piranka

Cloudflare’s (NYSE:NET) stock has been fairly range bound over the past 11 months, as investors weigh near-term headwinds against the company’s long-term opportunity. Demand in many SaaS segments appears to have found a temporary floor in early 2023, particularly those related to security. Deterioration in the macro environment could cause demand to decline further though. Longer-term, Cloudflare continues to innovate rapidly and introduce products that are difficult for incumbents to compete against. This situation should become more apparent in time as Cloudflare continues to expand into adjacent markets.

Market

Cloudflare noted a downturn beginning in the fourth quarter of 2021, which it was able to identify early due to its exposure to internet traffic and ecommerce. Management responded to this situation by moderating investments and focusing on profitability. Growth was still fairly robust throughout 2022 though, indicating that the market did not weaken as much as initially expected.

Cloudflare’s management now believes that the market has rebounded somewhat, with their pipeline improving in the third quarter of 2022 and strengthening further in the fourth quarter. There is still uncertainty around the conversion of opportunities into ACV though. Customers are pursuing smaller deals and sales cycles are lengthening due to increased scrutiny.

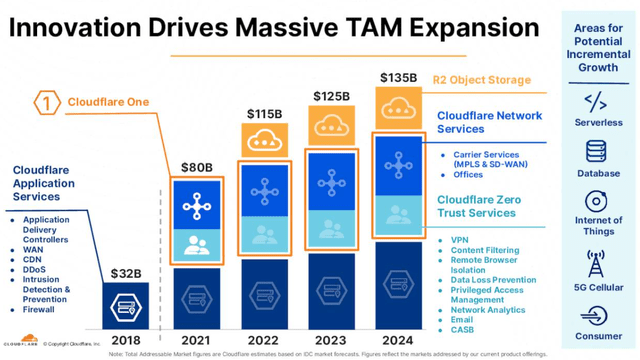

While the near term remains uncertain, Cloudflare is still well positioned to become a leading SaaS company. Innovation is driving TAM expansion, although Cloudflare must still demonstrate that it can capitalize on this opportunity.

Figure 1: Cloudflare TAM (source: Cloudflare)

Cloudflare

Innovation is driving Cloudflare upmarket, increasing exposure to larger customers and creating the need for a top down sales motion. Cloudflare broadly groups its products into three waves:

- Wave 1 products – Application Services

- Wave 2 products – Zero-Trust

- Wave 3 products – Workers, Storage

While Cloudflare’s wave 2 products are maturing, they are still gaining traction in the market, and sales and marketing efforts need to improve. Wave 3 products are nascent, and it will likely take time for these to become significant revenue contributors. The importance of the wave 3 products extends beyond their growth potential though. Many of Cloudflare’s products are being built on Workers, enabling rapid innovation at the network edge. While much of the focus on edge computing is around reducing latency, Cloudflare continues to highlight the importance of compliance use cases. For example, Workers is being used extensively in Europe because of GDPR.

Networking Services

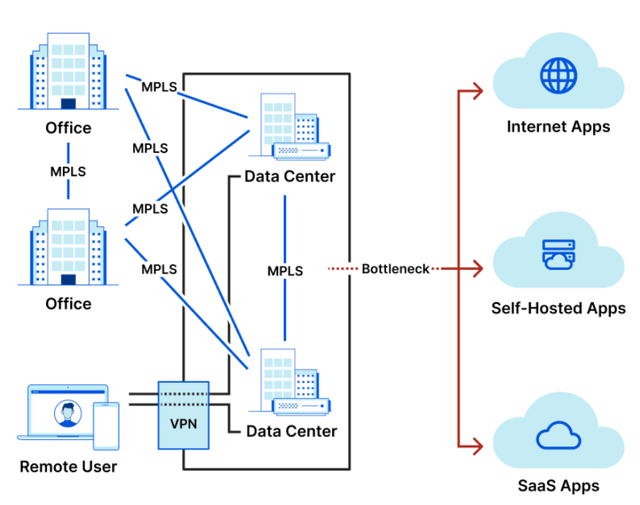

SASE is likely Cloudflare’s most important near-term opportunity. Cloudflare’s networking services, and competing solutions, are likely to replace MPLS over time, which in itself is a large market opportunity (45 billion USD). Magic WAN is a relatively low cost solution that enables vendor consolidation, provides a single control plane and drives efficiency.

