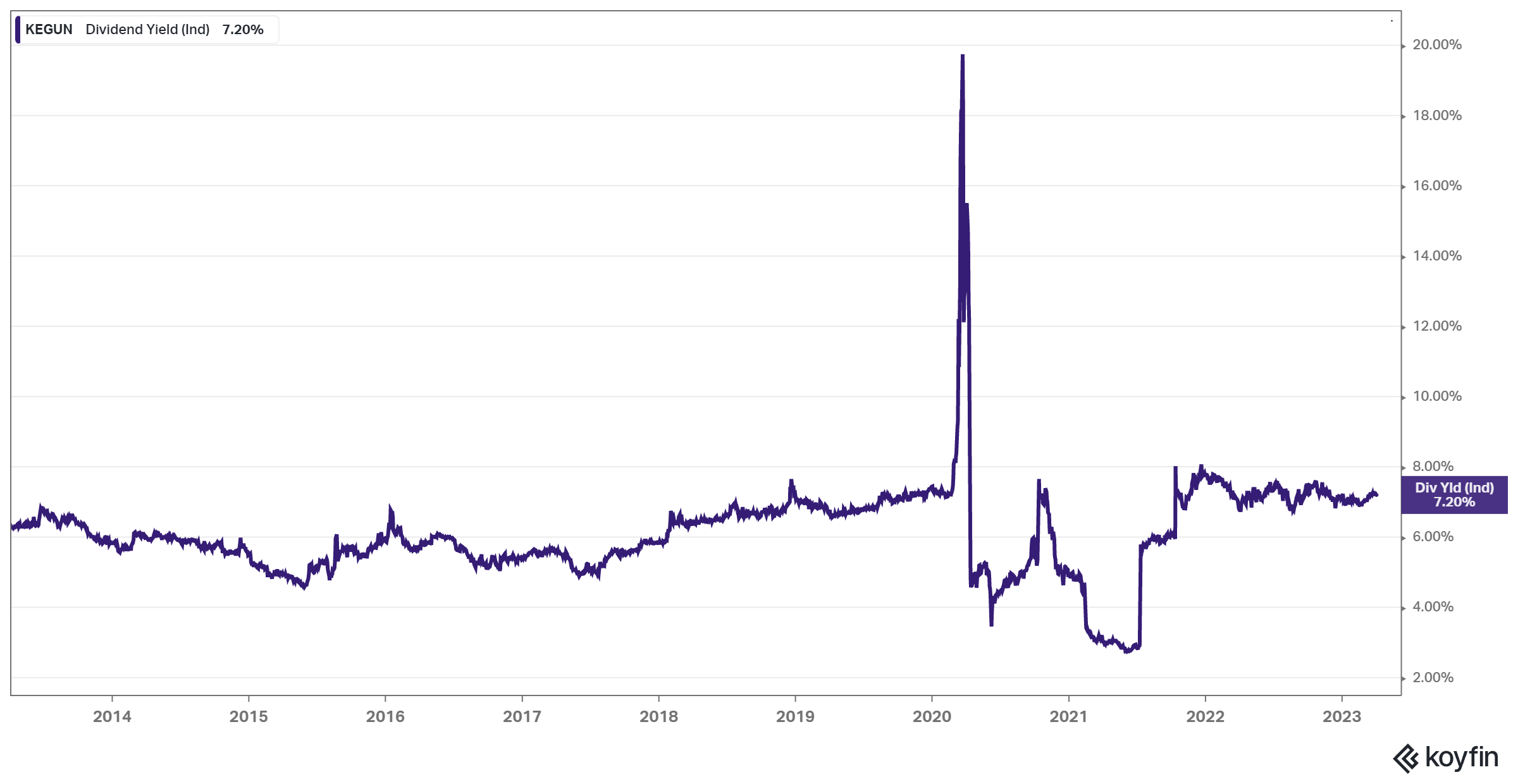

The present month-to-month distribution of C$0.09 interprets to an annualized fee of C$1.08 (or US$0.78), implying a yield of seven.5%. This yield is somewhat substantial, but it surely additionally displays traders’ expectations for restricted dividend progress prospects.

Supply: Koyfin

It’s value highlighting that the administration’s method seems to contain dividing the quarterly or yearly distributions into equal sums by forecasting the forthcoming money flows, thereby making a uniform distribution fee and making certain consistency in payouts month after month.

Ultimate Ideas

The Keg Royalties Revenue Fund affords a hefty dividend yield, which, together with the extremely engaging frequency of its month-to-month payouts, makes it a compelling decide for income-oriented traders.

Its frictionless income mannequin, which is straight tied to the restaurant’s product sales in its royalty pool, affords safety from inflation and a reliable stream of income, no matter every particular person restaurant’s profitability.

Supplied that the Keg model doesn’t considerably change, we anticipate the corporate will proceed to generate a secure stream of month-to-month distributions by way of dependable royalty and curiosity earnings.

Nevertheless, in comparison with different trusts of this sort we now have analyzed, we anticipate that the scope for distribution progress is comparatively restricted because of the paucity of recent restaurant openings and the potential saturation of the model.

Consequently, traders ought to put together for the majority of their returns to come back from the dividend. Taking this under consideration, we consider the fund is not going to obtain annualized returns exceeding the mid-to-high single digits, which is in keeping with its present dividend yield.

Don’t miss the sources beneath for extra month-to-month dividend inventory investing analysis.

And see the sources beneath for extra compelling funding concepts for dividend progress shares and/or high-yield funding securities.

Thanks for studying this text. Please ship any suggestions, corrections, or inquiries to [email protected].

")

")

")

{kind=link}