Violka08

Discovering readability in complexity: Mounted revenue outlook for 2025

As 2024 closes, the fastened revenue market faces acquainted challenges: financial coverage shifts, fiscal pressures and protracted inflation considerations— complexities which have formed the panorama since 2020. Whereas the short-term backdrop might seem daunting, it doesn’t detract from Oakmark’s capability to uncover compelling alternatives for our traders. Rooted in basic worth, our investments are supposed to develop over the long run and supply steadiness in a world too usually centered on short-term good points.

Heading into 2025, fastened revenue traders appear centered on three key themes:

- Implications of rising fiscal deficits

- The Federal Reserve’s subsequent strikes

- Methods for locating worth amid complexity

Is that this the yr fiscal deficits make fastened revenue uninvestable?

The scale and scale of U.S. fiscal deficits have gotten tougher to disregard. Debt-to-GDP ratios are nearing 120%, in response to the Congressional Finances Workplace, and Treasury issuance is projected to exceed $2 trillion in 2025. This surge in provide, coupled with fears about how markets will soak up it, has fueled considerations that bonds are dropping their place as a viable funding.

Nonetheless, as we outlined in our second-quarter commentary, “Don’t allow them to scare you out of bonds,” these considerations usually overlook the market’s resilience, which is pushed by numerous structural realities.

Fiscal deficits and heavy Treasury issuance may appear intimidating, however the bond market’s historic resilience tells a extra balanced story. Demand tends to rise as worth improves— elasticity that’s evident as actual and nominal yields attain engaging ranges. Structural consumers, like pensions and insurers, proceed to offer important help, at the same time as some sovereign demand softens. With yields as soon as once more compensating traders for inflation dangers and providing long-term stability, bonds stay a cornerstone for considerate, income-focused portfolios.

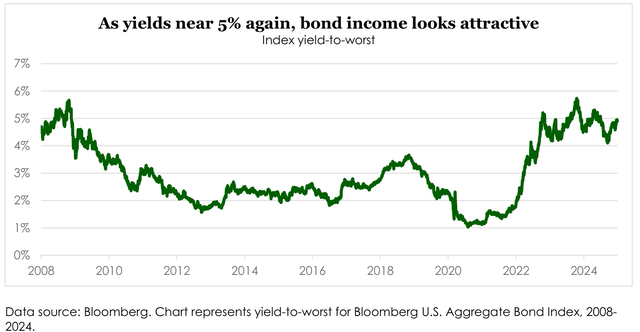

- Enticing all-in nominal and after-inflation yields: The Bloomberg U.S. Mixture Bond Index yield is as soon as once more close to 5% because of the very giant backup in charges through the fourth quarter, basically enhancing the worth proposition of fastened revenue investments.

- Elasticity of demand: A lot focus has been on the provision facet of the story that we prefer to remind people that bonds, similar to most liquid funding merchandise, have elastic demand curves. Meaning when worth goes up, demand tends to go up. Traditionally, actual yields on 10-year Treasurys (US10Y), which now exceed 2%, have made longer length belongings extra compelling, attracting each home and worldwide consumers.

- Liquidity from cash markets: The sheer scale of cash market and front-end paper— at present over $6 trillion in belongings—characterize a reservoir of demand potential that we imagine will finally circulation again into longer length securities as charge volatility stabilizes.

- Treasurys as the worldwide reserve foreign money: Treasurys stay the monetary world’s consolation meals, steadfast in demand no matter market temper swings. Though just lately there was decreased demand from a number of main sovereign governments, structural demand from pensions, insurers and the institutional cash administration enterprise continues to underpin the market.

- Historic resilience: Provide considerations will not be new. Treasury issuance exceeded $1.8 trillion in 2023, but bond markets absorbed the issuance with out long-term disruption. Traditionally, shifts in yield curves and actual charges have prompted reallocation into length, offering important help to the bond market even in periods of heavy issuance.

How will the Fed react to fiscal or geopolitical dangers that would reignite inflation?

Inflation has cooled considerably, falling from its mid-2022 peak of 9.1% to three.1%. Nonetheless, the trail to sustained worth stability shouldn’t be assured. Fiscal insurance policies aimed toward reshaping the U.S. financial system—reminiscent of reshoring initiatives, tariffs and restrictions on low-cost immigrant labor—carry long-term dangers. These insurance policies disrupt provide chains, elevate manufacturing prices and will embed structural inflationary pressures into the financial system. Geopolitical elements, reminiscent of vitality worth shocks or provide chain disruptions stemming from conflicts, additional complicate the inflation outlook.