MPLS offers an alternative to routers that rely on network addresses and complex routing tables. MPLS routes traffic over private wide area networks using the shortest path based on labels. This improves the speed of traffic, but has become inefficient and costly because:

- In a world with distributed infrastructure, it is becoming increasingly problematic to backhaul traffic to centralized data centers, rather than access the cloud directly.

- A proliferation of applications, services and mobile devices, has increased demand for bandwidth, and hence costs.

Figure 2: Illustrative Corporate Network (source: Cloudflare)

Software-Defined WAN (SD-WAN) can resolve some of these issues, but depending on how it is implemented, it can have its own issues. SD-WANs allow organizations to shift from MPLS private lines to broadband Internet, significantly reducing costs. SD-WANs can also offer application-aware intelligent routing based on path quality.

SD-WAN is generally implemented as a hardware-based edge routing technology that does not consider the network being traversed. Broadband internet is generally fast and widely available, but it doesn’t offer the end-to-end security or reliability that mission-critical applications require. This is where Cloudflare’s global network provides a point of differentiation and competitive advantage.

Magic WAN enables customers to utilize Cloudflare’s network to interconnect their infrastructure. Magic WAN eliminates the need to manage a mesh of tunnels. Cloudflare’s network acts as a hub so that a single Anycast IPSec or GRE tunnel provides connectivity to all other sites and applications. Zero Trust security can also be implemented as needed and managed through a single dashboard.

Zero Trust

Cloudflare has introduced a large number of services over the past few years, which may be a source of confusion. Many of these solutions have been bundled within Cloudflare One to drive go-to-market efficiencies and create a simpler value proposition. This bundling also broadly aligns with the services falling under SASE (WAN, SWG, CASB, ZTNA, and FWaaS). SASE is the convergence of wide area networking, and network security services like CASB, FWaaS and Zero Trust, into a single, cloud-delivered service model.

While Cloudflare has a solid zero trust solution, its competitive positioning in the space is still somewhat unclear. Zero trust requires a top down selling motion and a large amount of customer trust, both things that Cloudflare is still developing. One of the primary problems at the moment appears to be a lack of customer awareness of Cloudflare’s zero trust solution. Management has stated that they are happy with their win rates though. In particular, Cloudflare is successful amongst technically rigorous companies that measure performance and want to provide the best end user and developer experience.

Within zero trust, a large part of Cloudflare’s current business comes from replacing on-premise infrastructure from vendors like Cisco (CSCO) and Citrix. Amongst modern solution providers, Cloudflare has specifically mentioned Zscaler (ZS), Netskope and Palo Alto Networks (PANW). Zscaler operates multiple independent networks to provide their services, which can be inefficient and provide a poor customer experience. Cloudflare has mentioned customers switching from Zscaler for this specific reason.

Products like zero trust have little marginal cost for Cloudflare, which enables them to price competitively and achieve high margins. This could become important in time as Palo Alto and Zscaler both offer premium products that are extremely expensive to implement.

Sales and Marketing

Cloudflare’s sales organization is an area of the company that is still under development, and has potentially been a drag on growth. The shift up market means that Cloudflare is selling to larger customers, and increasingly, selling with a top down motion. Both of which are significant departures from Cloudflare’s previous product led growth amongst generally small customers. Marc Boroditsky recently joined Cloudflare to lead its sales organization and he has identified many areas that need improvement. Brent Remai also recently joined Cloudflare as the head of marketing. Remai was previously CMO at FireEye and CMO of Core Services at AWS.

