tdub303

Thesis

U.S. Bancorp (USB) is the bank holding company and parent company of U.S. Bank. It is the fifth-largest bank in the United States by assets, with over $550 billion in assets and it is based in Minneapolis, Minnesota. Unlike its peers in the top 5 banks, USB declined significantly on Friday, being down even -10% at some point. Mind you that JPMorgan (JPM) ended the day in the green. USB has preferred shares outstanding, mostly notably the U.S. Bancorp Preferred Series A (NYSE:USB.PA):

Preferred shares, also known as preference shares or simply “prefs,” are a type of stock issued by a company that has features of both equity and debt. Unlike common shares, preferred shares generally do not carry voting rights in the company, but they do have priority over common shareholders when it comes to receiving dividends or liquidation proceeds.

USB 10K (Annual Report)

Large banking corporations that are systemically important such as U.S. Bancorp will not end up with any issues as the current regional banking crisis continues. There are ongoing discussions regarding a new SPV that would guarantee deposits outside the original $250,000 limit:

The Federal Deposit Insurance Corp. and the Federal Reserve are weighing creating a fund that would allow regulators to backstop more deposits at banks that run into trouble following Silicon Valley Bank’s collapse. Regulators discussed the new special vehicle in conversations with banking executives, according to people familiar with the matter. The hope is that setting up such a vehicle would reassure depositors and help contain any panic, said the people. They asked not to be identified because the talks weren’t public.

Single Issuer Concentration Risk

However, the question is whether an individual retail investor should take single bank risk, and at what price. Let us have a closer look at USB.PA:

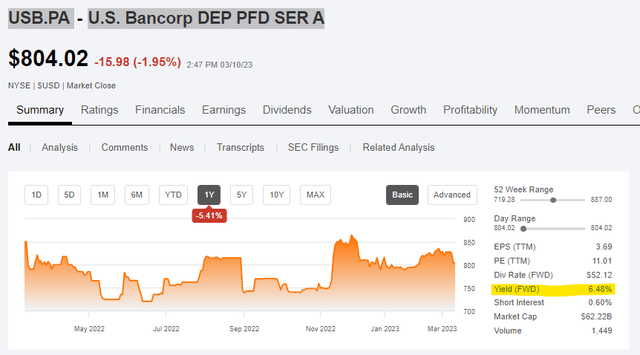

Yield (Seeking Alpha)

It is currently trading at a 6.5% yield, and it is past its call date:

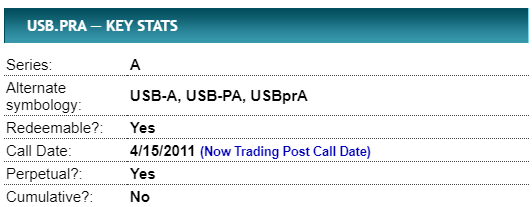

Characteristics (PreferredStockChannel)

It is a perpetual, so we will assume it will be a constant source of capital. We do not think USB will have any issues whatsoever from a default risk perspective, but the stock volatility observed in the common can percolate eventually to the preferred stock as well. And the more important question is if a 6.5% yield is sufficient of a reward for single issuer concentration. More importantly, what other alternatives does a retail investor have?

Preferred Equity ETF

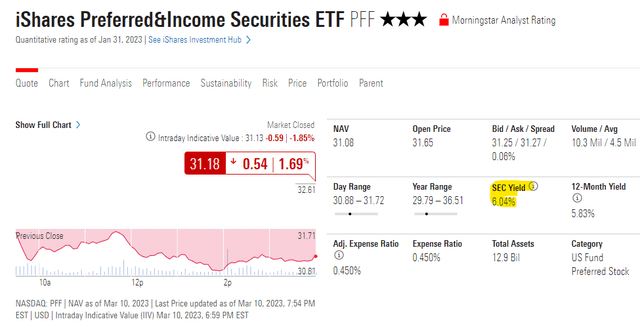

At this juncture, when it is fairly unclear how volatile certain names can be, an investor’s best bet is to look at what aggregators are yielding and benchmark individual names versus a portfolio. To that end and investor can look at the iShares Preferred and Income Securities ETF (PFF) which is an un-leveraged exchange traded fund which is overweight financials:

PFF Yield (Morningstar )

We are going to use a different article to do a deep dive into this name, but suffice to notice that PFF trades at a yield which is only 40 bps lower than USB.PA. In our mind that is too narrow. In terms of uncertainty diversity helps, and diversity is definitely priced wider than just 40 bps. In other words USB.PA is not yielding enough to justify concentration risk. I think a fair spread over a diversified name such as PFF should be around 100 bps, or a yield for USB.PA exceeding 7%.

We can see how PFF outperforms long term as well when compared to the single name:

Total Return (Seeking Alpha)

Depending on what the regulators come up with this weekend we can see volatility subside or increase. If there is no clear cut solution to the banks with high uninsured depositor bases then capital is just going to swiftly move to large, stable names, while weak credits will be aggressively pursued. USB has the potential to widen out significantly more, and if its yield exceeds by more than 100 bps the PFF yield then we would consider that an attractive entry point.

Conclusion

U.S. Bancorp is a domestic systemically important bank. The bank is the fifth largest in the U.S. and we do not believe there is credit risk associated with this institution. USB’s preferred equity Series A is currently trading with a 6.5% yield, which is just 40 bps wider than a well diversified preferred equity ETF. We do not feel a retail investor is well served by taking concentrated single issuer risk for only 40 bps over a diversified portfolio, and we believe we should see a spread in excess of 100 bps for USB.PA to start looking attractive versus the iShares Preferred and Income Securities ETF.

")

This autumn 2024 Earnings Name Transcript")

:max_bytes(150000):strip_icc()/Health-GettyImages-1370735977-146c3a69dc064dea922fe1076d88e2aa.jpg "ADHD vs. Anxiety: Similarities and Differences")

{kind=link}