J Studios/DigitalVision via Getty Pictures

Prolonged-time readers know I’ve been bullish on short-term and variable price bonds since mid-2021, as skyrocketing inflation was practically really going to result in bigger fees. I’ve been bullish on senior mortgage ETFs too, along with the benchmark Invesco Senior Mortgage ETF (NYSEARCA:NYSEARCA:BKLN), in spite of their extreme expense ratios, as monetary conditions appeared favorable enough to beat their payments.

Monetary conditions appeared to have stabilized by now, with below-target inflation and (practically positive) price cuts inside the coming months. Beneath these conditions, senior loans are unlikely to materially outperform, BKLN’s 0.65% expense ratio is an important drag on its effectivity, and a deal-breaker for me. As such, I’d not be investing inside the fund in the meanwhile.

BKLN – Overview and Analysis

Method and Portfolio

BKLN is an index ETF specializing in senior loans, which might be practically always senior secured variable price loans from non-investment grade corporations. BKLN’s underlying index is kind of broad, so the fund must switch alongside senior loans as an asset class, with out essential under or overperformance.

BKLN in the meanwhile invests in over 160 loans. Largest of these are as follows:

BKLN

Curiosity Cost Hazard

Some context first.

Most bonds are fixed-rate bonds, and so pay the an identical coupon from issuance until maturity. Buy a 4.25% yielding 10y treasury instantly, and also you’ll get hold of 4.25% in earnings yearly for the next ten years, it doesn’t matter what the Fed or the market does.

Fees on treasuries issued eventually may change though. Very important price cuts later inside the yr would practically really lead to lower coupon fees for treasuries issued later inside the yr, older issuers would retain their bigger fees. Investor demand for these older, higher-yielding treasuries would enhance, leading to bigger prices. Bond funds invariably give consideration to older bonds, and so would see capital options / bigger share prices from essential price cuts.

Lower fees would have the choice affect.

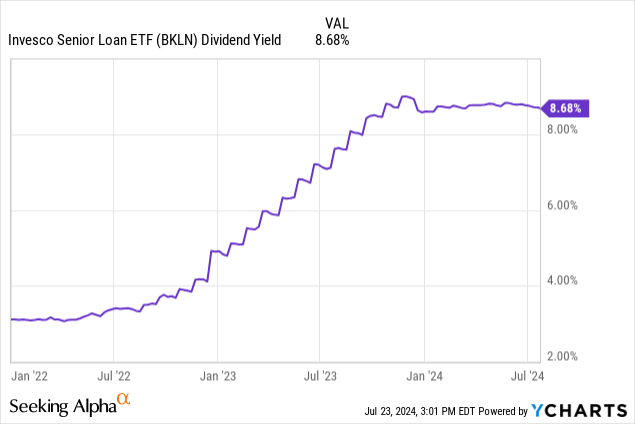

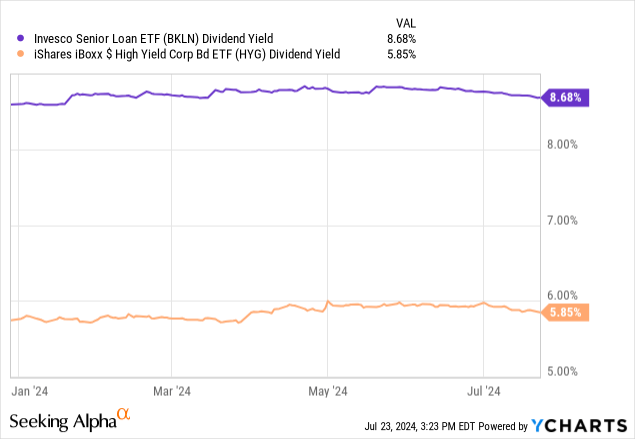

Senior loans are not fixed-rate investments, nonetheless variable. Simplifying points a bit, senior loans are listed to explicit benchmark fees, and see bigger coupon fees when the Fed hikes, and vice versa. BKLN’s yield has elevated by 5.7% as a result of the Fed started to hike, broadly in-line with Fed hikes.