It will likely take time for Cloudflare to develop a solid enterprise sales and marketing organization, and this creates a risk that the company will be left behind, even if its solutions are competitive. Cloudflare’s ability to attract and retain talent, and the quality of the management team, should limit this risk though.

Cloudflare must also make greater use of channel partners if it is to successfully compete in markets like Zero Trust. Channel partners only account for around 13% of Cloudflare’s revenue, compared to approximately 96% for Zscaler.

Another area where Cloudflare trails competitors is FedRAMP certification. Cloudflare only just received moderate FedRAMP certification. In comparison, companies like Zscaler and Palo Alto have been FedRAMP certified for some time, and Zscaler is the only security organization with the highest level of FedRAMP certification. The public sector space only accounts for around 3% of Cloudflare’s revenue, demonstrating both how far behind the company is, but also the opportunity ahead.

Disruptive Innovation

Cloudflare’s competitive positioning continues to be misunderstood as the company expands into new markets. Cloudflare is a disruptive innovator in the true sense of the term, rather than the grossly abused way that most new products are referred to as disruptive. Disruptive innovation is about the business model, not the technology. A disruptive business model leaves incumbents unwilling or unable to respond, allowing the new entrant to succeed.

Cloudflare started as essentially a low-priced CDN, an unattractive market that didn’t garner attention from future competitors in adjacent markets. Cloudflare used this market to build a highly efficient global network, which is now allowing it to expand into high-value markets with a differentiated value proposition.

Incumbents in these markets are faced with a difficult choice, as Cloudflare is beginning to gain market share. Building out a comparable network would be time consuming and expensive, and competitors are unlikely to achieve the traffic volumes that Cloudflare has. Competing on price is also often difficult, as Cloudflare generally has a lower cost basis, due to the amortization of network costs across a broad range of solutions. For example, Cloudflare could choose to offer its zero trust services for free to gain market share, as there is little direct cost associated with providing these services. While this is unlikely to happen, it highlights how differentiated Cloudflare’s position is to companies like Zscaler and Palo Alto.

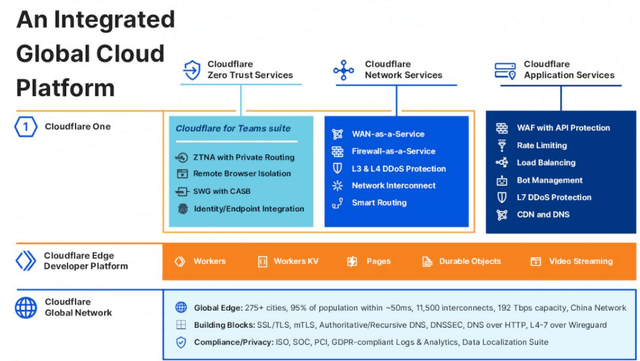

Figure 3: Cloudflare Solutions (source: Cloudflare)

This situation can most clearly be seen from Cloudflare’s launch of R2 storage, which is priced extremely favorably relative to Amazon’s (AMZN) S3 storage. While a direct comparison is difficult for a variety of reasons, Cloudflare offers free data egress and analysis suggests that storage pricing is roughly 35% lower. AWS achieves extraordinary margins on data egress, and part of this is likely due to its strong position in the cloud market, and desire to prevent customers from moving data elsewhere. If AWS chooses to respond, it will cannibilize an attractive source of profits and undermine the competitive positioning of its business.

Cloudflare is able to do this, due to the way that egress costs are actually calculated. The internet is made up of a collection of smaller networks. The networks that connect directly to each other are said to be “peered”. Intermediary networks that connect other networks are referred to as “transit providers”. Cloudflare purchases bandwidth from a range of transit providers at wholesale prices, based on the capacity used in a given month. This is important as costs are based on bandwidth, whereas vendors like AWS often charge based on data quantity, which is where the high margins come from.

