Up to date on July seventh, 2025 by Felix Martinez

We consider that long-term buyers ought to give attention to the highest-quality dividend-growth shares. These are firms with lengthy histories of elevating their dividends, and sturdy aggressive benefits to gas continued dividend progress.

Due to this fact, we are likely to steer buyers towards the Dividend Kings, a bunch of simply 55 shares which have maintained no less than 50 years of consecutive dividend will increase.

You may as well obtain an Excel spreadsheet with the complete record of all 55 Dividend Kings (plus essential metrics equivalent to price-to-earnings ratios and dividend yields) by clicking on the hyperlink under:

We overview every of the Dividend Kings yearly. The next inventory to be reviewed on this yr’s version is AbbVie (ABBV).

There are questions relating to AbbVie’s future progress, as its flagship drug, Humira, is dealing with patent expiration. Nonetheless, the corporate has a plan to proceed rising within the years forward.

Enterprise Overview

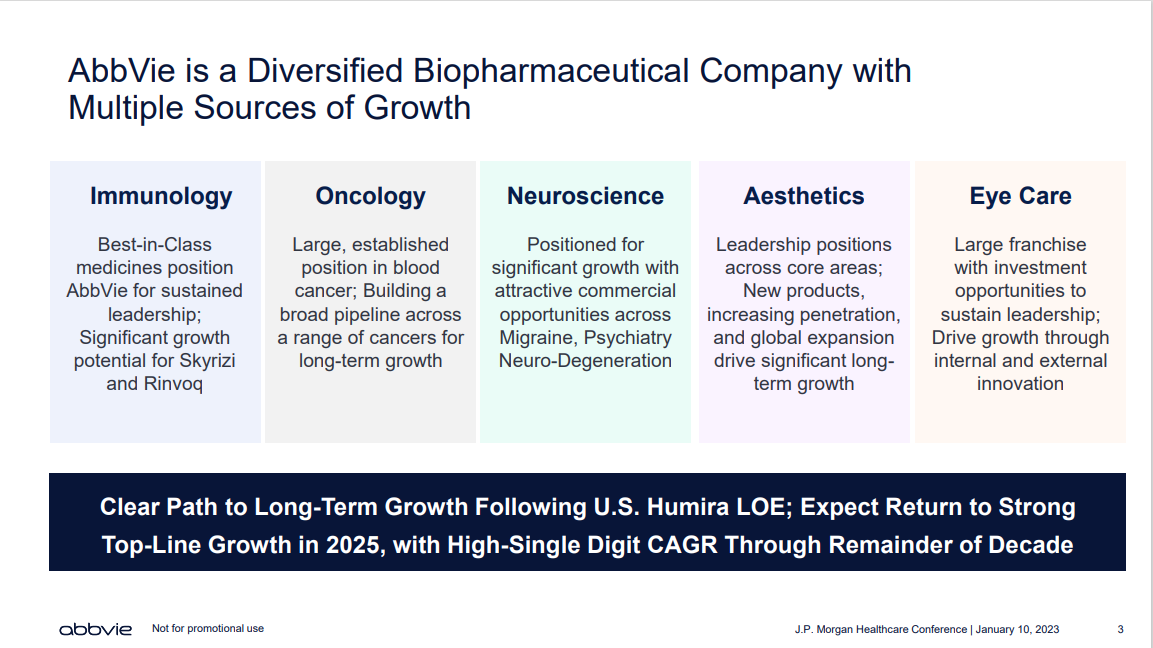

AbbVie is a worldwide pharmaceutical large. It started buying and selling as an unbiased firm in 2013, having been spun off from Abbott Laboratories (ABT). For the reason that spin-off, AbbVie has generated robust progress. In line with AbbVie, income and adjusted EPS progress elevated by 9% and 12.1%, respectively, annually from 2013 to 2024.

Right this moment, AbbVie focuses on a single primary enterprise section: prescription drugs. It focuses on a number of key therapy areas, together with immunology, hematologic oncology, neuroscience, and others.

Supply: Investor Presentation

For the reason that spin-off from Abbott, AbbVie has skilled glorious progress, primarily pushed by Humira, a multi-purpose drug. The problem for AbbVie is that Humira is now dealing with biosimilar competitors after it has misplaced patent exclusivity.

Even so, AbbVie stays a large within the healthcare sector, with an in depth and diversified product portfolio.

AbbVie reported Q1 2025 web revenues of $13.343 billion, up 8.4% (9.8% operational) from $12.310 billion in Q1 2024. Internet revenue fell 6.5% to $1.271 billion, with GAAP diluted EPS of $0.72, down 6.5%. Adjusted diluted EPS rose 6.5% to $2.46, regardless of a $0.13 per share impression from acquired IPR&D and milestones. The adjusted working margin was 42.3%, with gross margin at 84.1%, SG&A at 24.6%, and R&D at 15.4% of revenues. Key portfolio efficiency included immunology at $6.264 billion (up 16.6%), neuroscience at $2.282 billion (up 16.1%), oncology at $1.633 billion (up 5.8%), and aesthetics at $1.102 billion (down 11.7%).

