Abu Hanifah/iStock via Getty Images

Co-produced with Treading Softly.

When the Oakland A’s wanted to assemble an effective and playoff-worthy team, they struggled to compete against teams who could afford a higher salary for their players. The traditional logic of throwing millions of dollars at their problems wouldn’t work – they simply didn’t have the money to do it.

In 2002, the general manager of the Oakland A’s decided to try building a team using a different methodology. Instead of chasing “the best” and trying to outbid others, the method sought to identify undervalued players. It was new, unknown, and misunderstood method. It lead them to have a record-breaking 20-game-winning streak and eventually reach the American League Division Series – one step away from the finals.

His efforts are chronicled in the movie and book Moneyball.

When it comes to investing, the misunderstood or unknown investment opportunities often bear higher yields due to that status. My team and I seek out these investments using our own unique methodology to unlock the unseen values and income from the market.

Today, I want to look at two of these opportunities.

Let’s dive in!

Pick#1: AGNC – Yield 14%

(This report was first published to HDO subscribers on December 3rd, and all data is from that date.)

Investing in hindsight is easy. October 24th, 2022, was the day to buy AGNC Investment Corp. (AGNC). So go get your time machine fired up and send yourself a message. In just 6 weeks, AGNC has returned 36%, that’s a +300% annualized return!

Of course, on October 24th, nobody knew it was at the bottom. Since then, readers on Seeking Alpha have been advised that they should worry about the “massive” equity issuance, told that AGNC has “unprecedented” value destruction, and told to “learn” from mistakes and avoid AGNC.

All this wailing and gnashing of teeth was over an unrealized loss that AGNC will never realize. The assets they hold, agency MBS, come with a principal guarantee. The “agencies,” Fannie Mae and Freddie Mac, will buy the mortgages back at par value if they are delinquent. The cash flow that AGNC will receive never changed. What changed was the price the market was willing to pay for that cash flow.

In all fairness, we weren’t confident that October 24th was bottom, either. Heck, we still aren’t. Mortgage spreads have compressed over the past month, but there is no guarantee that they keep going in that direction. We wrote to members on October 25th:

So Treasuries are down, and MBS is down relative to Treasuries. The “spread” between MBS and Treasuries is what AGNC profits from. The wider that spread, the more money they are capable of making. The rates they borrow at are tied to Treasuries, and the rates their assets pay them are tied to MBS. When MBS prices are down, it is bad for book value, but it is great for the yield that AGNC earns.

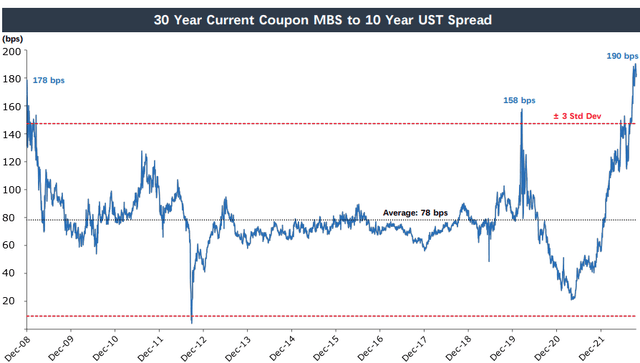

We presented this chart from AGNC that shows the spread as measured by the 30-year Current Coupon MBS and the 10-year Treasury at an eye-watering 190bps. That is higher than it was before the GFC and the highest in AGNC’s history as a public company. Source.

AGNC Q3 Investor Presentation

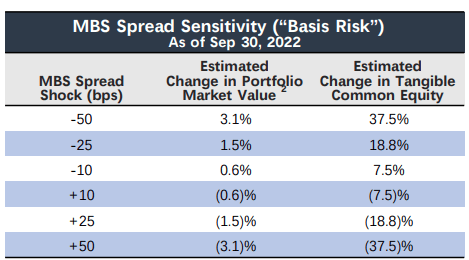

At the time of this writing, this spread has narrowed to 144 bps. While still absolutely wide in a historical sense, this narrowing has likely been a key reason for AGNC’s share price to rally. AGNC predicted, assuming a static portfolio, that a 50 bps tightening of the MBS to Treasury spread would lead to a 37.5% increase in book value.