The Fed’s problem in 2025 lies in navigating these uncertainties whereas sustaining its hard-won credibility. Fed Chair Jerome Powell and his colleagues perceive the stakes: Slicing charges too shortly may undo years of painstaking effort to revive worth stability. Regardless of benign inflation information in latest months, the Fed stays cautious and properly conscious that fiscal and geopolitical elements may reignite inflationary pressures. As I famous in a latest Making Markets podcast:

“The Fed’s credibility is its most essential asset. Transferring too shortly to chop charges, even within the face of benign inflation prints, dangers an abrupt reversal if fiscal or geopolitical elements reintroduce inflationary pressures. A return to charge hikes would destabilize markets and erode belief within the Fed’s capability to handle long-term worth stability.”

This deliberate strategy is formed by the Fed’s classes from the Nineteen Seventies and Eighties when untimely easing allowed inflation to resurge, forcing extra aggressive tightening. Powell’s Fed appears decided to keep away from repeating these errors, even when it means holding charges larger for longer. The bar for charge cuts is ready excessive. Absent a extreme recession or vital risk-off occasion, the Fed is prone to keep its present posture properly into 2025.

For fastened revenue traders, the implications are clear. A measured Fed reinforces revenue as the first driver of returns within the present atmosphere. Charge-driven capital appreciation, whereas attainable in remoted situations, will probably take a backseat to regular, dependable revenue streams. This backdrop mirrors the dynamics of 2024 when cautious financial coverage, coupled with tight monetary situations, restricted the scope for charge cuts however supplied constant alternatives for yield-seeking traders.

The Fed’s stance additionally underscores the significance of length positioning and credit score choice. Traders who align their portfolios with the Fed’s cautious trajectory are higher positioned to climate potential volatility. Longer dated Treasurys, for instance, profit from the soundness of anchored inflation expectations whereas choose credit score devices proceed to supply alternatives to seize yield with out taking up extreme danger. For traders keen to adapt to a Fed that prioritizes credibility over short-term market appeasement, the fastened revenue market in 2025 presents fertile floor for considerate, income-driven methods.

How will we make investments amid immediately’s complexity?

Volatility and noise are unavoidable, however additionally they create fertile floor for disciplined traders. Beneath are 4 noteworthy elements of the present fastened revenue backdrop.

- Acknowledge the extraordinary charge atmosphere. Over the previous three months, 10- and 30- yr U.S. Treasury yields (US30Y) have surged practically 1%, a transfer that represents virtually two commonplace deviations from historic norms. Such vital shifts are uncommon. For these assured that the Fed will meet its 2% inflation mandate throughout the subsequent three to 5 years, immediately’s market presents compelling alternatives. Actual yields now exceed 2.5% above long-term inflation expectations, offering a sexy basis for income- centered portfolios—with out requiring publicity to credit score danger.

- Draw on the benefits of lively administration. Credit score spreads close to historic lows depart little room for error in evaluating default dangers. Success hinges much less on aggressively pursuing high-yielding alternatives and extra on avoiding poor risk-reward dynamics. Managers with the pliability to bypass overpriced segments of the market—reminiscent of particular areas of company credit score or leveraged loans—are higher positioned to ship sustainable returns. On this context, avoiding losses whereas incomes a constant 5%+ revenue stream creates a compounding benefit that passive methods usually fail to attain.

- Search for alternatives in key asset lessons. Leveraged loans, with their floating-rate buildings, supply safety in opposition to additional charge volatility whereas offering engaging yields that compensate for inherent dangers. Equally, company mortgage-backed securities current vital worth. Spreads relative to company credit score stay traditionally large, and as charge volatility stabilizes, the convexity challenges which have weighed on MBS are prone to ease, making these devices significantly interesting to income-focused traders. Excessive-quality credit score devices, which supply predictable money flows and strong enterprise worth protection, additionally stand out. These belongings emphasize the significance of disciplined credit score choice to keep away from overvalued names whereas specializing in resilience and sturdiness in risky markets.

- Give attention to particular person credit score tales. Persistently outperforming in fastened revenue doesn’t require macroeconomic predictions or makes an attempt to time sector developments. As an alternative, it’s about figuring out alternatives the place markets misprice credit score relative to its default dangers. This strategy emphasizes deep, bottom-up analysis to uncover companies with robust capital allocation, firms enduring non permanent challenges however sustaining operational power, or onerous belongings undervalued in present market situations. By concentrating on fundamentals, we cut back reliance on unpredictable macroeconomic outcomes and improve potential returns.

The highway forward

The fastened revenue market in 2025 stays sophisticated, however not uninvestable. Issues in regards to the deficit, charge volatility and different financial elements are counterbalanced by what we really feel is a rising worth case for fastened revenue belongings as actual yields climb.

We see alternatives for these keen to dig deeper. Leveraged loans stand out for his or her compelling yields, and MBS company paper presents compelling relative worth for long-term traders, particularly in comparison with company benchmark paper and U.S. Treasurys. Throughout the board, we advocate specializing in high-quality issuers that proceed to offer sturdy money flows and resilience in opposition to potential market shocks—an antidote to the temptation of chasing yield at any worth when index credit score unfold ranges are nonetheless close to historic lows.