Transit costs are also based on egress or ingress, whichever is higher, not both. As a caching proxy, egress typically exceeds ingress by 4-5x for Cloudflare, meaning Cloudflare pays for egress bandwidth. This is what allows Cloudflare to offer unmetered DDoS attack protection. An attack increases ingress, but this doesn’t impact Cloudflare’s costs, unless the attack is extremely large, allowing Cloudflare to offer unmetered DDoS protection.

Unlike transit, peering is typically free, meaning the more that Cloudflare peers, the less it has to pay for bandwidth. Peering also typically increases performance by cutting out intermediaries that may add latency. This is an important scale based advantage for Cloudflare that cannot be quickly or cheaply replicated.

While R2 may be a relatively niche storage solution compared to S3, it will be difficult for AWS to respond, and in time R2 storage should open up new opportunities. For example, R2 enables data replication across multiple regions using Snowflake tables. This is something that could be extremely expensive to do with S3 storage due to egress costs. Cloudflare’s management has suggested that R2 is gaining popularity amongst AI developers as it enables training data to be moved to the lowest cost GPUs available.

As Workers matures as a developer platform, it will also provide Cloudflare opportunities to enter markets like infrastructure management, developer tools and observability. The ongoing convergence of these segments with security is likely to give Cloudflare a strong competitive position, all based upon its network.

Financial Analysis

Cloudflare’s revenue growth has fallen off significantly in recent quarters, although management expects it to stabilize somewhat going forward. Growth deterioration is potentially problematic for Cloudflare’s stock as stable performance appears to have been one of the factors that has attracted investors over the past few years. The drop in growth isn’t particularly concerning for investors with a longer time horizon though, given macro headwinds and Cloudflare’s high exposure to smaller customers.

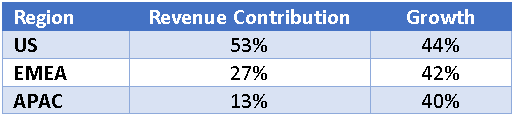

Table 1: Cloudflare Performance by Region (source: Created by author using data from Cloudflare)

Cloudflare has guided for 37% YoY revenue growth in the first quarter of 2023 and 37% revenue growth for the full year. The fact that management is not projecting a decline in growth throughout the year, has caused some to assume that guidance hasn’t been derisked to the extent of some SaaS peers. It should be noted that Cloudflare’s revenue is driven by subscriptions, providing a high degree of visibility, and management has a track record of beating guidance.

Management has stated that guidance does not include any expectation of an improvement in the macro environment or any benefits from go-to-market initiatives. A significant portion of Cloudflare’s revenue is also related to security, and many security vendors have stated that 2023 has started strongly.

Figure 4: Cloudflare Revenue Growth (source: Created by author using data from company reports)

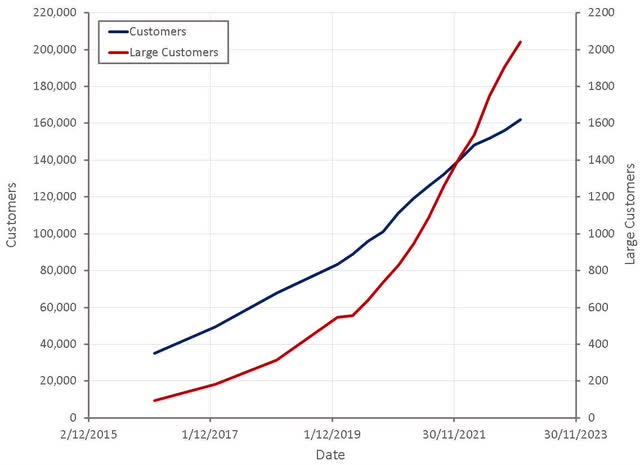

Cloudflare continues to attract new customers, and in particular, the company’s large customer count is growing quickly. This is reasonably impressive given Cloudflare’s exposure to smaller customers, which in general have been more impacted by the current environment.