AGNC Q3 Investor Presentation

While there are other moving parts, likely, AGNC is still trading at a discount to book value. Plus, there is ample room for more upside as MBS spreads trend back to normal.

This kind of volatility shouldn’t be surprising. AGNC has been utilizing the leverage of 7.5x-9x equity, which is actually lower than historical leverage. When you are using that kind of leverage, small changes can have big impacts on book value.

The agency MBS market, along with the Treasury market and other bonds, has seen an unprecedented level of volatility. Here is a look at the 4% Coupon 30-year UMBS prices since 2013 – the largest allocation AGNC has. Note how large the downswing has been relative to history, including COVID. Source.

Mortgage News Daily

This fall is what has been driving AGNC’s book value lower. They own MBS on a highly leveraged basis, and the prices have fallen from a peak of $106.77 to a bottom of $89.58.

Note that when these mortgages are repaid, AGNC will receive par ($100) in every conceivable scenario. Borrower defaults? $100. The borrower sells their house? $100. House burns down, hit by a tornado, flooded, or other destruction? $100. The borrower is eager to pay off the mortgage early? $100.

Can we say that October 24th was a long-term bottom and guarantee that MBS prices and AGNC won’t revisit those depths? No. Predicting the future is a lot harder than predicting the past.

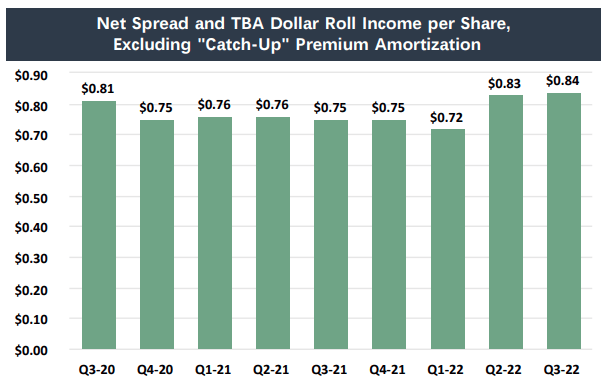

What we can say is that throughout this downturn in book value, AGNC’s earnings have held up and actually hit recent highs in the past two quarters, covering its dividend by over 230%.

AGNC Q3 Investor Presentation

This is why we haven’t spent our time worrying over the past year about the decline in book value. Even as book value declined, earnings went up. It was only a matter of time before MBS prices rebounded, and embedded in every MBS is that it will eventually be redeemed at par 100% of the time. All MBS prices are headed to $100, it’s only a question of how many detours they take to get there.

So while others are out there hyperventilating over unrealized paper losses, we’ll just keep collecting our very realized cash dividends. At peace, knowing that prices will take care of themselves in time.

Pick #2: TRINL – Yield to Maturity 6.6%

(This report was first published to HDO subscribers on December 11th, and all data is from that date.)

Trinity Capital Inc. (TRIN) is a less well-known business development company (“BDC”) focusing on venture capital investments. Unlike others in the space, like SuRo Capital Corp. (SSSS), TRIN focuses primarily on making equipment or senior loans to new and growing companies vs. taking on an equity position.

This allows TRIN to have a more predictable income stream from their holdings. Overall TRIN has a riskier loan profile than long-time High Dividend Opportunities favorites like Owl Rock Capital Corporation (ORCC) or Ares Capital (ARCC). Its portfolio has been effectively managed to maintain strong income, with TRIN’s common shares trading at a discount to book value due to the increased risks in its portfolio.

Let’s take a closer look at their overall portfolio:

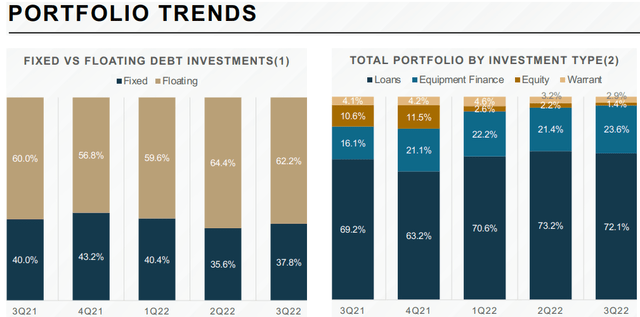

Trinity Capital Presentation Q3

TRIN’s portfolio is heavily weighted towards floating rate debt, with only 1/3rd fixed in its interest yield. This allows TRIN to benefit from recent and coming rate hikes. We’d like to see the fixed interest percentage of loans rise when it appears the Federal Reserve will maintain interest rates before cutting them again. So at this point, their portfolio is attractive with 72% in loans, meaning they are taking a more conservative route in their investments.

