Pension funds’ annualized mixture returns since 2000 have been just about equivalent to a easy 60-40 index portfolio.

That feels considerably anticipated it appears, however what in regards to the true crème de la crème, the highest establishments. Certainly they may beat a easy purchase and maintain allocation?

Seems, they actually can’t. Beneath we recall an article we penned a couple of years in the past, “Ought to CalPERS Hearth Everybody and Purchase Some ETFs?”

“He was a U.S.-class easy politician, which is the one approach you’re going to outlive in that job. It has nothing to do with investing.”

That’s how Institutional Investor just lately described a former CIO of the California Public Staff’ Retirement System, also called CalPERS.

The outline is particularly attention-grabbing when contemplating that the “I” in “CIO” stands for “funding,” which raises an eyebrow at how the function may have “nothing to do with investing”.

For readers much less aware of CalPERS, it manages pension and well being advantages for over a million public workers, retirees, and their households. They oversee the most important pension fund within the nation, valued at over $450 billion.

With that huge quantity of belongings comes an excessive amount of scrutiny over how these belongings are deployed. The CIO function managing this pension is among the most prestigious and highly effective within the nation, therefore Institutional Investor’s curiosity. Apparently, it’s additionally one of many hardest roles to carry down. The place has averaged a brand new CIO roughly each different 12 months for the previous decade.

Now, this text isn’t going to spend an excessive amount of time on CalPERS governance, as many others have spilled an excessive amount of ink there. Plus, the drama surrounding the pension is unending and can seemingly function a brand new twist by the point we publish our article. (To be truthful, Harvard’s endowment points are practically equally as dramatic…)

As a substitute, we’re going to make use of CalPERS’ funding method as a jumping-off level for a broader dialogue about portfolio allocation, returns, charges, and wasted effort. And if we do our job accurately, we hope you’ll really feel only a bit much less stress about your personal portfolio positioning by the point we’re finished.

The staggering waste of CalPERS market method

CalPERS’ acknowledged mission is to “Ship retirement and well being care advantages to members and their beneficiaries.”

Nowhere on this mission does it state the objective is to put money into a great deal of non-public funds and pay the inflated salaries of numerous non-public fairness and hedge fund managers. However that’s precisely what CalPERS’ does.

The pension’s Funding Coverage doc – and we’re not making this up – is 118 pages lengthy.

Their record of investments and funds runs 286 pages lengthy. (Possibly they should learn the ebook “The Index Card”.)

Their construction is so difficult that for a very long time, CalPERS couldn’t even calculate the charges it pays on its non-public investments. On that notice, by far the largest contributor to excessive charges is CalPERS’ non-public fairness allocation, which they plan on rising the allocation to. Is {that a} nicely thought out thought or is it a Hail Mary go after years of underperformance? In keeping with a latest CalPERs enterprise capital portfolio returned 0.49% from 2000 to 2020.

Now, it’s straightforward to criticize. However is there a greater approach?

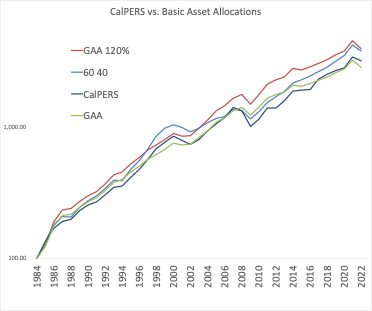

Let’s study CalPERS’ historic returns towards some primary asset allocation methods.

We’ll start with CalPERS’ present portfolio allocation:

Supply: CalPERS

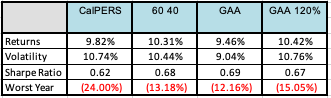

Now, that we all know what CalPERS is working with, let’s examine its returns towards three primary portfolios starting in 1985.

- The basic 60/40 US shares and bonds benchmark.

- A worldwide asset allocation (GAA) portfolio from our ebook International Asset Allocation (accessible as a free eBook right here). The allocation approximates the allocation of the worldwide market portfolio of all the general public belongings on the planet.

- A GAA portfolio with slight leverage, since most of the funds and techniques that CalPERS makes use of have embedded leverage.

Supply: CalPERS, International Monetary Information, Cambria

As you possibly can see from the desk, from 1985-2022 CalPERS fails to distinguish itself from our easy “do nothing” benchmarks.

To be clearer the returns will not be dangerous. They’re simply not good.

Contemplate the implications:

All of the money and time spent by funding committees debating the allocation…

All of the money and time spent on sourcing and allocating to non-public funds…

All of the money and time spent on consultants…

All of the money and time spent on hiring new workers and CIOs…

All of the money and time spent on placing collectively limitless reviews to trace the 1000’s of investments…

All of it – completely wasted.

