Rob Stothard/Getty Photographs Information

On January 18, 2022, Microsoft (MSFT) introduced its acquisition of Activision (NASDAQ:ATVI) for $95 per share in an all-cash transaction. ATVI’s share worth continues to hover round ~$80 as buyers stay skeptical about whether or not the regulators will approve the transaction and uncertainty relating to the upcoming shareholder vote.

Primarily based on an anti-trust evaluation evaluation, I imagine the FTC will finally approve the transaction. Draw back danger stays capped even when the FTC approval doesn’t pan out, making ATVI a horny merger arbitrage alternative with an ~18% upside inside 14 months.

Vertical Or Horizontal Merger?

Given the dimensions of the transaction, the extra request for data from FTC is inevitable. The FTC will then assess whether or not the acquisition is a vertical or horizontal merger. The previous refers to an acquisition of an organization offering a special service (normally a part of the provision chain) from the acquirer, whereas the latter refers to an acquisition of a direct competitor.

Vertical Merger

Vertical mergers had remained unchallenged for over 20 years until lately. There have been three mergers challenged: Illumina-Grail, NVIDIA-ARM and Lockheed Martin-Aerojet Rocketdyne. The primary was consummated and is presently present process court docket proceedings. Whereas the latter two offers had been deserted. The explanation cited for disapproval of all three mergers was constant, being {that a} sole provider of important downstream enter was being acquired.

There was a consensus that the FTC will view the merger as a vertical merger. The explanations are (i) MSFT’s key revenue-generating segments stay the Workplace and Home windows companies and (ii) Xbox being a platform with gaming content material as a downstream enter.

Provided that ATVI doesn’t present “important” gaming content material inputs, FTC may have a tough time denying the merger if it views it as a vertical one. Additional, there’s a multitude of profitable media content material consolidation priority in assist of an MSFT-ATVI merger (suppose Disney-Fox, Discovery-WarnerMedia and Amazon-MGM).

Shoppers might be harmed and competitors stifled if MSFT was to transform standard titles like Name of Responsibility to Xbox exclusives. Nevertheless, MSFT has confirmed that a minimum of Name of Responsibility will stay obtainable on the PlayStation platform. As such, there stays no purpose for FTC to disclaim this merger from a vertical merger standpoint.

Horizontal Merger

It may be argued that the merger is a horizontal one given MSFT’s presence within the sport publishing house with video games like Halo, Minecraft, Forza and Gears of Warfare. This presence has since expanded with the acquisition of ZeniMax Media (owns The Elder Scrolls and Fallout IPs amongst others).

The FTC might be following the Horizontal Merger Tips revealed in 2010. These pointers concentrate on the opposed aggressive impact on prospects be it pricing, high quality, selection, service or innovation. The proof of such opposed aggressive impact might be (i) priority of opposed aggressive impact, (ii) lack of a considerable head-to-head competitor, (iii) elimination of a “maverick” and (iv) change in market focus.

Priority of opposed aggressive impact

The FTC will evaluation the historic influence of latest mergers, entries, expansions or exits within the video gaming market or comparable markets to find out the aggressive influence of the merger. There may be restricted historic priority within the business for acquisitions of ATVI’s measurement. The closest is Tencent buying a majority of Supercell for $8.6 billion. This acquisition didn’t immediate any worth improve, as an alternative, the costs of digital items went down.

The same priority that the FTC may reference could be the Disney-Fox merger. Each mergers are comparable by way of the acquisition measurement and being within the leisure content material class. The Disney-Fox merger ended up as a plus for shoppers. They had been capable of benefit from the big library of Disney-Fox content material supplied by way of Disney Plus at a cheaper price level than Netflix.

Given the above precedences had a constructive influence on shoppers, the FTC will discover it difficult to disclaim the merger on such grounds.

Lack of a considerable head-to-head competitor

MSFT and ATVI are opponents for certain, particularly within the first-person participant shooter (“FPS”) style. Nevertheless, it could be difficult to argue that they’re substantial head-to-head opponents given the large vary of standard alternate options. These alternate options, which can be found on each consoles and PC, are priced as little as free within the case of Fortnite, Apex Legends and Group Fortress 2.

Elimination of a “maverick”

A “maverick” is a agency that disrupts the business be it via new know-how, enterprise mannequin or resisting worth will increase. Elimination of such a agency will doubtless result in an opposed aggressive influence given its disruptive impact on the business.