Information by YCharts

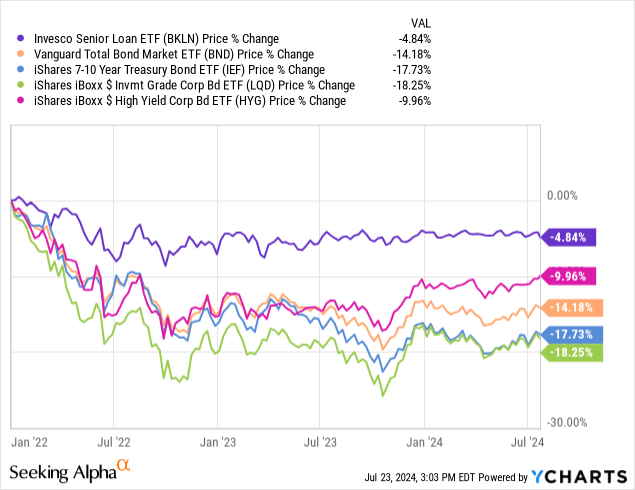

Because of above, senior mortgage prices normally usually are not significantly impacted by changes in charges of curiosity. For instance, BKLN’s share price is down solely 4.8% since early 2022, compared with double-digit declines for a lot of bonds and bond sub-asset programs.

Information by YCharts

Senior loans are inclined to outperform when fees rise, as has been the case since early 2022.

Information by YCharts

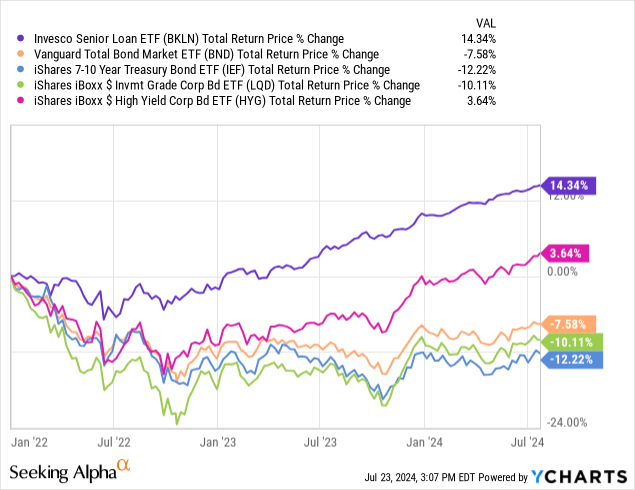

On the flipside, senior loans generally tend to underperform when fees decrease. Excluding the pandemic, closing time fees had been down was in 2022, all through which BKLN underperformed fixed-rate bonds of comparable credit score rating prime quality (high-yield bonds). It outperformed most bonds and treasuries though, ensuing from its above-average yield and credit score rating spreads tightening. Fees are positively not the solely consideration, nonetheless positively an very important one.

Information by YCharts

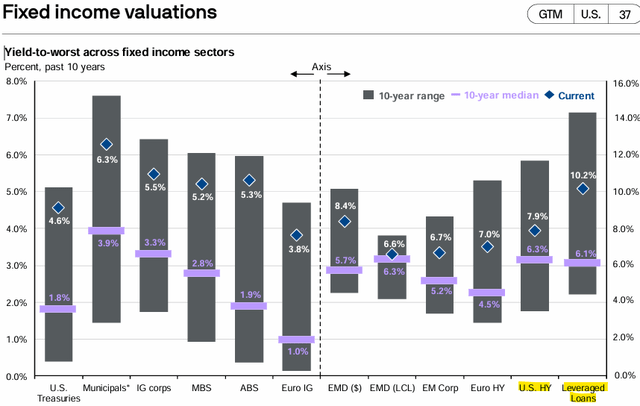

Senior mortgage and BKLN’s yield are every set to say no as a result of the Federal Reserve cuts fees later inside the yr. Every commerce with sizable spreads relative to high-yield bonds too, sizable enough that yields ought to remain aggressive for just some years. As per JPMorgan, spreads are at 2.3%.