CalPERS would have been higher off simply firing their entire employees and shopping for some ETFs. Ought to they name Steve Edmundson? It could definitely make the report holding loads simpler!

Plus, they’d save a whole lot of hundreds of thousands a 12 months on working prices and exterior fund charges. Cumulatively over time, the prices run nicely into the billions.

Personally, I take the “I” a part of the acronym very critically and have provided to handle the CalPERS pension without spending a dime.

“Hey pension funds battling underperformance and main prices and headcount. I’ll handle your portfolio without spending a dime. Purchase some ETFs. Rebal yearly or so. Have an annual shareholder assembly over some pale ales. Possibly write a 12 months in overview.”

I’ve utilized for the CIO function 3 times, however every time CalPERS has declined an interview.

Possibly CalPERS ought to replace its mission assertion to “Ship retirement and well being care advantages to members CalPERS workers, non-public fund managers and their beneficiaries.”

On this occasion, they’d be succeeding mightily.

Is it simply CalPERS, or is it the business?

One may have a look at the outcomes above and conclude CalPERS is an outlier.

Critics may push again, saying, “OK Meb, we get that CalPERS can’t beat a primary purchase and maintain, however let’s be sincere – it’s the GOVERNMENT! We outline our authorities by mediocrity. Any severe non-public pension or establishment ought to be utilizing the good cash, the massive hedge fund managers.”

Truthful level. So, let’s broaden our evaluation.