TRIN’s debt structure is also attractive.

Trinity Capital Presentation Q3

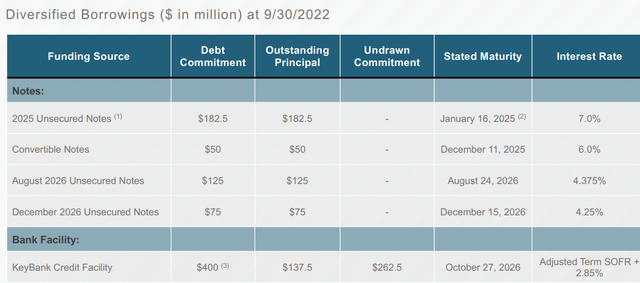

They’ve been able to finance through privately placed notes outside of their 2025 unsecured notes. These private placements were at materially lower interest rates than Trinity Capital Inc – 7% NT REDEEM 16/01/2025 USD 25 (TRINL). Note that TRINL is the next maturity for TRIN, and is the highest yielding, so it will be repaid first.

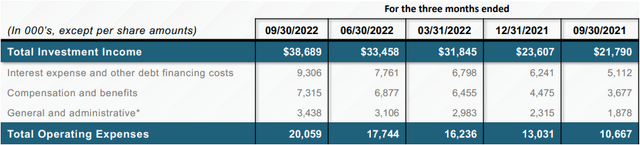

TRIN’s ability to service its debt should not be in question at this juncture either, with earnings easily covering the interest.

Trinity Capital Presentation Q3

They covered their interest expenses by 4.1x with their total investment income and have historically averaged a coverage ratio of over 4x over the trailing year.

So while we think TRIN’s common shares are potentially attractive for an investment, we’d rather lock in a safer high yield from their baby bond offering:

Trinity Capital Inc. 7.00% Notes due 01/16/2025, which has a YTM of 7.0%. Currently, TRINL is TRIN’s highest-cost debt and is easily serviceable by them. TRINL is rated BBB+ by Egan-Jones. Note that TRINL is callable in January 2023.

Do we expect an early call on TRINL? No. In this interest rate environment, it is unlikely that TRIN could refinance with a materially lower coupon. The days of refinancing with coupons in the 4% range are gone until the Fed turns Dovish again. Additionally, TRINs earnings are higher in this environment, so it will not be in a hurry to deleverage.

TRIN has occasionally sold additional bonds in the TRINL umbrella when it trades above PAR. Their proclivity to do this and its near maturity date has helped keep TRINL pinned to its PAR value recently.

Furthermore, its near-term maturity also provides a reduced influence of interest rate hikes on its trading value. TRINL is a good place to store cash that one does not need for a couple of years.

One warning is that TRINL has extremely limited trading volume, so using limit orders and packing an abundance of patience is a must.

Conclusion

With AGNC, you have a readily misunderstood investment opportunity. Others try to gamble and time their investments, we have continued to hold and collect income along the way. AGNC has begun an impressive recovery and I expect it will continue as MBS prices recover and rise upward.

TRINL is an attractive and low-risk place to invest and collect interest income for the next two years. TRIN is a very well-managed albeit less well-known BDC that is richly rewarding its common shareholders. The coverage of its interest expenses remains strong and consistent as TRIN has grown.

As you craft your income or retirement portfolio, you may not have the cash to throw millions into your portfolio and buy T-bills to live off of the tiny interest yield they bear. If you do and can, that’s great for you! However, most of us have portfolios like the Oakland A’s team, we need to look where others aren’t to find opportunities in the misunderstood and unknown players in the field.

It can and will carry your income and retirement to new levels of achievement when done effectively.

Stock: Slow Growth Ahead")

")

— RT World News")

{kind=link}