JPMorgan Info to the Markets

BKLN itself yields 2.8% better than a very powerful high-yield bond ETF (spreads are tighter for just a few of its buddies though).

Information by YCharts

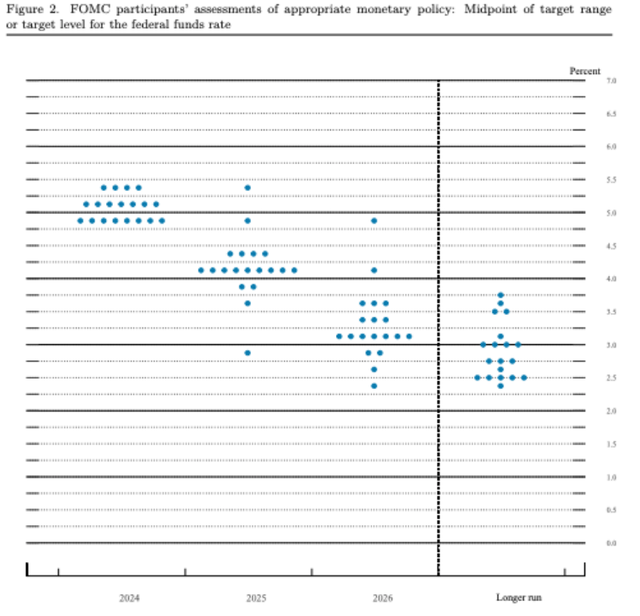

Current Fed steering implies senior loans persevering with to out-yield bonds until on the very least 2026, possibly long-term.

Federal Reserve

Beneath current market conditions, and considering Fed steering, senior loans might proceed to hold out pretty successfully even as a result of the Fed cuts fees later inside the yr. Yields ought to remain bigger than frequent for plenty of years, which ought to help stabilize share prices. Extreme-yield bonds would practically really outperform if fees plummet, nonetheless not if these keep bigger for longer, or see sluggish, methodical cuts.

