Rates of interest have been held at 4.5 per cent by the Financial institution of England (BoE) throughout mounting international uncertainty and rising commerce tensions sparked by Donald Trump.

That was the extent reached in February when the Financial Coverage Committee (MPC) made its first reduce since November final 12 months, in so doing bringing the speed right down to its lowest stage since mid-2023. March’s resolution noticed the MPC members vote 8-1 in favour of sustaining the 4.5 per cent price – with one vote for one more 0.25 proportion factors reduce.

Whereas the rate of interest is predicted to fall additional this 12 months, solely two extra cuts are anticipated in 2025 because the BoE tries to take care of a lid on inflation, whereas prices rise for companies and the broader financial outlook stays unsure.

A good portion of that uncertainty is because of Donald Trump’s commerce tariffs being positioned – and altered or withdrawn at quick discover – which has created unrest in industries and will see the price of promoting their items to the US rise considerably. Whereas the UK has but to implement any retaliatory tariffs, an escalating commerce battle might considerably hit financial progress in addition to shoppers’ spending energy.

The UK rate of interest stays above the eurozone price, which the European Central Financial institution reduce to 2.5 per cent earlier this month, whereas on Wednesday, America’s Federal Reserve opted to pause its personal cuts, leaving borrowing charges at 4.25-4.5 per cent.

The BoE utilises the rate of interest as one of many methods to aim to manage inflation, with a goal price of two per cent.

Andrew Bailey, governor of the Financial institution of England, mentioned: “There’s a whole lot of financial uncertainty for the time being. We nonetheless suppose that rates of interest are on a regularly declining path, however we have held them at 4.5 per cent in the present day.

“We’ll be wanting very intently at how the worldwide and home economies are evolving at every of our six-weekly rate-setting conferences. No matter occurs, it is our job to guarantee that inflation stays low and secure.”