Section highlights confirmed robust progress in immunology, with Skyrizi growing 70.5% to $3.425 billion and Rinvoq rising 57.2% to $1.718 billion, though Humira declined 50.6% to $1.121 billion. Neuroscience noticed Vraylar up 10.3% to $765 million, Botox Therapeutic up 15.8% to $866 million, and Ubrelvy/Qulipta up 17.8%/47.6% to $433 million. Oncology had Venclexta up 8.3% to $665 million and Elahere at $179 million, however Imbruvica dropped 11.9% to $738 million. Aesthetics weakened, with Botox Beauty down 12.3% to $556 million and Juvederm down 22.2% to $231 million.

AbbVie raised its 2025 adjusted diluted EPS steering to $12.09–$12.29 from $11.99–$12.19, reflecting sturdy Q1 outcomes. Strategic strikes included Rinvoq’s EU approval for large cell arteritis, Elahere’s constructive Part 3 knowledge, a BLA for trenibotulinumtoxinE, and collaborations with Xilio and Gubra for novel therapies. CEO Robert Michael highlighted the corporate’s robust fundamentals and pipeline developments, positioning AbbVie for sustained progress regardless of uncertainties surrounding commerce coverage.

Progress Prospects

The numerous danger for world pharmaceutical producers is the lack of patent safety. When a selected drug loses patent, the market is usually flooded with competitors, particularly for the world’s top-selling merchandise.

AbbVie’s greatest danger is the upcoming competitors to its flagship drug, Humira. This multi-purpose drug is used to deal with a wide range of situations, together with rheumatoid arthritis, plaque psoriasis, Crohn’s illness, ulcerative colitis, and extra.

Humira as soon as generated over half of AbbVie’s annual gross sales. Lack of patent exclusivity is a big overhang; because of this, AbbVie’s complete gross sales declined in 2023. On the similar time, AbbVie additionally expects to return to gross sales progress in 2025, with excessive single-digit annual progress by means of the tip of the last decade.

Luckily, the corporate ready for the lack of patent exclusivity on Humira by investing closely in new merchandise and acquisitions to spice up its progress. For instance, Rinvoq and Skyrizi are two key merchandise that signify long-term progress catalysts.

Supply: Investor Presentation

AbbVie additionally accomplished the $63 billion acquisition of Allergan. Allergan’s flagship product is Botox, which diversifies AbbVie’s portfolio by exposing it to the worldwide aesthetics market.

We anticipate AbbVie to attain 5% EPS progress over the subsequent 5 years. We consider the expansion outlook will enhance as soon as the Humira overhang is resolved, however there may be uncertainty surrounding AbbVie’s potential to offset this with new merchandise.

Aggressive Benefits & Recession Efficiency

Probably the most crucial aggressive benefit for AbbVie and any pharmaceutical firm is its patent portfolio. Pharmaceutical giants should make investments closely in growing new medication and therapies when one in all their blockbusters loses patent safety.

AbbVie has over 60 scientific applications. It has a number of progress alternatives to exchange Humira, notably within the therapeutic areas of immunology, hematology, and neuroscience. The results of its important funding in R&D is a well-stocked pipeline.

AbbVie was not a standalone firm over the last monetary disaster, so it doesn’t have a recession monitor report. Nonetheless, since sick individuals require therapy whatever the financial system’s power, it’s extremely probably that AbbVie would proceed to carry out effectively throughout a recession.

AbbVie’s earnings are more likely to decline considerably throughout a recession, however the dividend is predicted to stay safe. AbbVie has a projected dividend payout ratio of ~54% for 2025.

Valuation & Anticipated Returns

AbbVie is predicted to generate adjusted EPS of $12.19 for 2025 on the midpoint of steering. At this EPS degree, the inventory at present has a price-to-earnings ratio of 15.4.

Our honest worth estimate for AbbVie is a price-to-earnings ratio of 13, indicating that the inventory is at present overvalued. A declining P/E a number of might scale back shareholder returns by roughly 3.2% per yr over the subsequent 5 years.

Moreover, we anticipate annual earnings progress of 5% by means of 2029.

Lastly, the inventory has a present dividend yield of three.5%. Given these inputs, we anticipate annual returns of 5.2% per yr over the subsequent 5 years, making AbbVie inventory a maintain.

Ultimate Ideas

AbbVie is a high-quality enterprise, boasting a powerful pharmaceutical pipeline and important progress potential. It’s also a shareholder-friendly firm that returns extra money move to buyers by means of inventory buybacks and dividends.

AbbVie faces a big problem in changing misplaced Humira gross sales, because it competes with different firms within the U.S. and Europe. That is why we’ve got pretty low assumptions for the corporate’s future EPS progress and honest worth P/E a number of.

Nonetheless, the corporate has constructed an in depth portfolio of latest merchandise that ought to assist preserve its progress. AbbVie can even be capable of generate extra progress from the acquisition of Allergan.

Nonetheless, the anticipated returns make the inventory a maintain.

Further Studying

The next databases of shares include shares with very lengthy dividend or company histories, ripe for choice for dividend progress buyers.

Thanks for studying this text. Please ship any suggestions, corrections, or inquiries to [email protected].

")

{kind=link}