Figure 5: Cloudflare Customers (source: Created by author using data from Cloudflare)

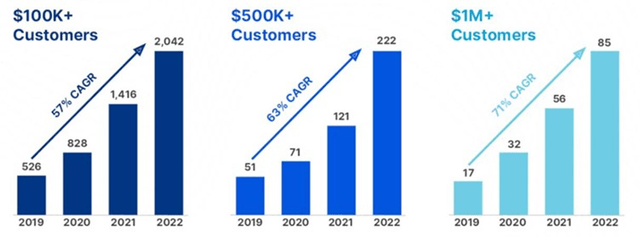

Larger customers are dominating Cloudflare’s growth, as indicated by the fact that revenue growth for sub 100K USD customers was only around 26% in 2022. This slowdown amongst smaller customers demonstrates the extent to which Cloudflare has been impacted by macro headwinds, but also how Cloudflare’s shift upmarket is progressing successfully.

Figure 6: Cloudflare Large Customer Growth (source: Cloudflare)

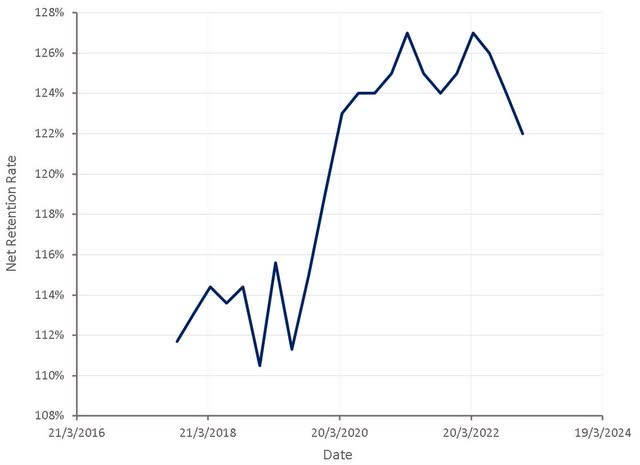

Cloudflare’s net retention rate has ticked lower in recent quarters, which is somewhat disappointing in light of Cloudflare’s growing portfolio of solutions. This decline has nothing to do with churn though, with management stating that gross renewal rates are over 90% and remain as high as ever. This figure is quite impressive given Cloudflare’s exposure to smaller customers, and should improve over time as Cloudflare’s presence amongst larger customers increases and customers adopt multiple solutions.

The drop in net retention rate is being driven by less net expansion within smaller customers. Retention of Cloudflare’s pay-as-you-go customer base improved in the fourth quarter though, rebounding to 2020-2021 levels.

Longer term, Cloudflare is still targeting a dollar-based net retention rate of over 130%, as seat-based products like zero trust and storage-based products like R2 scale.

Figure 7: Cloudflare Net Retention Rate (source: Created by author using data from Cloudflare)

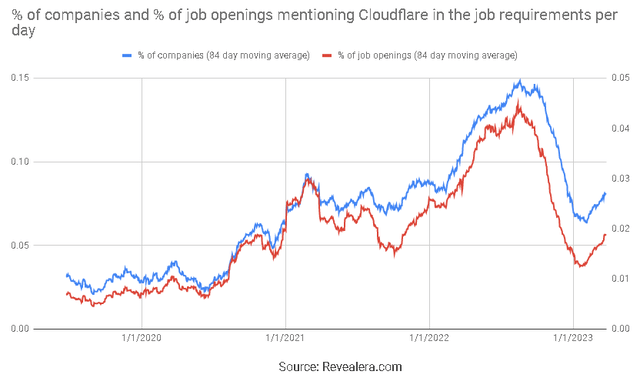

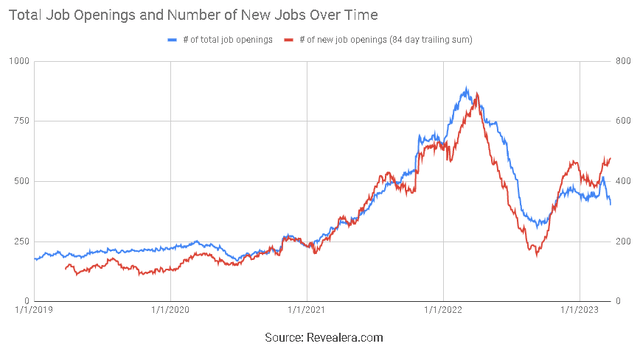

Job openings mentioning Cloudflare in the job requirements have ticked higher in 2023, which supports management’s assertion that 2023 has started well.

