Luis Alvarez

Funding thesis

Agora (NASDAQ:API) supplies a B2B platform for real-time communication and interplay by way of textual content, voice and video. The corporate’s APIs and SDKs enable builders to combine a number of communication channels of their purposes, with a larger focus in direction of video communication. The corporate differentiates itself by leveraging its expertise to ship distinctive stay video high quality which provides an enhanced consumer expertise. On the finish of Q1 final 12 months, the corporate was restructured into two impartial enterprise in order that its worldwide enterprise operated beneath the Agora model, whereas the Chinese language enterprise operated beneath the Shengwang model. The previous continues to point out strong development whereas the latter has confronted a number of headwinds resulting in income declines.

The corporate has demonstrated enhancing margins regardless of an absence of total income development by way of substantial expense reductions. Income development is anticipated to enhance in upcoming quarters because the enterprise is prone to profit from business tailwinds. The present market cap which is properly under the corporate’s web money displays a pessimistic view of the enterprise that I don’t share. Although upside will depend on the corporate demonstrating strong natural development and reaching FCF breakeven, draw back is restricted by its sturdy money place and diminished money burn. In the meantime administration continues to leverage its steadiness sheet energy to repurchase shares at discounted costs. I price shares a maintain as I wait to achieve larger confidence in upcoming quarters that the corporate is on a sustainable path in direction of worthwhile development.

Q1 earnings assessment

Q1 Investor Presentation

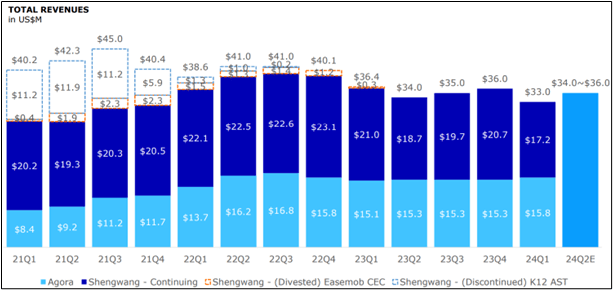

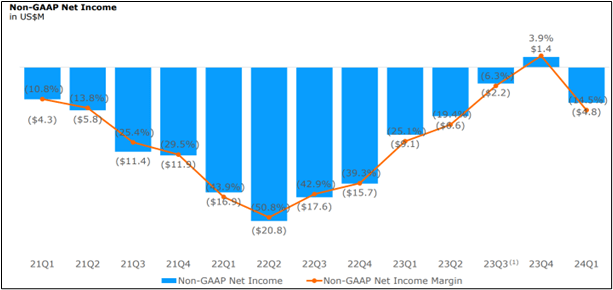

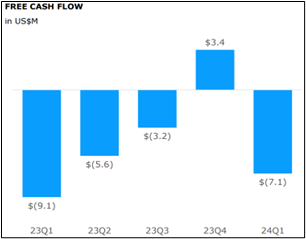

The corporate’s Q1 whole income was $33 million, down 9% versus the prior 12 months interval as proven above. Income from the Agora enterprise grew 4.6%, whereas in Shengwang income declined by 16% 12 months over 12 months. Total outcomes had been impacted by a off-season for its social and training clients however had been nonetheless inside administration’s steerage. Non-GAAP earnings and FCF improved to -$4.8 million and -$7.1 million respectively, in comparison with -$9.1 million and -$9.1 million versus Q1 2023. The margin enhancements depicted under had been achieved regardless of decrease income and weaker gross margins, pushed by expense reductions of $7 million within the quarter versus Q1 2023. The Greenback-based web retention price was 78% for Shengwang, although a lot stronger at 92% for the Agora enterprise.

Q1 Investor presentation

Administration’s steerage for Q2 of $35 million on the midpoint, signifies an expectation for strong sequential and 12 months over 12 months development pushed by sure development drivers which I’ll focus on subsequent.

Expectations going ahead

Potential development drivers

Administration expects tailwinds for the enterprise from the subsequent technology of chatbots akin to ChatGPT-4o which may purpose throughout audio, video, and textual content in actual time. Talking about this on the Q1 earnings name its CEO mentioned the chance intimately stating:

We anticipate a paradigm shift within the interplay between human and AI fashions, which is able to encourage the subsequent technology of killer apps. As this shift will result in a considerable improve within the quantity of voice and video feed transmitted globally in actual time, the significance of a low latency and extremely dependable transmission community might be larger than ever. This may put us within the distinctive place to turn into the vital infrastructure within the AI first way forward for human laptop interplay.

