by Charles Hugh-Smith

All these curveballs will additional fragment the housing market.

Oh for the nice outdated days of a pleasant, clear housing bubble and bust as in 2004-2011: subprime lending expanded the pool of patrons, liar loans and free credit score created speculative leverage, the Federal Reserve supplied extreme liquidity and the watchdogs of the business have been both induced (ahem) to look away or dozed off in a haze of gross incompetence.

The bubble burst was additionally simple: unsustainable debt, leverage, fraud and hypothesis all unwound in 2009-2011. The trigger was apparent and the impact simply predictable.

Alas, in the present day’s housing bubble and bust has these curveballs:

1. A silly amount of money sloshing around the globe.

2. Who has the money and an curiosity in utilizing it to purchase homes.

I thought-about the 2 standard explanations for the present bubble in Is Housing a Bubble That’s About to Crash?: 1) a housing scarcity and a couple of) the Federal Reserve shopping for mortgage-backed securities and flooding the financial system with low-cost credit score, inflicting mortgage charges to plummet to file lows.

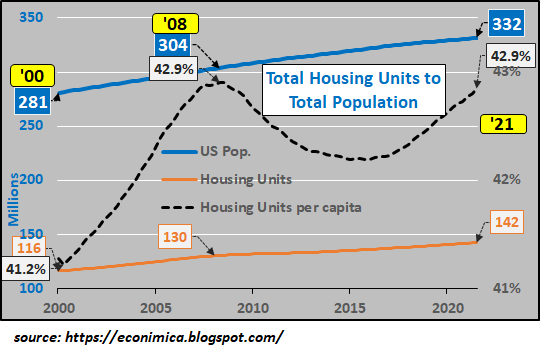

Because the per-capita housing chart under reveals, the variety of housing models per particular person (per capita) is now on the identical stage because the earlier bubble. This doesn’t help the housing-shortage clarification on a nationwide scale (although native scarcities might be driving costs a lot larger), and factors to a speculative cheap-credit-fueled FOMO frenzy as the first supply of the bubble.

Now that mortgage charges have risen from 3% to five%, the speculative credit-FOMO bubble is popping.

Not like the nationwide bubble bust in 2009 – 2011, the present bust might be extremely fragmented as a result of enormous variety of rich individuals with silly quantities of money at their disposal, due to the Every little thing Bubble that made the already-wealthy a lot, a lot wealthier.

The housing bubble will burst in locations the place patrons should borrow to purchase, not the place rich money patrons need to dwell. These with money don’t care a lot about mortgage charges, nor are they terribly delicate to cost. What issues is that they get to dwell the place they need to dwell.

One cause why individuals with money might be desirous about utilizing it to purchase a home is the city migration is reversing. The wealthy individuals who snapped up tony houses in tony city neighborhoods are quietly promoting to the unwary and transferring to rural cities and unique enclaves removed from decaying city facilities.

The locations the rich need to dwell don’t need sprawl and new houses sprouting up, so provide might be restricted. Locals who preceded the rich even have a dim view of sprawl, congestion, overcrowded colleges, and all the opposite blights of constructing booms.

Sturdy demand from money patrons and restricted provide equal house costs which don’t drop, they solely notch larger. Word that 1) mortgage charges don’t matter to these with silly quantities of money and a couple of) these are usually not the typical speculative purchaser, they’re shopping for for themselves, and are protecting of every part that makes the place someplace they need to dwell: they’re Tremendous-NIMBYs (not in my again yard). “Progress” is ok so long as it’s elsewhere.

A lot of individuals with insane quantities of money are usually not U.S. residents, they usually’re searching for secure havens and good neighborhoods in locations like Canada, Australia and the U.S. Sensible populations (for instance, Switzerland) place restrictions on overseas possession for the plain cause that overseas money can shortly drive costs past the attain of the homegrown populace. Residents turn out to be landless serfs in their very own nation.

Absent such limits on overseas possession, housing costs in fascinating locales shortly rise past the attain of the non-rich and carry on going larger.

Many of those overseas rich are escaping capital controls and the potential clawback of ill-gotten good points, and so they’re extremely motivated patrons.

Company house owners and patrons are one other curveball. Companies which snapped up a whole lot or 1000’s of rental homes could have confused greed with investing genius, and a pleasant little recession could depart them with a whole lot of vacant houses or newly unemployed renters resisting eviction for non-payment of lease.

As these companies unload their huge stock, costs might fall significantly decrease than pundits anticipate.

Yet one more curveball is city decay. It’s been roughly 50 years since U.S. cities unraveled in a self-reinforcing spiral of decay, and so the standard view is fast decay of fundamental companies and the ensuing collapse of housing values is “inconceivable.” Earlier than making any rash conclusions about “impossibility,” analysis New York Metropolis circa 1971 – 1980.

What’s been forgotten is the city decay of the Seventies was reversed by two one-off miracle-saves: the exploitation of just lately found super-giant oil fields, which introduced vitality prices down within the Eighties and past, and a couple of) the hyper-financialization of the U.S. and world economies.

Discoveries of latest super-giant oil fields has petered out. The planet has been scoured and there aren’t any extra. As for financialization, boosting debt and leverage are actually negatives, not positives. There might be no miracle-save by increasing debt, leverage and hypothesis.

City decay–declining tax base and tax revenues, hovering prices and crime and the out-migration of the wealthiest taxpayers–is a curveball few perceive. It’s “inconceivable” till it’s unstoppable. Folks vote with their toes.

All these curveballs will additional fragment the housing market. If nationwide house costs fall 20%, locales blighted by company dumping of leases and concrete decay might fall 50% on their method to “inconceivable” declines. Locales favored by the rich with silly quantities of money might go up 50%.

Generational and regional inequalities have reached extremes that additional fragment the bubble bust. People who purchased houses for $150,000 many years in the past in bubblicious coastal areas are promoting out for $1 million in money, whereas those that paid roughly the identical value in a less-bubble-blessed area have $250,000 after promoting– $100,000 lower than the present median house value. If you purchased and the place you got makes all of the distinction.

This can drive additional fragmentation because the sorta-wealthy with $1 million in money scoop up the tier under the mega-wealthy. The $2.5 million home within the unique enclave is out of attain, however the one for $950,000 in a extremely fascinating locale remains to be do-able for the highest 5%. These having to borrow a mortgage and make funds out of wages should search for locales which have good fundamentals however aren’t fairly engaging sufficient to be over-run by these with silly quantities of money.

Paul of Silver Docs and I talk about these matters in depth in The Large Issues And Crash Dynamics Of The Spring/Summer season 2022 Housing Market Disaster, Simplified (1:08 hr).

Assist Assist Unbiased Media, Please Donate or Subscribe:

Trending:

Views:

35

")

{kind=link}