PeopleImages

VZ inventory: earlier thesis and new growth

I final analyzed Verizon inventory (NYSE:VZ) greater than a month in the past. As you possibly can see from the screenshot beneath, that article was revealed on July 26, 2024, and was titled “Verizon Q2: Nonetheless Not Too Late To Promote (Technical Evaluation)”. Because the title suggests, the article really helpful promoting at the moment. The advice is principally primarily based on the near-term prospects and technical buying and selling patterns of the inventory costs surrounding its Q2 earnings report. Quote:

VZ inventory’s Q2 earnings report supplies one other instance of development challenges. Mixed with the promoting strain afterward, I see giant odds for VZ costs to fall beneath a key assist degree of $38.5 within the subsequent 6–12 months. Buyers with a brief timeframe ought to thus contemplate promoting. There are different various concepts (comparable to MO and EPD) that supply related value-yield combos however far larger development potential and constructive market momentum.

The purpose of this follow-up article is to improve my ranking to HOLD. The improve is predicated on two issues: volatility and new developments in its enterprise fundamentals. The inventory has certainly suffered sizable volatilities as you possibly can see from the subsequent chart beneath shortly after its Q2 ER in late July. With the earnings season over, I anticipate quieter volatility forward.

Searching for Alpha

On the enterprise entrance, a key growth since my final writing was the announcement the corporate has made to amass Frontier Communications (NASDAQ:FYBR). On Sept 5, VZ introduced a $20B money deal to amass FYBR and acknowledged that:

This strategic acquisition of the most important pure-play fiber web supplier within the U.S. will considerably broaden Verizon’s fiber footprint throughout the nation, accelerating the corporate’s supply of premium mobility and broadband companies to present and new prospects.

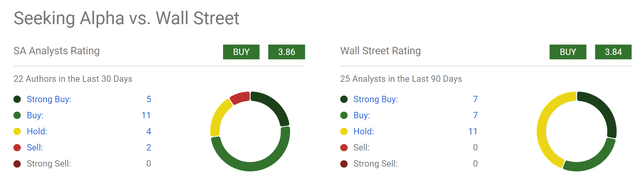

The corporate is optimistic concerning the synergist alternatives. And each Searching for Alpha and Wall Road analysts are bullish on the inventory, as you possibly can see from their latest rankings beneath. Nonetheless, my view is that such a bullish ranking very doubtless displays an overestimation of the potential impacts from this acquisition, as detailed subsequent.

Searching for Alpha

VZ inventory: Frontier’s potential impression

Earlier than transferring on, let me first make clear that I’m not denying the accretive nature of the acquisition. I actually see many synergistic alternatives because the bulls see. It’s simply that I feel the potential impacts are that substantial. For example,

VZ expects to appreciate not less than $500M in run-rate price synergies by yr three from the advantages of elevated scale and distribution and community integration. The deal integrates Frontier’s superior fiber community, which encompasses 2.2M subscribers throughout 25 states, into Verizon’s portfolio of fiber and wi-fi property, together with its best-in-class Fios providing.

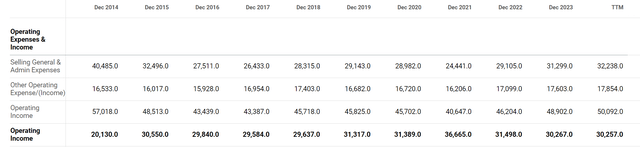

To contextualize the above price synergies, the chart beneath supplies a breakdown of Verizon’s working bills over the latest few years. Particularly, it exhibits the corporate’s SG&A (promoting, normal, and administrative bills) along with different working bills. As proven within the chart, VZ’s working bills have typically elevated through the years. On a TTM foundation, its SG&A bills reached $32.2B and different bills $17.8B within the newest quarter.

Searching for Alpha

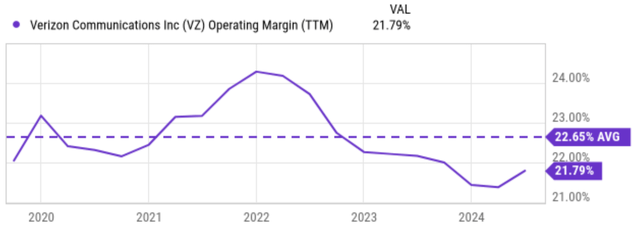

With these bills and its present income (of round $134.2B on a TTM foundation), its working margin labored out to be barely beneath 22% as you possibly can see from the subsequent chart beneath. Reaching a synergistic advantage of $500M (that’s, if the advantages truly materialize as administration predicts) would assist to scale back its working bills by about 1% in my estimate. VZ has been going through margin strain since 2022 as seen resulting from a wide range of headwinds (together with adjustments in borrowing charges, price administration methods, aggressive pressures, heavy CAPEX necessities, and so on.). And its present margin has fallen beneath the 5-year common of twenty-two.65% by a noticeable hole as seen. Even with the synergist advantages totally factored in, its margin can be nonetheless decrease than the long-term common, in line with my estimate.