ATVI has not purchased something new to the desk lately. It has caught to its tried and examined franchises – Name of Responsibility, Sweet Crush and World of Warcraft. There have been incremental gameplay enhancements, however innovation remained missing. The enterprise mannequin has remained the identical and it has been following the normal gaming pricing mannequin. It could be truthful to say that ATVI has not been a disruptive firm within the gaming business for a protracted whereas. As such, no “maverick” is being eradicated on this merger.

Change in market focus

If any, this could be the probably cited purpose by the FTC to disclaim a merger. Whereas making an attempt to find out the change in market focus, how the market is outlined issues. FTC has denied mergers on grounds of elevated focus in a narrowly outlined market. A distinguished instance is the 1997 Staples-Workplace Depot merger, the mixed firm would solely management 6-8 % of the general workplace merchandise market (barely important share). Nevertheless, the decide blocked the merger in acceptance of FTC’s “workplace provide superstores” market definition. The merger try was once more blocked in 2015 utilizing “B-to-B workplace provide” market definition.

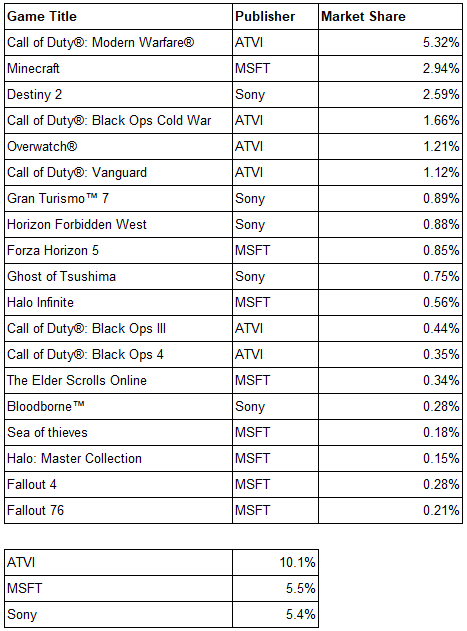

Desk 1: Market share of prime 50 video games on PlayStation & Xbox revealed by Sony, MSFT & ATVI (measured in time performed in March 2022)

Writer analysis

If one was to slim the market to video games on PlayStation and Xbox solely, the rise in market focus via the merger is 5.5%. The market share analysis in Desk 1 highlights the fragmented nature of the market. Even a longtime big participant like ATVI holds solely about ~10% of the market. A mixed ATVI-MSFT market share of ~16% is nowhere near holding monopolistic energy.

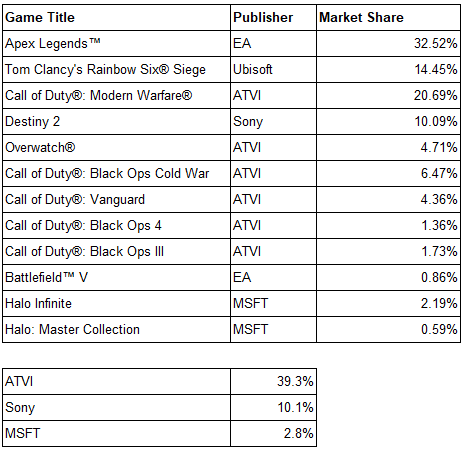

Desk 2: Market share of prime FPS video games on PlayStation & Xbox revealed by Sony, MSFT & ATVI (measured in time performed in March 2022)

Writer analysis

If one was to slim the market additional all the way down to the first-person shooter (“FPS”) style on PlayStation and Xbox solely, the rise in market focus is lower than 3% (Halo collection). As per Desk 2, ATVI does have a domineering market share within the FPS style. Then again, MSFT has a restricted presence on this style because the Halo collection is just obtainable on Xbox and its reputation stays far behind that of Name of Responsibility.

Each market share evaluation highlights that there might be a restricted improve in market focus. Thereby, a problem by FTC on such grounds might be unlikely to go muster.

Why The Enormous Unfold?

There are two key uncertainties behind the large unfold: (i) the necessity for a majority shareholder vote and (ii) altering merger regulatory atmosphere.

Shareholder vote

Shareholders may vote to reject the merger. It’s normally led by activist buyers with important stakes within the firm. Given there has not been any activist opposition thus far and solely a easy majority is required, I imagine the vote will go with no difficulty.