Inflation’s influence

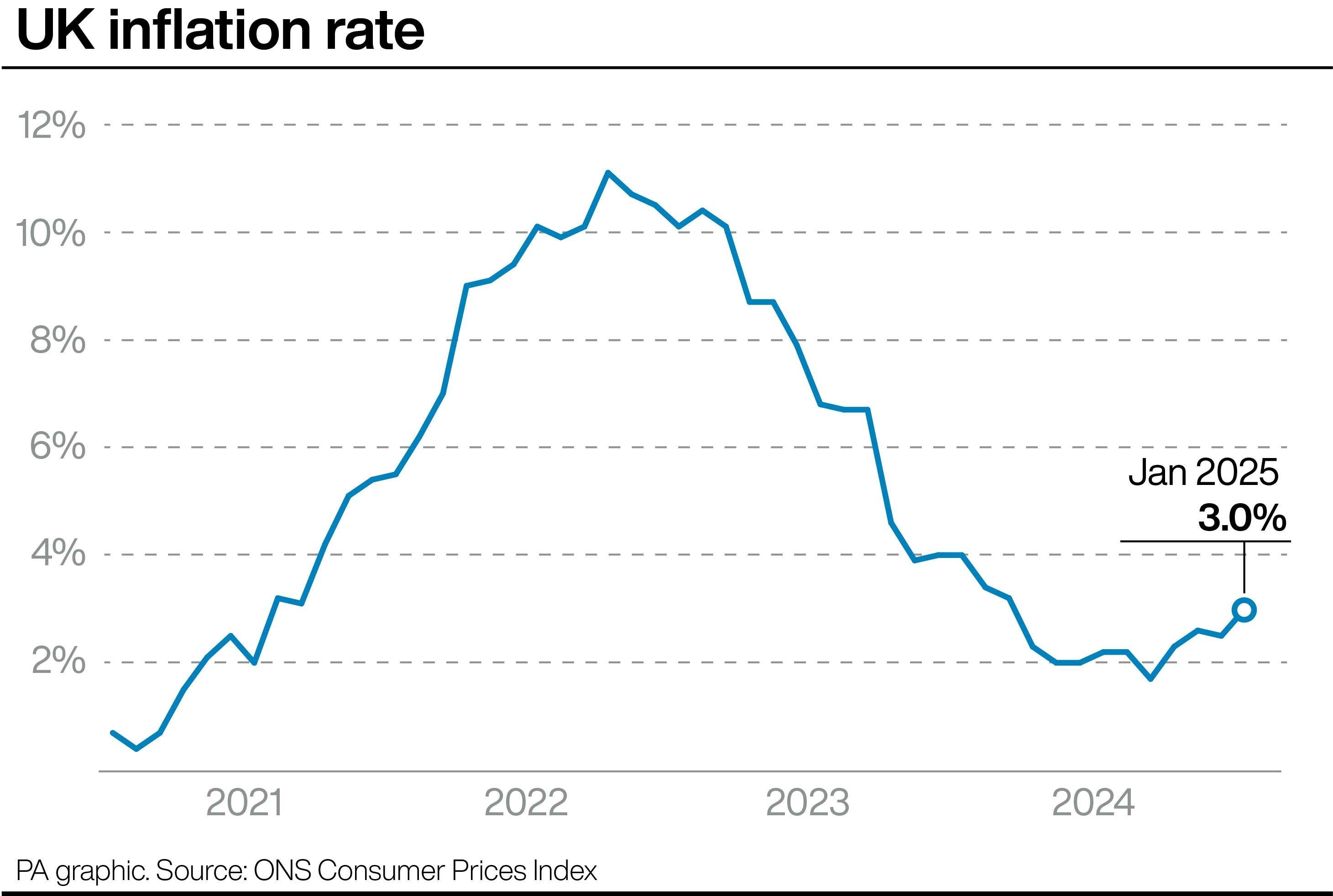

When the BoE made the Financial institution Price reduce final month, inflation had been on the decline. Nonetheless, a mid-February report confirmed Shopper Costs Index (CPI) inflation rose to three per cent in January, from 2.5 per cent in December.

With inflation due to this fact rising once more – and, importantly, rising by greater than anticipated – rates of interest had been all the time unlikely to be reduce this time round.

Decrease rates of interest can be utilized to encourage companies to renew investing as the price of borrowing is decrease, which may give the broader economic system a lift.

Nonetheless, it may possibly additionally result in rising costs as funding in additional jobs or salaries imply folks have, and spend, more cash; due to this fact the reverse can be seen as true in that if demand is decrease, it may possibly assist scale back these potential worth rises – or in different phrases, it may possibly assist stem inflation.

The BoE have said they’ll take a cautious strategy to decreasing the rate of interest in order to not see a pointy spike in inflation, as was seen a few years in the past.

Mortgages, financial savings and companies

Rates of interest are a double-edged sword for households. On the one hand, the upper it’s, the higher it’s for these with cash in financial savings accounts as they earn a better return on their money.

Reverse aspect of the see-saw to savers sit householders. Mortgages can naturally change into costlier when curiosity repayments must go up based mostly on an growing rate of interest.

Mounted-term offers negate the must be involved over adjustments, however after a fast enhance in prices over the previous two years many owners would have been hoping for larger cuts this time round.

“Whereas the central financial institution has prevented including gas to the hearth, the federal government should now take decisive motion. Merely ready for rates of interest to chill inflation isn’t a plan. Savers want consistency and assist to revive confidence of their monetary future,” mentioned Lily Megson, coverage director at My Pension Skilled.

“With the chancellor’s spring assertion quick approaching, we are able to solely hope for a renewed give attention to making certain folks can save sufficient for a safe monetary future.”

David Hollingworth, affiliate director at L&C Mortgages, famous that because the maintain had been anticipated, it ought to trigger “barely a ripple within the mortgage market” this time round.

For companies, whereas no change to rates of interest means short-term continuity when it comes to borrowing prices, the looming spring assertion subsequent week is an even bigger issue forward of elevated labour prices coming into play – particularly set in opposition to the backdrop of commerce tariffs.

“Tariffs imply costs and prices will inevitably go up and this can be a lose-lose state of affairs for shoppers, companies, and financial progress. Extra tariffs are additionally on the agenda for the beginning of subsequent month which can add contemporary uncertainty into the combination,” mentioned William Bain, head of commerce coverage on the British Chambers of Commerce (BCC).

Outlook for 2025

Most analysts are nonetheless anticipating two additional charges cuts in 2025, which exterior of mortgages and financial savings accounts can nonetheless have an effect on the whole lot out of your weekly store to vitality payments.