At Oakmark, we don’t view complexity as a barrier; it’s a characteristic of markets that rewards considerate, lively administration. The guiding rules mentioned right here—specializing in long-term worth, avoiding pointless dangers and embracing the self-discipline of particular person credit score evaluation— stay as related as ever in navigating the challenges of immediately’s bond market.

Completely satisfied New Yr to you and your households! Right here’s to a different yr of considerate investing and uncovering worth.

Adam D. Abbas

Portfolio Supervisor

|

The knowledge, information, analyses, and opinions introduced herein (together with present funding themes, the portfolio managers’ analysis and funding course of, and portfolio traits) are for informational functions solely and characterize the investments and views of the portfolio managers and Harris Associates L.P. as of the date written and are topic to vary and should change primarily based on market and different situations and with out discover. This content material shouldn’t be a suggestion of or a proposal to purchase or promote a safety and isn’t warranted to be appropriate, full or correct. Sure feedback herein are primarily based on present expectations and are thought-about “forward-looking statements.” These forward-looking statements replicate assumptions and analyses made by the portfolio managers and Harris Associates L.P. primarily based on their expertise and notion of historic developments, present situations, anticipated future developments, and different elements they imagine are related. Precise future outcomes are topic to numerous funding and different dangers and should show to be totally different from expectations. Readers are cautioned to not place undue reliance on the forward-looking statements. This materials shouldn’t be supposed to be a suggestion or funding recommendation, doesn’t represent a solicitation to purchase, promote or maintain a safety or an funding technique, and isn’t supplied in a fiduciary capability. The knowledge supplied doesn’t consider the particular aims or circumstances of any explicit investor, or counsel any particular plan of action. Funding selections must be made primarily based on an investor’s aims and circumstances and in session together with his or her monetary professionals. Yield is the annual charge of return of an funding paid in dividends or curiosity, expressed as a proportion. A snapshot of a fund’s curiosity and dividend revenue, yield is expressed as a proportion of a fund’s web asset worth, is predicated on revenue earned over a sure time interval and is annualized, or projected, for the approaching yr. The Bloomberg U.S. Mixture Bond Index is a broad-based benchmark that measures the funding grade, U.S. dollar-denominated, fixed-rate taxable bond market. The index consists of Treasurys, government- associated and company securities, mortgage-backed securities (company fixed-rate and hybrid ARM pass- throughs), asset-backed securities and business mortgage-backed securities (company and non- company). This index is unmanaged and traders can not make investments instantly on this index. The Oakmark Bond Fund invests primarily in a diversified portfolio of bonds and different fixed-income securities. These embody, however will not be restricted to, funding grade company bonds; U.S. or non-U.S.- authorities and government-related obligations (reminiscent of, U.S. Treasury securities); under investment- grade company bonds; company mortgage backed-securities; business mortgage- and asset-backed securities; senior loans (reminiscent of, leveraged loans, financial institution loans, covenant lite loans, and/or floating charge loans); assignments; restricted securities (e.g., Rule 144A securities); and different fastened and floating charge devices. The Fund might make investments as much as 20% of its belongings in fairness securities, reminiscent of widespread shares and most well-liked shares. The Fund may maintain money or short-term debt securities every so often and for non permanent defensive functions. Below regular market situations, the Fund invests not less than 25% of its belongings in investment-grade fixed- revenue securities and should make investments as much as 35% of its belongings in under investment-grade fixed-income securities (generally referred to as “high-yield” or “junk bonds”). Mounted revenue dangers embody interest-rate and credit score danger. Sometimes, when rates of interest rise, there’s a corresponding decline in bond values. Credit score danger refers back to the chance that the bond issuer won’t be able to make principal and curiosity funds. Bond values fluctuate in worth so the worth of your funding can go down relying on market situations. All info supplied is as of 12/31/2024 except in any other case specified. Earlier than investing in any Oakmark Fund, you need to rigorously contemplate the Fund’s funding aims, dangers, administration charges and different bills. This and different essential info is contained in a Fund’s prospectus and abstract prospectus. Please learn the prospectus and abstract prospectus rigorously earlier than investing. For extra info, please go to Oakmark.com or name 1-800-OAKMARK (1-800-625-6275). Natixis Distribution, LLC (Member FINRA | SIPC), a restricted objective broker-dealer and the distributor of varied registered funding firms for which advisory providers are supplied by associates of Natixis Funding Managers, is a advertising agent for the Oakmark Funds. Harris Associates Securities L.P., Distributor, Member FINRA. Date of first use: 01/08/2025 QCM-4132ADA-04/25 OPINION PIECE. PLEASE SEE ENDNOTES FOR IMPORTANT DISCLOSURES. Harris Associates | 111 South Wacker Drive, Suite 4600 | Chicago, IL 60606 | 312.646.3600 |

Authentic Publish

Editor’s Be aware: The abstract bullets for this text had been chosen by Searching for Alpha editors.

")

")

")

{kind=link}