Altering regulatory requirement

The FTC has acknowledged that will probably be reviewing supplies not lined within the pointers resembling client information entry, influence on the sport developer labor market and influence on mistreated workers. Given the office harassment considerations at ATVI, FTC will doubtless focus its consideration on labor points.

Recreation publishing studios have traditionally been identified to have poor working situations with pressured extra time, poisonous tradition and low pay. The business has been capable of get away with it as labor provide far outstrips demand. I extremely doubt the MSFT-ATVI acquisition will change that business labor dynamics.

I’d say that MSFT has among the higher office tradition within the business. Studying from its errors of extreme involvement in Lionhead Studios (developer of the Fable collection), MSFT has since taken a hands-off strategy to acquired studios. This has labored properly in lots of instances with few complaints heard. Certainly one of its acquired builders, Playground Studio, was even named among the finest locations to work.

Nonetheless, MSFT additionally has its share of office points in one in all its studios, Undead Labs. The office points appear to have come about because of the departure of its founder. However MSFT has since taken corrective actions in pushing out the concerned HR govt and investing in range and inclusion.

MSFT’s emphasis on office tradition can also be evident in giving up on working with an acclaimed studio, Moon Studios (developer of the favored Ori collection), as a result of poisonous office tradition. Certainly one of its key executives, Bonnie Ross, Head of 343 Industries (developer of Halo Sequence post-MSFT’s cut up with Bungie), has been instrumental in driving range within the gaming business.

I imagine MSFT is well-positioned to right the poisonous office tradition at ATVI, which is probably going the rationale why it went forward with the acquisition. ATVI below MSFT will probably be a significantly better working atmosphere for present sport builders. With that in thoughts, I discover little purpose why the FTC ought to cease this acquisition.

Draw back Capped

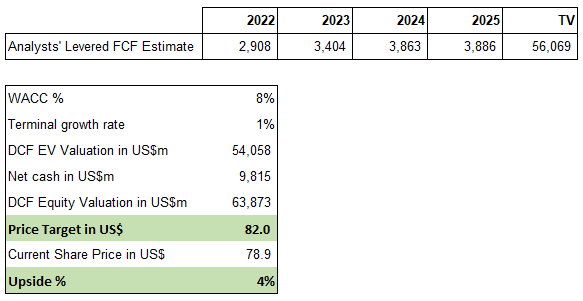

Determine 1: ATVI DCF Valuation (submit failed acquisition)

Writer analysis, Merely Wall St as of Apr 22, 2022

Primarily based on analysts’ free money move projections, a conservative discounted money move valuation as per Determine 1 will yield a worth goal of US$82. The valuation accounts for a $3 billion payout by MSFT ought to the acquisition fail as a result of antitrust points.

The share worth will tumble submit the information of a failed acquisition doubtless as a lot as 13% to $69 (ATVI’s pre-acquisition worth of $65 + $4 in money termination payment paid out per share). Nevertheless, ATVI stays a enterprise with robust IPs that may proceed to generate robust money move. Its share worth will finally get better from the one-off failed acquisition shock and commerce at its intrinsic worth of US$82.

Nonetheless, if an investor is unwilling to attend for the corporate to commerce at its intrinsic worth, a low 13% draw back likelihood versus a excessive 18% upside likelihood stays a horny risk-to-reward profile.

Timeline

Given the dimensions of the transaction, the events predict the conclusion of the merger by June 18, 2023 (last extension deadline). MSFT might be on the hook for US$2-3 billion ought to the merger be terminated as a result of antitrust points.

The particular shareholder assembly to resolve whether or not to proceed with the merger might be held on April 28. A majority vote is required else the merger settlement might be terminated.

Within the meantime, MSFT/ATVI might be compiling and submitting the knowledge as requested by the FTC. In line with the steerage, the FTC has 30 days to evaluation the submitted supplies. However the FTC has been identified to take far longer, which is able to doubtless be the case for such a distinguished merger. My projection is the approval will are available in Q1 2023.

Conclusion

It’s plain that there’s danger concerned else a diffusion won’t exist. Nevertheless, on this particular case, it appears the market has drastically overestimated the dangers resulting in a horny arbitrage situation.

2026-03-05")

")

{kind=link}