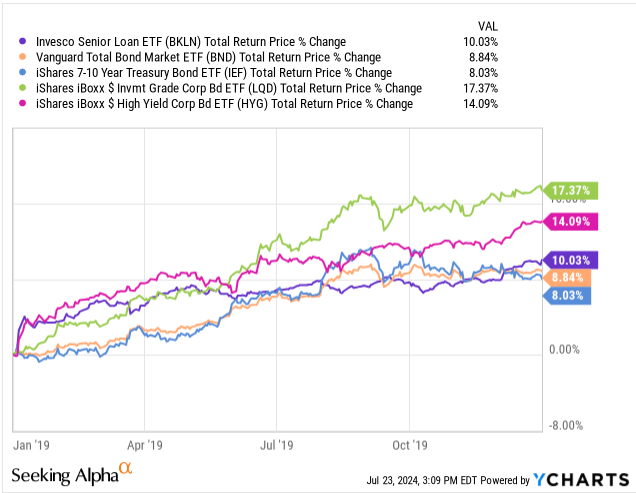

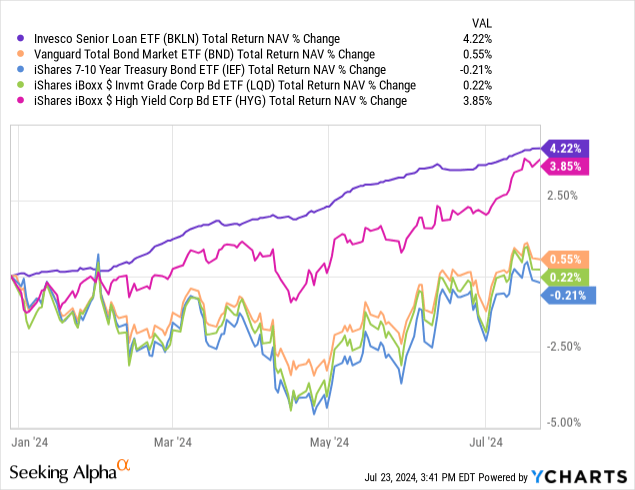

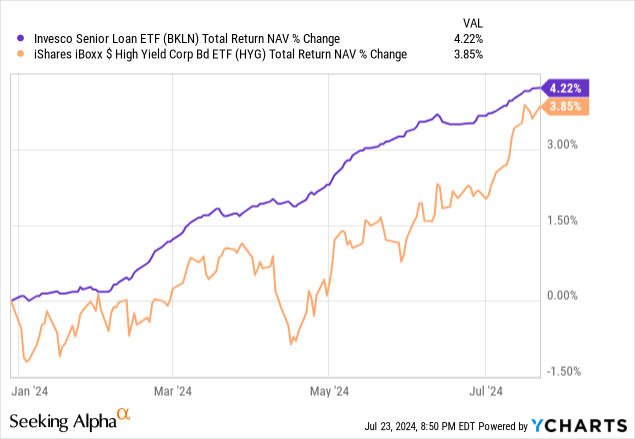

As a (partial) occasion of the above, BKLN has outperformed most bonds and bond sub-asset programs YTD though fees are flat. Outperformance may very well proceed if fees are solely cut back 0.25% – 0.50%, nonetheless additional essential price cuts would put rather a lot increased pressure on the fund’s effectivity.

Information by YCharts

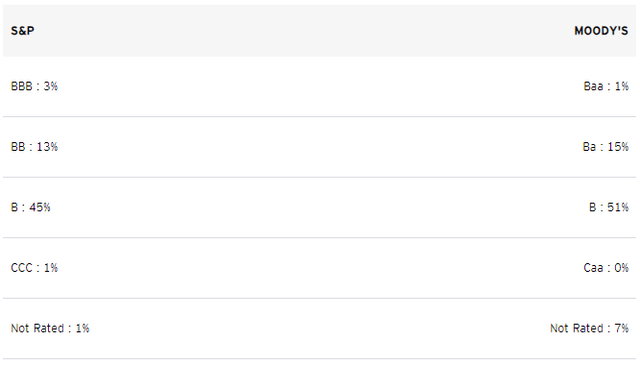

Credit score rating Hazard

BKLN focuses on non-investment grade loans, with these accounting for 97% – 99% of its portfolio, and with a imply credit score standing of B. Complete credit score rating prime quality is low and below-average, although not excessively so.

BKLN

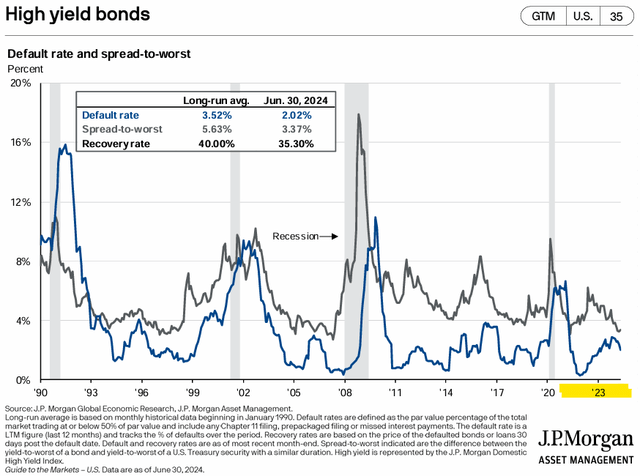

Current monetary conditions favor high-quality investment-grade investments and securities, not BKLN’s low-quality loans. Notably, credit score rating spreads have tightened as default fees rise, which means these riskier loans are seeing bigger risks, lower (comparative) yields, and below-average risk-adjusted returns and yields. Information as per JPMorgan, give consideration to the lower left of the graph.