Searching for Alpha

Different dangers and last ideas

Moreover the restricted impression, there are a number of different draw back dangers surrounding the deal. The deal interprets into an acquisition value of $38.5 a share in money, representing a premium of near 44% to FYBR’s common share value earlier than the deal’s announcement. To me, such a large premium very doubtless implies that VZ is overpaying, and the overpayment may offset among the anticipated accretive advantages. It is usually unsure if the deal could be accepted, as there are antitrust and different dangers related to a large acquisition like this.

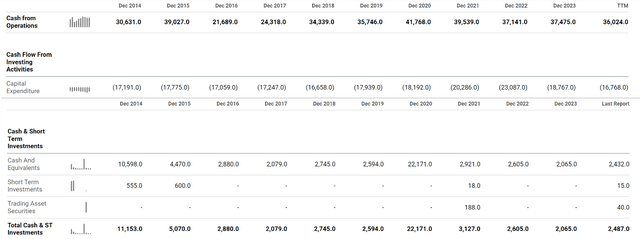

On the constructive facet, VZ generates a major amount of money move from its core enterprise actions and maintains a wholesome steadiness sheet to finance the deal. To wit, as of TTM, VZ generated $36,420 million in money from operations as seen from the subsequent chart beneath. Nonetheless, there have been fluctuations on this metric, with some years exhibiting larger ranges of money era than others. As famous earlier, VZ has invested closely in capital expenditure through the years. Nonetheless, I anticipate its CAPEX to have peaked already. As of TTM, its CAPEX sits at $16,768 million as seen, in comparison with over $20B in 2021 and 2022. Because of this, VZ generated about $20B of free money move as of TTM, virtually the precise quantity wanted for its Frontier deal. Along with the strong money move, VZ additionally maintains a wholesome money place. As seen within the chart, as of the newest reported interval, VZ has over $2.4 billion in money and short-term investments on its ledger.

Searching for Alpha

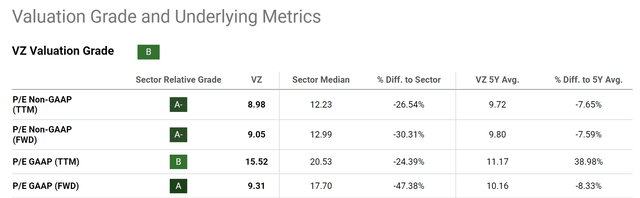

On the similar time, the corporate is buying and selling at a really affordable valuation, each in absolute and relative phrases. Extra particularly, the chart beneath summarizes VZ inventory’s valuation grade. As seen, VZ’s P/E ratios, each in TTM and FWD phrases, are decrease than the sector median and its personal 5-year common. For example, VZ’s TTM non-GAAP P/E ratio is 8.98 solely. In comparison with the sector median of 12.23, this represents a 26.54% low cost. In comparison with its 5-year common of 9.72, this represents a milder low cost of about 7%. Its FWD non-GAAP P/E ratio is 9.05 and exhibits an identical pattern when in comparison with the sector median of 12.99 and its 5-year common of 9.80.

All instructed, within the mid to long run, I don’t see something clearly towards holding on to a pacesetter in a secure sector at a ~9x P/E a number of. Its 6.4% dividend yield provides additional draw and draw back safety. Nonetheless, I don’t anticipate an alpha from VZ when in comparison with different dividend shares (comparable to Altria and/or Enterprise Merchandise, as talked about in my final article). I anticipate the whole return potential to be uninspiring underneath present situations with a good valuation a number of, restricted margin enlargement potential, and restricted EPS development potential. I don’t anticipate the Frontier acquisition to essentially change these limitations.

Searching for Alpha

This autumn 2024 Earnings Name Transcript")

")

")

— RT World News")

/cdn.vox-cdn.com/uploads/chorus_asset/file/25628673/Screenshot_2024_09_18_at_4.46.56_PM.jpeg "Google Workspace users will see their Calendars front and center in Chrome")

{kind=link}