RapidEye/iStock via Getty Images

By Peter C. Earle

Media coverage of inflationary effects primarily focuses on the impact of rising price levels upon consumers and producers, but there are clearly effects beyond those. As monetary authorities initiate policies intending to stem the upward trend of prices, financial markets may become more volatile than normal. Should inflation prove stubborn, or particularly unpredictable and thus difficult for contractionary monetary policy to counteract, financial markets may become excessively volatile. High levels of volatility dissuade investment, and at very high levels, careening markets may pose a threat to financial stability. In either case, the prices that guide economic calculation become less reliable. Supply- and demand-driven changes in relative prices, which provide information to entrepreneurs and seasoned managers alike, can be completely masked by broad moves in the general price level.

Early in the pandemic, the Federal Reserve undertook one of the fastest quantitative easing campaigns in its then 107-year history, under conditions ostensibly necessitating such actions. But like all major government programs, unintended consequences are likely; we may be experiencing some early effects at present.

US Public Debt (5 years)

(Source: Bloomberg Finance, LP)

For both the US and the UK, inflation is taking a toll on sovereign (government-issued) bond markets. For several reasons, the typical purchasers of US Treasury bonds have been stepping away from the market. Treasury bond yields are used as the global proxy for the “risk free rate,” a variable that impacts countless financial and economic calculations all over the world. If the market for US government bonds were to soften materially, the pricing of countless other instruments could be impacted. A loss of confidence in the reliability of bond prices could have massive ripple effects with negative implications for the entire world’s financial system. There have already been warnings that this risk “poses one of the greatest threats to global financial stability today, potentially worse than the housing bubble of 2004-2007.”

In the quest to determine causes, the most fundamental consideration is the prevailing forces of supply and demand. The massively expansionary fiscal programs of the past few years show clearly that the supply of US Treasury bonds has been torrential. As has been pointed out elsewhere, it may well be that the global appetite for US government securities has been sated, at least for the moment. Whether we are discussing ice cream cones or US Treasury bills, demand curves (almost) universally slope downward. As the cost of a good increases, the quantity demanded decreases. Moreover, there are potential buyers all along the curve. Those beneath the equilibrium price would be willing to consume should the price fall to lower levels, while those above would continue to purchase the good even if the price were to increase.

Federal Reserve balance sheet (5 years)

Source: Bloomberg Finance, LP

This fall in market demand was precipitated by major outflows of US sovereign debt from foreign buyers, Japan chief amongst them. Japan’s central bank and numerous Japanese pension funds sold $2.4 billion worth of US treasuries last May alone, after six months of persistent sales that constituted the “longest streak of outflows in data going back to 2005.” Japan’s efforts had been undertaken to deal with its own currency problems, but also due to wariness over continued US inflation. The People’s Bank of China also sold US bonds, and the IMF estimates that central banks in emerging markets have reduced their holdings of U.S. debt by a cumulative $300 billion so far this year.

The biggest drop in demand has come from the Federal Reserve, which “plans to offload Treasuries from its balance sheet to $60 billion a month.” This transition, called the balance sheet “runoff,” constitutes a massive change in US monetary policy. For the past few decades, the Federal Reserve has been a major buyer of US Treasuries (and other instruments), and after essentially supporting that market for years, the reversal of the policy is being felt acutely. For conditions to remain as they were, the withdrawal of demand previously provided by the Fed must now be made up by other buyers. But high debt loads, rising inflation, and the slowing of growth globally has foreign governments and large international financial firms wary of buying US debt. As a result, Bloomberg reports that the “Bloomberg US Treasury Total Return Index has lost about 13 percent this year, almost four times as much as in 2009, the worst full year result on record for the gauge since its 1973 inception.” This has prompted some analysts to warn of an illiquidity spiral, in which “volatility creates more illiquidity, which leads to more volatility,” which in turn causes yet more illiquidity.

