Revealed on October twenty eighth, 2025 by Felix Martinez

Excessive-yield shares pay out dividends which can be considerably larger than the market common. For instance, the S&P 500’s present yield is just ~1.2%.

Excessive-yield shares will be notably useful in supplementing earnings after retirement. A $120,000 funding in shares with a median dividend yield of 5% creates a median of $500 a month in dividends.

Timbercreek Monetary Corp. (TBCRF) is a part of our ‘Excessive Dividend 50’ sequence, which covers the 50 highest-yielding shares within the Positive Evaluation Analysis Database.

We now have created a spreadsheet of shares (and carefully associated REITs, MLPs, and so forth.) with dividend yields of 5% or extra.

You possibly can obtain your free full checklist of all securities with 5%+ yields (together with vital monetary metrics equivalent to dividend yield and payout ratio) by clicking on the hyperlink under:

Subsequent on our checklist of high-dividend shares to overview is Timbercreek Monetary Corp. (TBCRF).

Enterprise Overview

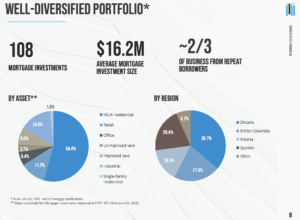

Timbercreek Monetary is a Canadian non-bank lender specializing in short-term, structured financing for business actual property. The corporate primarily gives first-mortgage loans for income-producing properties, together with multi-residential, retail, industrial, and workplace property. Its loans help acquisitions, redevelopment, or transitional financing and are usually repaid by means of long-term financing or property gross sales. The agency’s portfolio is totally targeted on business actual property, with round 92% of capital deployed in Ontario, British Columbia, Quebec, and Alberta.

Timbercreek emphasizes conservative danger administration, sustaining a 63.3% loan-to-value ratio (year-end 2024) and floating-rate loans with fee flooring to guard in opposition to market volatility whereas benefiting from rate of interest actions. The corporate pays month-to-month dividends, interesting to income-focused buyers, and has a market capitalization of CAD 460.8 million. Its disciplined lending mannequin and urban-focused portfolio present steady, high-quality publicity to Canada’s main actual property markets.

Supply: Investor Relations

Timbercreek Monetary reported Q2 2025 web earnings of $12.4 million, or $0.15 per share, barely under expectations. Web funding earnings was $25.2 million, and distributable earnings totaled $14.6 million ($0.18 per share). The corporate declared $14.3 million in dividends ($0.17 per share), yielding 9.5% on the present share value.

The web mortgage portfolio grew to $1.114 billion, up 11% year-over-year, with new loans weighted towards the tip of the quarter. Stage 2 and three loans totaling $80 million have been resolved, liberating capital for higher-yield investments. Variable-rate loans with rate of interest flooring made up 87.4% of the portfolio, defending in opposition to rate of interest swings, whereas multi-family residential property stay resilient.

The portfolio’s weighted-average LTV was 66%, with first mortgages accounting for 91.6% and cash-flowing properties accounting for 76.3%. Weighted common rates of interest have been 8.6%. Timbercreek’s disciplined underwriting, energetic mortgage administration, and deal with high-quality city property proceed to generate steady earnings and enticing risk-adjusted returns for shareholders.

Supply: Investor Relations

Progress Prospects

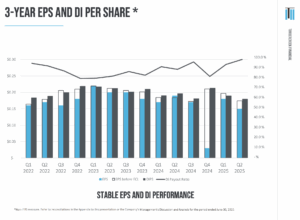

Timbercreek Monetary grows by lending to new prospects at enticing charges, primarily in opposition to income-producing properties. Nonetheless, EPS has proven little development over the previous seven years, and U.S. buyers face added danger from CAD/USD fluctuations. Even accounting for foreign money results, Timbercreek’s backside line has been largely flat, and EPS is predicted to stay steady over the subsequent 5 years.

Over the previous decade, EPS ranged from $0.36–$0.43 by means of 2017, fell to $0.23 in 2020 resulting from low charges and pandemic-related accounting changes, and rebounded to $0.43 by 2023. EPS declined to $0.28 in 2024 from higher-risk mortgage provisions and a few portfolio runoff.

Distributable earnings per share is predicted to remain round $0.36, and the month-to-month dividend has been steady at roughly $0.042 USD since 2017. Timbercreek stays a low-growth, income-focused funding with predictable dividends.

Supply: Investor Relations

Aggressive Benefits & Recession Efficiency

Timbercreek Monetary’s aggressive benefit lies in its deal with short-term, structured lending to business actual property buyers, permitting quicker execution and extra versatile phrases than conventional Canadian banks. Its disciplined underwriting, conservative loan-to-value ratios, and excessive share of first mortgages (over 90% of the portfolio) present draw back safety, whereas variable-rate loans with rate of interest flooring assist the corporate profit from rising charges and mitigate rate of interest danger. Moreover, Timbercreek’s urban-focused, income-producing property portfolio ensures predictable money movement and steady distributable earnings for shareholders.

Throughout financial downturns, Timbercreek has demonstrated relative resilience. Its emphasis on cash-flowing properties, primarily multi-family residential property, and conservative lending practices helps keep mortgage efficiency even in softer markets.

Whereas EPS will be unstable resulting from accounting changes or foreign money fluctuations, precise defaults have traditionally been restricted, and the corporate has continued to generate regular distributable earnings. This defensive positioning makes Timbercreek a extra steady selection in contrast with broader business actual property lenders throughout recessions.

Dividend Evaluation

Timbercreek Monetary’s annual dividend is $0.50 per share. At its latest share value, the inventory has a excessive yield of 9.5%.

Given the corporate’s 2025 earnings outlook, EPS is predicted to be $0.50 per share. Consequently, the corporate is predicted to pay out 100% of its EPS to shareholders in dividends.

Closing Ideas

Timbercreek Monetary gives publicity to high-yield, short-term business actual property lending, benefiting from rate of interest sensitivity and energetic portfolio administration. The corporate provides enticing month-to-month dividends, however buyers ought to train warning, as the present payout stage will not be totally sustainable.

Its returns are tied to market situations and the efficiency of income-producing properties, making it a higher-risk funding relative to extra diversified or low-volatility choices.

Given its present valuation and restricted potential for dividend development, we count on modest whole returns, forecasting roughly 4.3% annualized by means of 2030. Contemplating the mix of elevated danger, stagnant earnings, and capped dividend upside, the inventory is rated a promote, as its whole return potential seems restricted relative to various income-focused investments.

Excessive-Yield Particular person Safety Analysis

Different Positive Dividend Sources

Thanks for studying this text. Please ship any suggestions, corrections, or inquiries to [email protected].

2025-10-30")

{kind=link}