Solskin

Introduction & Funding Thesis

I closing wrote about Doximity (NYSE:DOCS) in April, the place I rated the stock a “preserve.” Although I mentioned that the stock has a attainable upside of not lower than 29% from its ranges once more then, I believed that patrons could possibly be weary until the administration would possibly reignite the growth story. Since then, the stock has climbed 45% as a result of it reported a strong Q1 FY25 earnings report, the place earnings and Adjusted EBITDA grew 17% and 41% YoY, respectively, beating estimates.

Concurrently, the administration moreover raised their earnings and earnings steering on your whole FY25. All through the quarter, the company observed a 16% enhance in purchaser rely, contributing $500K+ in Subscription Revenue and the administration sounded considerably bullish on the tempo of their product innovation, which ought to help them seize larger market share.

Whereas the administration maintained its cautious tone on the final state of the financial system, the place it continues to see year-over-year declines in Web Retention Value, I wish to stage out that the metric has stabilized on a sequential basis. Whereas a projection of a 9% YoY growth charge in earnings isn’t technically a “growth” stage, it may have marked a bottom. Subsequently, assessing every the “good” and the “harmful”, I take into account that patrons can provoke a small place inside the agency, making it a “buy”.

The great: Revenue growth pushed by 16% enhance in $500K+ prospects, Resonating Product Innovation, Growing margins

Doximity reported its Q1 FY25 earnings, the place earnings grew 17% YoY to $126.7M beating estimates, which was pushed by a 16% enhance in purchaser rely, contributing not lower than $500K in subscription earnings on a trailing twelve-month basis. Within the meantime, their prime 20 customers, which embody refined pharmaceutical producers, moreover grew on the quickest charge, up 21% on a trailing twelve-month basis. That’s indicating that the combination of their product innovation and “land and develop” approach is starting to bear fruit, as distinctive energetic prospects on the platform grew by double digits, thus deepening adoption of their choices.

Q1 FY25 Earnings Slides: Revenue and Earnings growth

With regards to their product innovation, Doximity observed a file 590,000 distinctive energetic prescribers leverage their genAI telehealth, messaging, and scheduling devices to boost affected particular person experience and provide larger care, whereas utilization of their AI-powered personalized info feed moreover set new info. Within the meantime, the Doximity GPT utility has moreover seen a deep adoption by medical medical doctors, with over 1.5M letter requests or prompts, as medical medical doctors look to streamline their administrative duties. All through the earnings title, the administration shared the following excerpt that demonstrates how Doximity GPT is enabling medical medical doctors to be additional atmosphere pleasant.

“The American Medical Affiliation estimates that medical medical doctors spend 12 hours each week on prior authorization paperwork. So chopping that time in half is a substantial enchancment. Dr. Tariq went on to say that Doximity GPT is “lastly a tool I can use to battle once more.”

Lastly, Doximity has rolled out its new shopper portal to 30% of their customers, which consists of three key choices that embrace day-to-day updates, product sales data, and actionable recommendations, enabling their prospects to have full transparency and actionability of their best-performing content material materials and efficiently measure ROI. So far, the consumers have been strongly resonating with the portal, as they’ll confidently take into account their packages and allocate spending accordingly to maximise ROI.

Shifting gears to profitability, Doximity generated an Adjusted EBITDA of $65.9M, which grew 41% YoY, with a margin of 52%, which is 900 basis components elevated than the sooner yr. The margin expanded as non-GAAP working payments contracted over 2% YoY, indicating a extreme diploma of operational effectivity. Within the meantime, the company’s success in driving elevated spend per purchaser, significantly by rising their $500K+ purchaser cohort, moreover carried out a pivotal place in unlocking working leverage.

The damaging: Administration nonetheless cautious regarding the macroeconomic panorama, Web Retention Value declined on a year-over-year basis.

However, the administration continued to maintain up its cautious stance on the final macroeconomic state of affairs, which has been negatively impacting pharma budgets. All through the earnings title, Anna Bryson, CFO at Doximity, outlined that they rely on pharma budgets to develop roughly 5-7%, which has not modified from its earlier expectation. However, what I found optimistic is that the administration sounded pretty bullish on the ability of their current product portfolio and the additional insights that are being pushed by their shopper portal, which ought to help it unlock a greater pharma funds over time as they get additional comfortable deploying their {{dollars}} with Doximity earlier on inside the upsell cycle. On the an identical time, Doximity may be taking a measured technique to R&D spend, which declined 4.2%, demonstrating that the administration is trying to navigate a fancy macroeconomic state of affairs, develop platform engagement, and preserve their aggressive positioning all on the an identical time. On that discover, Doximity is projected to develop at a loads faster charge of 9% in FY25 when compared with its fast opponents, which embrace Teladoc (NYSE:TDOC), which is anticipated to see product sales decline by 2%, and American Correctly Firm (NYSE:AMWL), which is anticipated to develop by merely 1.6% along with far superior profitability.