And this is not the first time waning interest in Treasuries has caused concern. Six months before anyone knew what COVID was, a crisis in the market for repurchase agreements (repos) had its roots in a similar dissipation of appetite for government securities. As McCormick and Mohsin wrote in Bloomberg, reprinted in Financial Advisor Online,

on Wall Street, bond dealers provided a small, but pointed reminder that, just maybe, debt and deficits do matter after all. It came in the form of a sudden spike in interest rates for repurchase agreements, or repos, a normally obscure part of finance that keeps the global capital markets spinning. Plenty of factors helped cause liquidity to dry up, but one that’s getting more attention is concern that dealers are starting to choke on Treasuries as the U.S. government goes deeper into the red … Primary dealers, which are obligated to bid at U.S. debt auctions, have absorbed more and more Treasuries to finance the Trump administration’s tax cuts as investor demand has waned. Typically, they rely on repos to fund those purchases by putting up the debt as collateral. The problem is that with the financial system already inundated by over $16 trillion of Treasuries, banks constrained by crisis-era rules have fewer incentives to participate in repo. Simply put, there was too much new debt flooding the financial system and not enough money, causing lenders to jack up repo rates.

At that time, the outstanding US public debt was roughly $22 trillion. Now, with the total almost $10 trillion higher, real concerns regarding the financing of massive budgets should be a topic of preeminent importance.

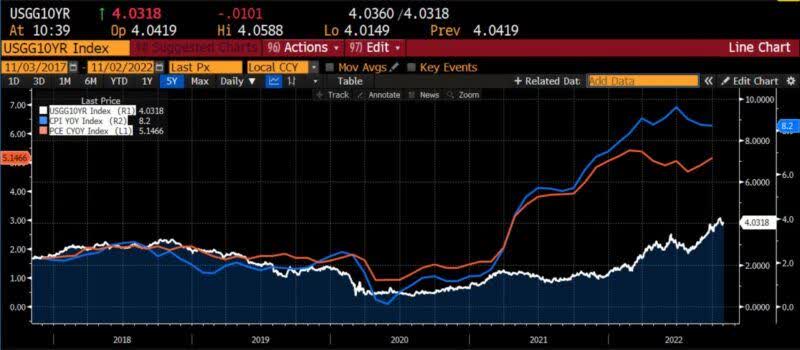

Headline CPI (year-over-year), Personal Consumption Expenditure (year-over-year), and Generic 10-year US Treasury yield (5 years)

Source: Bloomberg Finance, LP

Instead, Treasury Secretary Janet Yellen has hinted that the US Treasury may buy back Treasury bonds, and earlier this month the Treasury called primary dealers to discuss the details of those repurchase operations. In the past, repurchases of treasuries tended to occur during periods of fiscal surplus. But this time the situation is fundamentally different, and it is still uncertain how these goals will be achieved. The Treasury may use a variation of Operation Twist, which the Fed employed in 2012, by essentially injecting liquidity into the market by raising short-term Treasury debt and lowering long-term Treasury rates. The reputation of that program is controversial, however, and there is concern that this policy would clash with the Fed’s deflationary efforts. The path forward is unclear, as the rise in yield rates necessary to induce greater demand could also mean higher costs of lending for both private and public actors.

Though a central tenet of the Fed’s mission is price stability, its recent performance has been sharply dissonant with that principle for several reasons: additional mandates, political pressure, and more recently DEI distractions. The Federal Reserve is inarguably culpable for the current inflationary dilemma, first due to its expansionary monetary policies, and then for not arresting the consequent upward trend in prices in a timely manner. Americans would do well to recognize that in the midst of a fight against inflation, a sudden turn to expansionary monetary policy is an unlikely (but not impossible) policy shift. If, on top of that, global demand for US Treasuries remains low and financing the existing debt becomes increasingly costly, taxation is essentially the only available means by which the US government can finance its insatiable expansion. Hopefully, a path forward becomes clear and a lesson is learned, as to the knock-on effects that attend not only excessively loose monetary policy, but fiscal profligacy as well.

Original Post

Editor’s Note: The summary bullets for this article were chosen by Seeking Alpha editors.

2026-02-27")

{kind=link}