Klaus Vedfelt

Article Thesis

Alphabet (NASDAQ:GOOG)(NASDAQ:GOOGL) has not too way back seen its shares come beneath stress on account of licensed battles with regulators and on account of worries about what ChatGPT may indicate for Alphabet’s search enterprise in the end. Nevertheless I contemplate that these risks are overblown. On the similar time, Alphabet now trades at a extremely undemanding valuation whereas persevering with to ship extraordinarily attractive enterprise improvement. I contemplate that this presents a nice searching for different on this high-quality stock — it’s time to be greedy when others are fearful, as Warren Buffett has taught us.

Earlier Safety

I’ve lined Alphabet proper right here on Searching for Alpha a lot of situations, most not too way back in April. Close to half a 12 months has handed since then, with Alphabet reporting quarterly earnings outcomes for Q2 inside the meantime, whereas GOOG’s valuation has moreover come down. Closing nonetheless not least, regulatory factors have progressed, which is why it’s time for an enhance.

Why Being Greedy When Others Are Fearful Can Make Sense

The above phrase is utilized by Warren Buffett, one among many best-known and most worthwhile price patrons on the earth. Markets are prone to overreact often, every to the upside and to the draw again. Good news could find yourself in very substantial share worth options in some situations, nonetheless it might find yourself that these options have been overblown — assume, as an example, regarding the COVID vaccine options for Moderna (MRNA), BioNTech (BNTX), and Pfizer (PFE). All of them have seen their shares fall significantly, as their valuations have been too extreme as a result of the market was greedy. In the identical methodology, markets may be too fearful. Meta Platforms (META) seen its shares crash not too means again when the market feared that the company was overspending on its metaverse investments. Nevertheless the agency corrected its course, and earnings rapidly soared as soon as extra. Individuals who used the panic to buy shares on a finances when the possibility arose have seen their investments develop by plenty of of proportion components in a short time interval. When markets are irrationally bearish on a top quality stock, that will make for an superior searching for different. I contemplate that this holds true for Alphabet presently.

What The Market Fears

Over the past two months or so, Alphabet has seen its shares pull once more from a 52-week extreme of $193 to the $140s, making for a extremely substantial pullback. This was not pushed by weak outcomes — pretty the other, as Alphabet beat estimates merely when it reported its Q2 outcomes just a few weeks previously. The share worth pullback moreover wasn’t pushed by unfavourable analyst revisions. As Searching for Alpha explains, practically all of revisions for every Alphabet’s prime line and its bottom line have been upwards over the past three months, with better than 30 upwards revisions for every traces in that timeframe.

Alphabet’s weak share worth effectivity inside the newest earlier was thus neither pushed by weak ends within the present nor by expectations for weaker ends within the near time interval. In its place, it seems to be like like patrons have some pretty imprecise worries about rivals from Artificial Intelligence-driven search, whereas political and regulatory worries exist as properly. Let’s take a extra in-depth look:

ChatGPT has made an infinite splash spherical two years previously. The Large Language Model has a weekly full of life shopper base of spherical 200 million, which is profitable for OpenAI for sure. They don’t seem to utilize the service pretty usually, nonetheless, as month-to-month internet hits full spherical 2.4 billion, which pencils out to spherical 80 million per day. Google, within the meantime, is used for 22 billion searches per day. After we consider to internet hits that ChatGPT will get per day with the searches carried out by means of Google, the latter amount is spherical 275x greater. Whereas ChatGPT is profitable for OpenAI, it’s nonetheless abysmally small as compared with Google Search. And Google Search is just one of Alphabet’s many enterprise fashions, with YouTube, cloud computing, and so forth providing additional earnings.

All through the most recent quarter, Alphabet’s earnings was up 15% in mounted currencies, with improvement accelerating from the sooner 12 months when the growth worth had been 9%. Google Search earnings was up 14% 12 months over 12 months all through the most recent quarter, displaying an in-line improvement worth as compared with the rest of the company (company-wide reported earnings was up 14%, there was a small foreign exchange headwind). Whatever the curiosity that some have in ChatGPT, it doesn’t seem like ChatGPT is hurting Alphabet’s Search enterprise the least bit — Search is many situations better, and continues to develop. With improvement even accelerating, there could also be, I contemplate, little objective to worry that Google Search will run into principal points. In a rising market, every ChatGPT and Google Search can develop, with the latter rising from a method better base.

Moreover, it’s important to note that Alphabet has its private Large Language Model. Even when LLMs have been to realize massive market share, Alphabet would in all probability not be missed, as Alphabet’s Gemini would in all probability be among the many many beneficial LLMs should such a state of affairs occur.