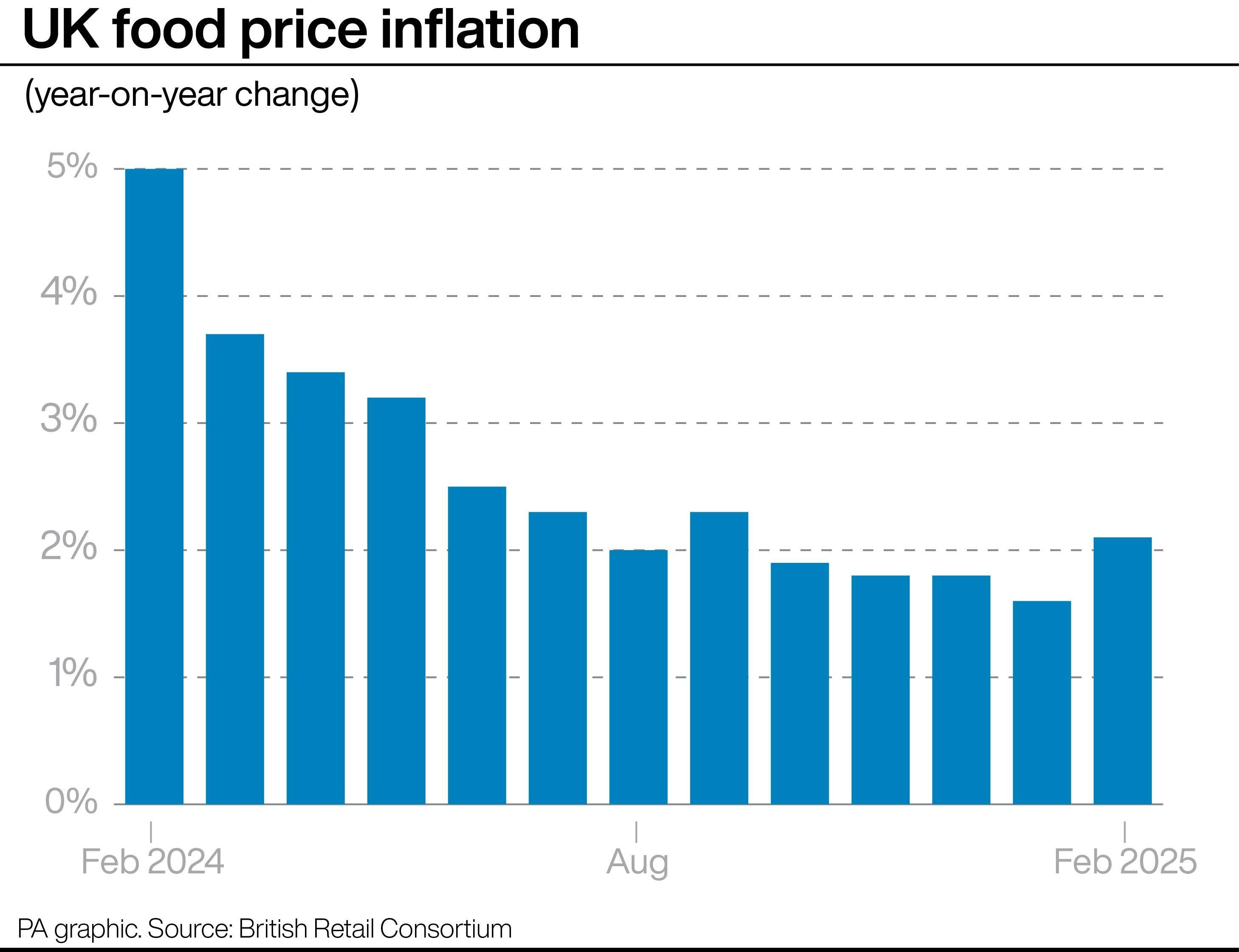

Whereas the goal is to decrease inflation to 2 per cent, it’s not often a straight-line trajectory and the recommendation is to count on a bumpy experience, significantly when it comes to meals value inflation later in 2025, which is predicted to rise.

“It has been a turbulent few weeks, each economically and politically, so a cautious strategy appears justified whereas the info stays so unsure,” mentioned Victor Trokoudes, CEO of Plum.

“The BoE has a lot to contemplate. Inflation is now forecast to extend additional to three.7 per cent as a result of larger vitality prices and controlled costs. Fuel and electrical, water and broadband prices in addition to council tax are all as a result of considerably rise in April, which provides inflationary stress in addition to usually damaging folks’s day-to-day funds. These inflationary worries ought to seemingly ease considerably later within the 12 months, however till then the BoE might want to stay vigilant to rising costs.

“Added into the combination are political elements. Additional public spending is required on defence as a result of current international developments, and employment tax will increase are coming into impact shortly as nicely. And that’s earlier than you have in mind the looming menace of elevated tariffs underneath the brand new Trump administration within the USA, although there are hopes that the UK’s commerce stability with the USA places it in a greater place than others to keep away from a heavy influence right here.”

It additionally stays to be seen how these incoming extra enterprise prices in April translate to companies and folks’s pockets, so whereas a decreasing rate of interest throughout the 12 months is predicted, it’s very a lot wait-and-see territory as to when that may occur – although economists at The Pantheon say it could possibly be Might and November this 12 months.

It stays difficult nonetheless, if you happen to’re seeking to remortgage, transfer your cash or in any other case handle your funds, to know when the precise greatest second to take action might be, with Rachel Reeves’s spring assertion subsequent week the following massive date to mark within the calendar for brand spanking new data.

")

{kind=link}