Although Doximity is rising faster and additional worthwhile than its fast opponents, there isn’t a doubt that earnings growth is slowing. One in all many better areas of concern is that Web Retention Value is fixed to slide on a year-over-year basis from 118% to 114%, which can very nicely be pushed by tight pharma budgets, thus putting pressure on Doximity’s prime line. Up until this quarter, Doximity would report the number of prospects in its $100,000 cohort. In my earlier submit, I recognized that it was seeing a slight decline inside the number of prospects in its $100K+ cohort, and in This fall, it solely observed a 1% YoY enhance in its $100K+ cohort. Inside the latest quarter, the administration has not equipped the latest $100K+ purchaser cohort amount and as a substitute chosen to supply the consumer rely in its $500K+ cohort (which has been rising). So, whereas Doximity is having success in driving adoption of its choices inside the $500K+ cohort, which has a NRR of 121%, it’s attainable that it’s seeing larger churn from the cohort that sits between $100K and $500K in subscription earnings, thus pushing the amount down on a year-over-year basis. However, sooner than I shut this half, I wish to stage out that whole NRR figures have stabilized on a quarter-over-quarter basis, and matched with administration’s bullish sentiment on capturing a better share of the pharma funds from their superior product innovation, it could possibly be on the cusp of a turnaround.

Revisiting my valuation: A small place could also be initiated.

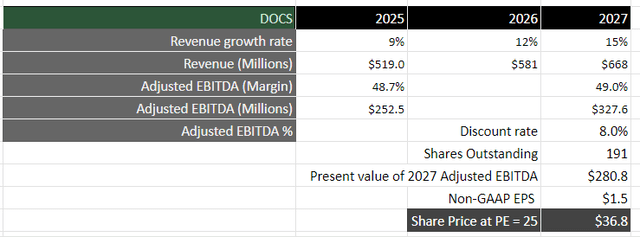

Wanting forward, Doximity administration has raised its earnings steering from $512M to $519M, which could symbolize a growth charge of 9% YoY. Assuming that Doximity can pace up its growth once more up into the low to mid youngsters over the next 2 years as a result of it drives product innovation to land and develop all through its purchaser base, resulting in elevated spend per purchaser, it must generate close to $668M in earnings by FY27.

From a profitability standpoint, the administration moreover raised its steering for Adjusted EBITDA from $244M to $252.5M, which may symbolize a margin of 48.7%. Assuming it should in all probability proceed to drive the current diploma of financial self-discipline over the next two years, it must generate close to $327M in Adjusted EBITDA, which may be equal to $280M, when discounted at 8%.

Taking the S&P 500 as a proxy, the place its companies develop their earnings on frequent by 8% over a 10-year interval, with a price-to-earnings ratio of 15–18, I take into account it must commerce not lower than at 1.5 situations the numerous, given the growth charge of its earnings all through this time interval. This may result in a PE ratio of 25, or a price objective of $36.8, which is the place the company is in the intervening time shopping for and promoting.

Author’s Valuation Model

My final verdict and conclusions

As soon as I revealed my earlier submit, I had a price objective of $29.4 for the stock, which represented an upside of shut to twenty-eight% from its ranges once more then. Since that time, the stock is up 45%. The reason I gave it a “preserve” was on account of I believed that the administration wanted to showcase that it’d revive its growth story. Whereas a 9% YoY growth charge in earnings isn’t primarily a “growth” story, it’s demonstrating indicators of a turnaround. First, it beat its earnings estimate by over 5%. Second, it’s seeing growth in its $500K+ subscription earnings cohort, with purchaser rely rising 16% YoY. Third, it’s seeing rising utilization and adoption of its choices, with the administration sounding bullish that it’ll in all probability unlock elevated pharma budgets ultimately. Fourth, it’s seeing a decline in NRR on a year-over-year basis, nonetheless it could possibly be stabilizing on a sequential basis, which can very nicely be proof of a turnaround. Lastly, the administration continues to remain exceptionally disciplined in relation to sustaining its operational effectivity.

Q3 2025 Earnings Call Transcript")

")

")

")

")

{kind=link}