Some patrons are moreover anxious about regulatory factors. Alphabet is being attacked by the DoJ over its Google selling enterprise, with the DoJ claiming that Google is illegally working a monopoly. There have been many antitrust situations in opposition to Massive Tech firms so far, along with Microsoft (MSFT), Meta Platforms, and Apple (AAPL), nonetheless these situations under no circumstances hurt these firms meaningfully in the long run. These firms didn’t get minimize up up, nor did earnings fall — pretty the other: Microsoft, Apple, and Meta Platforms are additional worthwhile and further worthwhile than they’ve ever been:

At least so far, antitrust situations have been thus additional of a nuisance than an precise threat for Massive Tech firms. I contemplate that there’s a superb probability that the similar will preserve true for the current antitrust case in opposition to Google. And even when the trial is worthwhile and the DoJ wins, I assume that there may be some minor concessions. Alphabet moreover might presumably be pressured to pay fines, nonetheless even a multi-billion buck improbable wouldn’t be an issue the least bit — Alphabet sits on $101 billion of cash. Would a improbable of $1 billion, $5 billion, and even $10 billion be a unfavourable enchancment? Positive, that may be true. However it could not be a threat for the company — Alphabet’s patrons would in all probability not even uncover, in any case, there isn’t any such factor as a big distinction between a $101 billion cash place and a $91 billion cash place. Alphabet’s working cash flow into totaled $105 billion over the past 12 months, thus even a hypothetical improbable of $10 billion may be equal to only some weeks worth of cash flows.

Alphabet: A Good Deal

Alphabet combines many positives: An exquisite market place inside the cash cow Search market, a strong place inside the fast-growing cloud computing home, a fortress steadiness sheet, sturdy enterprise improvement, and tight worth controls that make its margins develop better and higher.

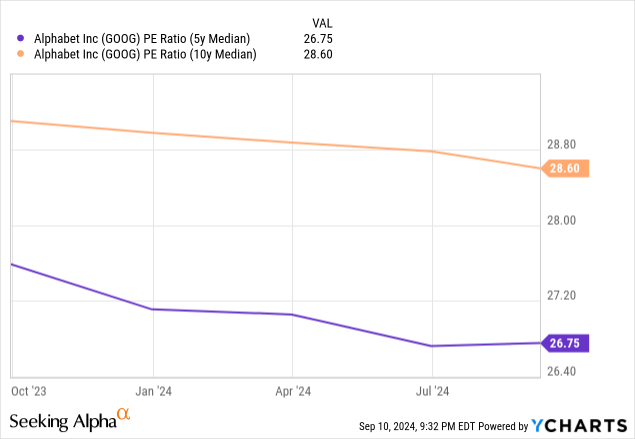

And however, Alphabet is a fairly low value stock, I contemplate. Based totally on current estimates for this 12 months, Alphabet trades for just below 20x forward web earnings. After we take into consideration that the company has a clear historic previous of beating estimates with six earnings per share beats in a row, it couldn’t be too surprising if the consensus earnings per share estimate for 2024 is simply too low, which could finish in a superb lower valuation. After we take into consideration Alphabet’s sizeable web cash place, the cash-adjusted earnings a lot of is lower as properly. Nevertheless even with out these modifications, Alphabet trades at a sizeable low value as compared with the market and its private historic valuation norm. The S&P 500 trades at spherical 26x 2024’s anticipated earnings correct now, which suggests Alphabet trades at a discount of spherical 20%. On the subject of mannequin energy, enterprise improvement, margins and returns on capital, and so forth, Alphabet appears as if an above-average top quality agency for sure. The reality that it nonetheless trades at an infinite low value to the broad market is thus surprising.

Throughout the above chart, we see that Alphabet was largely shopping for and promoting with a mid to high-20s earnings a lot of so far. The current sub-20 earnings a lot of is thus historically low.

Normal, I contemplate that Alphabet’s very undemanding valuation, along with its diverse strengths and compelling improvement outlook, makes shares look attractive.

Risks To Have in mind

No funding is risk-free, and that moreover holds true for Alphabet. It’s attainable that this antitrust case is completely totally different as compared with totally different Massive Tech antitrust situations and that there’ll in all probability be a critical affect, although I don’t see this as very in all probability. Even when the company have been to be minimize up up, the sum of the parts would nonetheless be extraordinarily worthwhile, actually.

All through a attainable recession, selling budgets may get decrease, which could have a unfavourable affect on Alphabet’s selling enterprise. Alphabet is thus not completely resilient versus macro troubles, although its massive cash pile would provide quite a few security in any downturn, I contemplate.

Alphabet is spending huge sums of money on its AI ventures, which contains the acquisition of NVIDIA’s (NVDA) AI data center chips. It’s attainable that the return on this funding will ultimately be unattractive. In that case, Alphabet would have burned a significant sum of money, although this might not be a company-threatening draw back the least bit.

These risks shouldn’t be ignored, and it’s smart for patrons to control them. That being talked about, I contemplate that the potential rewards outweigh the risks — when a high-quality improvement agency is on sale and trades at an infinite low value to its historic valuation norm and to the broad market, it’s smart to be greedy.

Q3 2024 Earnings Call Transcript")

")

{kind=link}