Administration additionally expects the Shengwang enterprise particularly to learn from the European Soccer Championship and Olympic Video games this summer season, because it has partnered with main sports activities broadcasting platforms in China. The benefits of its answer over legacy programs for broadcasting is anticipated to maintain demand excessive for the remainder of the 12 months. This was additional defined by its CEO when he mentioned:

I imagine this new expertise will set off a significant transformation in sports activities broadcasting and our highly effective, versatile and cost-effective answer will turn into broadly adopted by extra platforms to energy many different stay sports activities — stay sporting occasions all year long.

Margin enchancment

The corporate has made main strides in latest quarters to proper measurement its value construction and divest non core property. The corporate’s CFO expects the present expense run-rate to stay secure stating:

So wanting ahead this 12 months, we’re nonetheless very cautious concerning the total working surroundings. So we’ll proceed to handle our bills very fastidiously and we don’t count on Opex normally and together with R&D bills to extend sequentially from Q1 onward.

I due to this fact count on margin enhancements in upcoming quarters to be primarily pushed by income development. On condition that the corporate continues to spend greater than 40% of its income on R&D, I imagine that there’s room for administration to additional scale back bills if the anticipated income development doesn’t materialize.

Capital allocation

The corporate has deployed roughly $107.5 million in direction of share buybacks and repurchased almost 20% of the shares excellent since initiating the $200 million share repurchase program in February 2022. This system runs till February 2025 and the corporate has greater than $90 million left to deploy. I count on administration to proceed to buyback shares aggressively so long as the enterprise doesn’t drastically deteriorate and shares stay at these depressed ranges. It’s doable that the corporate initiates a particular dividend in direction of the tip of the 12 months if losses proceed to scale back.

Ideas on valuation

The corporate’s steadiness sheet consists of $381 million in money and $18 million in debt. This leads to a web money place of $363 million which corresponds to $3.94 per share, assuming 92.1 shares excellent. On the present share worth of $2.5, its market capitalization is $235 million, which is a 35% low cost to its web money. The destructive enterprise worth assigned by the market is because of the development stagnation and lack of profitability of the corporate. I nevertheless argue that the market is simply too pessimistic and that free money circulation has proven an enhancing development in latest quarters as proven under. That is primarily because of restructuring and value management measures by administration that started early final 12 months. The FCF burn during the last 4 quarters was diminished to $12.5 million and is anticipated to scale back going ahead as income development improves.

Q1 Investor Presentation

In addition to its large web money place relative to its market cap, I might additionally wish to level out that the underlying enterprise which has an annual income run-rate of above $140 million, although unprofitable, may demand a valuation of at the least $100 million. This valuation would nonetheless be at a big low cost to friends akin to Twilio (TWLO) and Sinch (OTCPK:CLCMF) that commerce at Worth to gross sales multiples of as much as 2. Due to this fact I argue that draw back is restricted on the present valuation so long as the corporate continues to scale back its quarterly money burn. If the corporate can efficiently attain FCF breakeven by the tip of subsequent 12 months, it’s going to doubtless have greater than $300 million in web money, which remains to be significantly larger than its present market cap.

Dangers

Lack of profitability

In line with me the most important danger going through buyers is that the corporate fails to ignite income development and due to this fact struggles to succeed in sustained profitability. With a purpose to mitigate this danger, administration wants to point out that they will convert among the present alternatives that had been highlighted into income for the corporate.

Publicity to China

In line with its newest Annual report, greater than half its income got here from China. This portion of income has confronted headwinds during the last two years regarding rules and a weak macroeconomy.

Competitors

Agora faces competitors from bigger world gamers akin to Twilio, Sinch and Bandwidth (BAND). It, nevertheless, has managed to distinguish itself by specializing in video associated communication whereas its rivals focus extra in direction of textual content and voice-based communication.

Conclusion

Whereas acknowledging the dangers recognized, I imagine the present valuation of the corporate displays extreme pessimism and doesn’t absolutely account for administration’s efforts for lowering bills and and enhancing margins. Though I discover the present valuation interesting, I stay cautious and keep on the sidelines till I acquire larger confidence within the firm’s path to profitability.

")

")

{kind=link}