Revealed July twenty sixth, 2022 by Nathan Parsh

With market uncertainty leading to important strikes up and down for a lot of the yr, traders may very well be seeking to spend money on safer and extra dependable investments as a substitute of tolerating a rollercoaster trip.

To that finish, we recommend that traders concentrate on proudly owning shares of blue chip shares. The time period “blue chip” can have a distinct which means to totally different traders. To us, we view blue chips as these corporations with at the very least 10 consecutive years of dividend will increase.

A longtime observe report of dividend progress of at the very least a decade implies that an organization has confirmed profitable at rising its distribution over a protracted interval and that administration groups are dedicated to rising the payout.

For corporations that measure dividend progress streaks within the a number of many years, they’ve proven that they’ll elevate their funds by way of all parts of the financial cycle. This consists of recessionary intervals, which are sometimes essentially the most tough setting to develop dividends.

In consequence, we really feel that blue chip shares are among the many most secure dividend shares that traders should purchase.

With all this in thoughts, we created a listing of 350+ blue-chip shares which you’ll be able to obtain by clicking under:

Along with the Excel spreadsheet above, we are going to individually assessment the highest 50 blue chip shares right now as ranked utilizing anticipated whole returns from the Positive Evaluation Analysis Database.

The subsequent installment of the 2022 Blue Chip Shares in Focus sequence will analyze Franklin Assets, Inc. (BEN)

Enterprise Overview

Franklin Assets was based in 1947 and is headquartered in San Mateo, CA. Franklin Assets is a worldwide asset supervisor that has a protracted and profitable historical past. The corporate presents funding administration providers, which contributes the vast majority of charges that Franklin Assets collects. As well as, the corporate gives gross sales, distribution, and shareholder providers. The corporate is valued at near $13 billion and generates annual income in extra of $8 billion.

Franklin Assets reported second quarter outcomes on Might third. Income grew 0.2% to $2.1 billion whereas adjusted earnings-per-share of $0.96 in contrast favorably to $0.79 within the prior yr.

Franklin Assets’ property underneath administration (AUM) is without doubt one of the largest in all the asset administration area.

Supply: Investor Presentation

As of the tip of the primary quarter of 2022, Franklin Assets had $1.5 trillion in AUM. The corporate’s AUM have enormously outperformed friends and benchmarks over a number of intervals of time.

AUM did decline $100.6 billion in comparison with the final quarter, principally as a result of $81.8 billion of internet market change, distributions, and different objects. The corporate additionally had $11.7 billion of long-term internet outflows and $7.1 billion of money administration internet outflows.

Development Prospects

Franklin Assets has a number of avenues for progress. First, the emergence of alternate traded funds has turn into a significant supply of energy within the asset administration enterprise. That is true for Franklin Assets as nicely. For instance, the corporate had $12.7 billion of outflows over the last quarter, however the ETF enterprise had $13 billion of internet flows as this funding technique stays highly regarded with traders even because the markets have seen violent swings in costs.

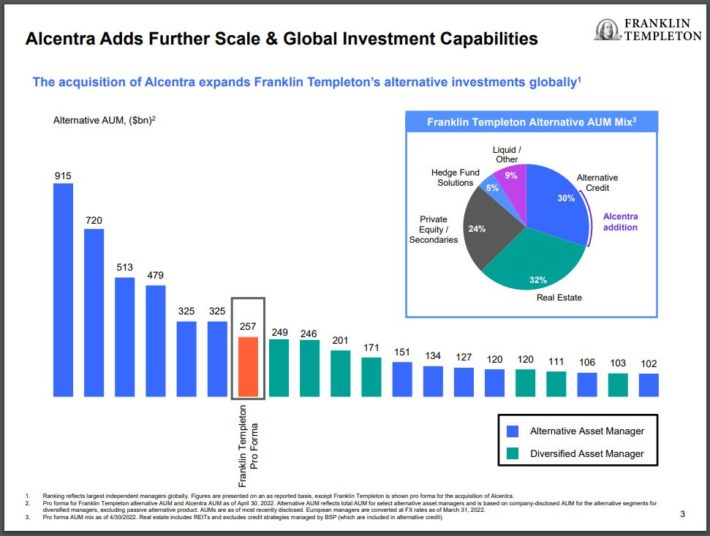

Subsequent, Franklin Assets has augmented its core enterprise by way of the usage of acquisitions, particularly in areas that the corporate doesn’t have as a lot of a presence. One such space is various investments, which incorporates non-public debt, structured credit score, high-yield funds, business actual property, and collateralized mortgage obligations.

To that finish, Franklin Assets has made a number of acquisitions over time to enhance the corporate’s positioning on this enviornment.

On April 1st, Franklin Assets introduced that it had accomplished its beforehand introduced buy of Lexington Companions, a number one international supervisor of secondary non-public fairness and co-investment funds, for $1.75 billion. This added $34 in AUM to Franklin Assets and prolonged the corporate’s footprint in various investments.