Figure 8: Job Openings Mentioning Cloudflare in the Job Requirements (source: Revealera.com)

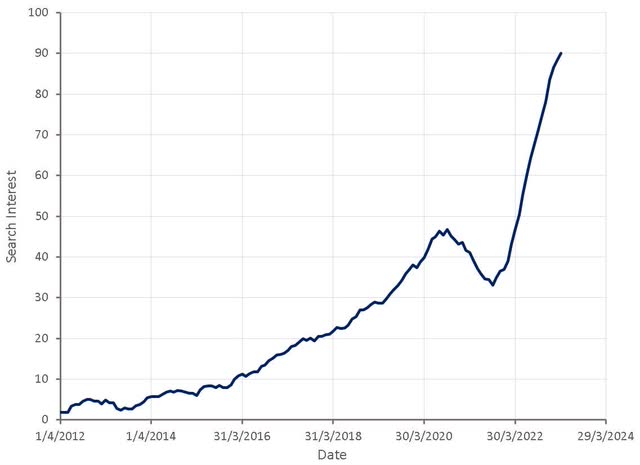

Search interest for “Cloudflare Pricing” also continues to be strong, although this could be the result of strong demand or concerns over pricing.

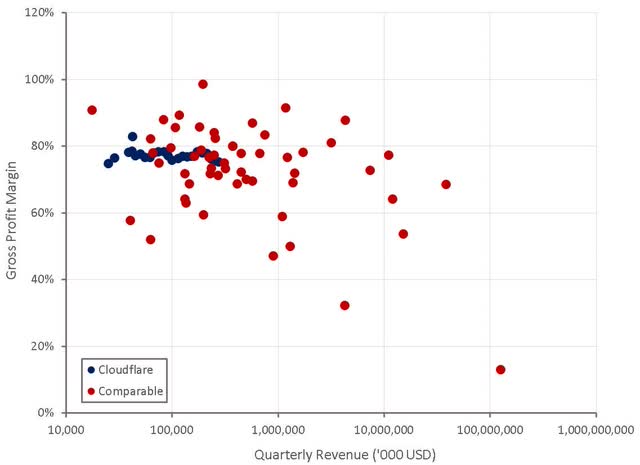

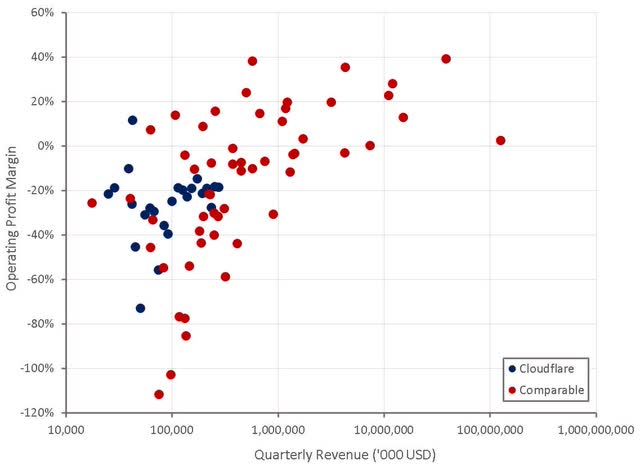

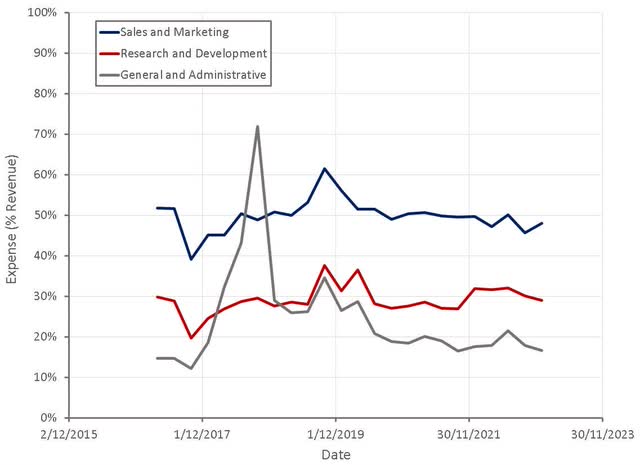

Figure 9: “Cloudflare Pricing” Search Interest (source: Created by author using data from Google Trends) Figure 10: Cloudflare Gross Profit Margins (Created by author using data from company reports) Figure 11: Cloudflare Operating Profit Margins (source: Created by author using data from company reports) Figure 12: Cloudflare Operating Expenses (source: Created by author using data from Cloudflare)