JPMorgan Info to the Markets

The above is an important detrimental for the fund, and disadvantage relative to higher-quality variable price ETFs, along with the Janus Henderson AAA CLO ETF(JAAA) and the Janus Henderson B-BBB CLO ETF (JBBB).

Expense Ratio

BKLN has an expense ratio of 0.65%, bigger than frequent for an index ETF, and rather a lot bigger than that of plenty of sturdy ETFs. The SPDR Portfolio Extreme Yield Bond ETF (SPHY), for instance, has an expense ratio of solely 0.05%. JBBB costs 0.49%, comfortably lower than BKLN, though CLOs are significantly space of curiosity investments (a lot much less rivals, a lot much less pressure on fees). Senior mortgage ETFs are usually expensive, with the Franklin Senior Mortgage ETF (FLBL) having the underside expense ratio of 0.45%.

I’ve always considered BKLN’s expense ratio to be a serious detrimental, as a result of it primarily leads to lower yields and returns to shareholders. The reality that payments are a positive detrimental is important. There could also be a wide range of uncertainty when investing: valuations may certainly not improve, dividends may get cut back, the Fed may cut back or hike fees, and monetary conditions may improve or worsen. Payments are always a detrimental, so avoiding pricey funds is almost always helpful. Sufficiently favorable monetary conditions may outweigh extreme payments, they did for me earlier inside the yr, nonetheless conditions are merely not favorable enough. As such, and in my opinion, I’d not be investing in senior loans or BKLN correct now.

BKLN – Making an attempt Once more

I closing coated BKLN earlier inside the yr. I was bullish then, additional neutral now, so thought to elucidate my reasoning.

Briefly, spreads have tightened, charge of curiosity cuts are nearer, and uncertainty regarding inflation and the tempo of price cuts has decreased. These changes make senior loans a lot much less engaging investments than sooner than and have triggered my opinion on these to change.

One different drawback is that conditions YTD have been significantly favorable to senior loans, and BKLN has barely outperformed high-yield bonds since. Conditions should improve for effectivity to do the an identical, and I don’t merely don’t see how that may happen.

Information by YCharts

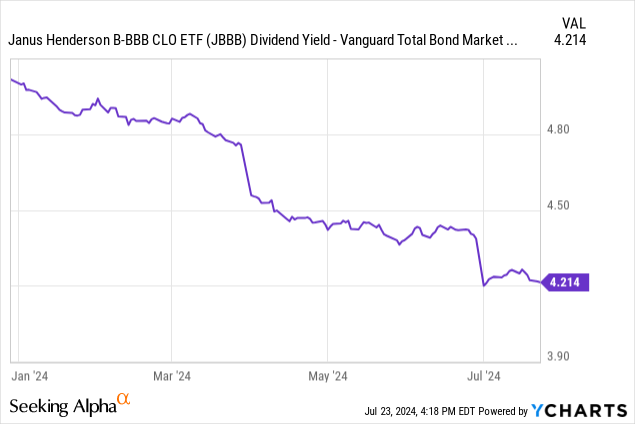

I keep bullish on cheaper, higher-quality variable price ETFs though, as these do commerce with healthful spreads relative to fixed-rate buddies. For instance, JBBB’s 7.6% dividend yield is spherical 4.2% bigger than that of most bonds. Steering is for decrease than 4.2% in long-term cuts, so JBBB’s dividend yield ought to remain aggressive long-term. Comparable state of affairs for plenty of completely different ETFs on this home, along with JAAA and CLOZ.

Information by YCharts

Conclusion

BKLN is an index ETF specializing in senior loans. BKLN’s above-average 0.65% expense ratio is a cloth drag on its effectivity, and a deal-breaker for me.

")

{kind=link}