Extra just lately, Franklin Assets introduced on Might thirty first that it had agreed to accumulate Alcentra Group Holdings from The Financial institution of New York Mellon Company (BK) for as much as $700 million. Alcentra has $38 billion in AUM and can double Franklin Assets’ various credit score capabilities in Europe. Following the shut of this transaction, the corporate shall be one of many bigger names in various investments, an area Franklin Assets had restricted scope just some years in the past.

Supply: Investor Presentation

As well as, Franklin Assets has lowered its share rely by a mean of two.5% per yr during the last decade. The corporate repurchased virtually 3 million shares of inventory in the newest quarter because it stays dedicated to returning capital to shareholders.

Given the dimensions of the corporate’s AUM, bolt on acquisitions, and share repurchases, we mission that Franklin Assets will develop earnings-per-share at a charge of three% per yr over the subsequent 5 years. This progress charge is sort of in-line with the common for the final decade.

Aggressive Benefits & Recession Efficiency

Asset administration is a really aggressive area that doesn’t afford a selected firm any main aggressive benefits.

That stated, Franklin Assets does seem to have a leg up on the competitors given its title and fund efficiency over the long-term.

The corporate has the AUM that it does as a result of its funds have outperformed friends, which attracts new traders. Franklin Assets’ long-term mutual funds have had robust returns during the last one-, five-, and 10-year intervals of time relative to competing funds, exhibiting that Franklin Assets’ methodology for investing works over a number of time frames. Almost half of Franklin Assets’ funds are rated 4 or 5 stars by Morningstar.

Performances like this are seemingly a driving drive behind the corporate’s capability to draw capital.

The draw back to the asset administration enterprise is that recessionary intervals may be tough for corporations to navigate. Beneath are Franklin Assets’ annual earnings-per-share outcomes earlier than, throughout, and after the final recession:

- 2006 earnings-per-share: $1.85

- 2007 earnings-per-share: $2.37 (28% improve)

- 2008 earnings-per-share: $2.24 (5.5% lower)

- 2009 earnings-per-share: $1.30 (42% lower)

- 2010 earnings-per-share: $2.12 (63% improve)

- 2011 earnings-per-share: $2.89 (36% improve)

Earnings-per-share for Franklin Assets declined 45% peak to trough from 2007 to 2009, which wasn’t uncommon for a corporation within the asset administration trade. The corporate did see a fast rebound the very subsequent earlier than setting a brand new excessive for earnings-per-share in 2011, pointing to the energy of Franklin Assets’ enterprise mannequin.

Importantly for revenue traders, Franklin Assets continued to develop its dividend all through the final recession, with shareholders receiving a complete dividend improve of 47.4% for the interval. The corporate has a dividend progress streak of 42 consecutive years, which has earned Franklin Assets the title of Dividend Aristocrat.

And with a projected payout ratio of simply 31% for 2022, Franklin Assets is poised to proceed elevating its dividend for years to return. Shares yield 4.6%, which is sort of 3 times the common yield for the S&P 500 Index.

Valuation & Anticipated Returns

Franklin Assets is at present buying and selling at simply 6.8 occasions anticipated earnings-per-share of $3.71 for the yr. For a lot of the final decade, the inventory has traded with a low double-digit price-to-earnings ratio.

Given the competitiveness of the asset managed enterprise, we consider {that a} goal price-to-earnings ratio of 9 for the inventory is suitable as this takes into consideration Franklin Assets’ title and efficiency with the competitiveness of the trade.

If the valuation had been to increase to fulfill our goal by 2027 then Franklin Assets would see a 5.7% annual tailwind from a number of enlargement.

Subsequently, we mission that Franklin Assets could have whole annual returns of 12.3% over the subsequent 5 years, stemming from a 3% earnings progress charge, a beginning yield of 4.6%, and a mid-double-digit contribution from a number of enlargement.

Remaining Ideas

In occasions of market volatility, we recommend traders contemplate proudly owning blue chip shares. Franklin Assets, with a dominate management place in its trade and greater than 4 many years of dividend progress, has all of the makings of blue chip title.

Simply as necessary, the inventory may present annual returns within the low double-digit vary primarily based on modest earnings progress, a secure excessive yield, and the potential for an increasing a number of. In consequence, Franklin Assets earns a purchase advice from Positive Dividend as a result of projected returns.

For these causes, we view Franklin Assets as a high-quality blue chip inventory that might present traders wonderful whole returns.

The Blue Chips checklist will not be the one strategy to shortly display for shares that repeatedly pay rising dividends.

Thanks for studying this text. Please ship any suggestions, corrections, or inquiries to [email protected].

:max_bytes(150000):strip_icc()/Beans-a5fd4ef5f4ca4b36a7e28f419c487bb3.jpg "6 Healthiest Beans to Add to Your Meals for More Fiber and Protein")

{kind=link}