Job openings at Cloudflare increased in the second half of 2022, indicating that the market did not deteriorate to the extent that management initially expected. Over 400,000 people applied for roughly 1,300 positions at Cloudflare in 2022. This demand allows Cloudflare to hire talented individuals, while remaining disciplined in overall compensation.

Figure 13: Cloudflare Job Openings (source: Revealera.com)

Valuation

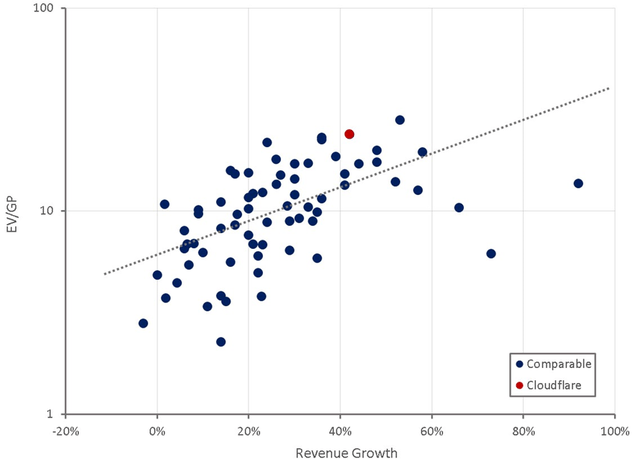

Cloudflare’s stock continues to be valued at a significant premium to the market given its growth and profitability. Absent a complete collapse in financial performance, this situation is likely to be ongoing though due to the strength of Cloudflare’s competitive position.

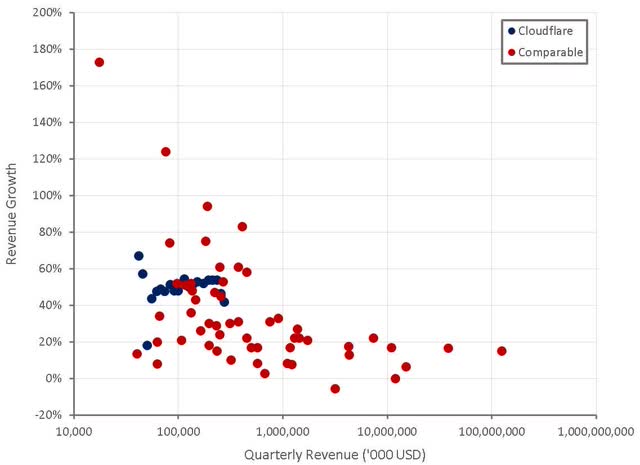

Figure 14: Cloudflare Relative Valuation (source: Created by author using data from Seeking Alpha)

Q4 2025 Earnings Call Transcript")

")

")

{kind=link}