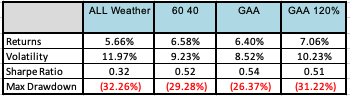

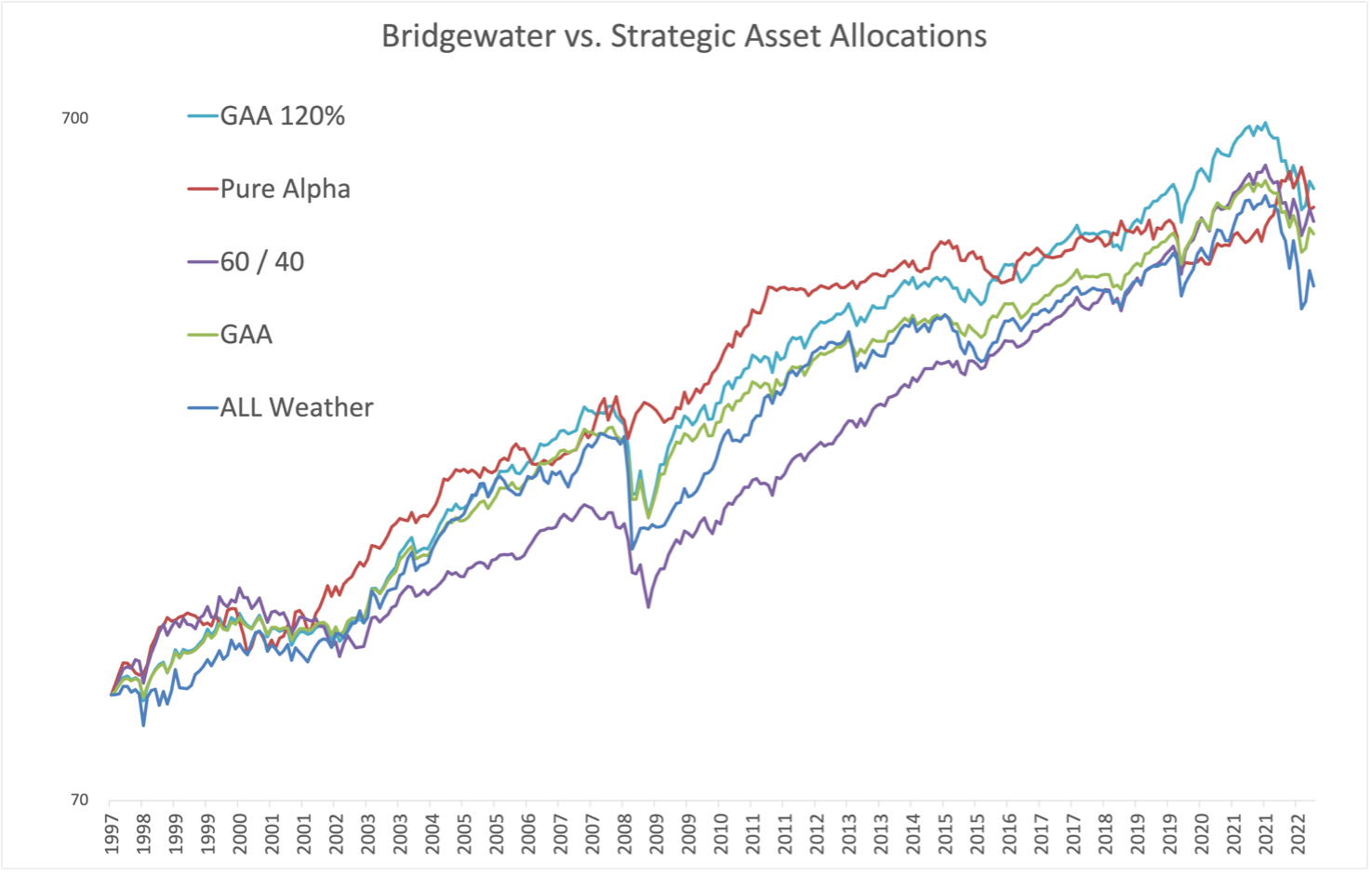

We’ll accomplish that by inspecting the most important and most well-known hedge fund supervisor, Bridgewater. This $100 billion+ cash supervisor presents two predominant portfolios, a purchase and maintain “All Climate” technique and a “Pure Alpha” technique.

In 2014, we got down to clone Bridgewater’s All Climate” portfolio – an allocation that Bridgewater says has been stress-tested by two recessions, an actual property bubble, and a worldwide monetary disaster.

The clone, based mostly on a easy world market portfolio comprised of indexes, did a great job of replicating Bridgewater’s providing when again examined. Extra importantly, working the clone would have required zero hedge fund administration prices and lockups, and wouldn’t have been weighed down by any tax inefficiency. To be truthful, this backrest has the good thing about hindsight and pays no charges or transaction prices.

The All Climate portfolio, with its give attention to danger parity, reveals that when you’re constructing a portfolio you don’t essentially have to just accept pre-packaged asset courses.

For instance, in terms of equities, they’re inherently leveraged, and most corporations have debt on their steadiness sheet. So, there’s no cause nor obligation to take shares at their notional worth. One option to “deleverage shares” could be to speculate half in equities and half in money. And the identical goes for bonds, you possibly can leverage them up or all the way down to make them roughly unstable.

This method has been round for a very long time, nicely over sixty years. Relationship again to the times of Markowitz, Tobin, and Sharpe, the idea is actually a brilliant diversified buy-and-hold and rebalanced portfolio – one which Bridgewater’s founder Ray Dalio says he would put money into if he handed away and wanted a easy allocation for his kids.

So clearly the world’s largest hedge fund ought to be capable of stomp an allocation one may write on an index card?

As soon as once more, from 1998-2022 we discover {that a} primary 60/40 or world market portfolio does a greater job than the most important hedge fund complicated on the planet.

Supply: Morningstar, International Monetary Information, Cambria

One might reply, “OK Meb, All Climate is meant to be a purchase and maintain portfolio. They cost low charges. You need the great things, the actively managed Pure Alpha!”

What about Bridgewater’s actively managed portfolio?

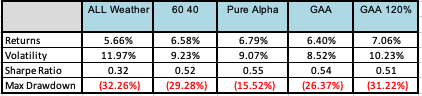

Dalio separated the All Climate portfolio from Bridgewater’s Pure Alpha technique, which is supposed to be its multi-strategy, go wherever portfolio.

His thought was to separate “beta,” or market efficiency from “alpha,” or added efficiency on high of common market returns. He believes beta is one thing that you need to pay little or no for (we’ve gone on the report in saying you need to pay nothing for it).

Let’s now deliver the Pure Alpha technique into the combo. Beneath, we’ll examine it with All Climate, the standard 60/40 portfolio, and the International Asset Allocation (GAA) portfolio from our ebook and above. Lastly, the chance parity technique makes use of some leverage, so we additionally did a check with GAA and leverage of 20%.

The replication technique again examined the portfolios’ respective performances between 1998 and 2022.

Supply: Morningstar, International Monetary Information, Cambria

As soon as once more the returns of Pure Alpha had been practically equivalent to the GAA and 60/40 portfolios, with efficiency differing by lower than 0.5%. And don’t miss that Pure Alpha really trailed the leveraged model of the GAA portfolio.

Once more, this isn’t dangerous, it’s simply not good.

Some might say, “however Dalio and the corporate did this within the Nineteen Nineties in actual time with actual cash.”

We completely tip our hat to that argument, and moreover, the Pure Alpha appears prefer it takes a special return path than the opposite allocations, seemingly providing some diversification profit from the non-correlation to conventional belongings. We additionally acknowledge that the benchmarks embrace a very sturdy trailing run for US shares.

Right here’s the issue. Many of those hedge fund and personal fairness methods price the top investor 2 and 20, or 2% administration charges and 20% of efficiency. In order that 10% annual gross efficiency will get knocked down to six% in spite of everything of these charges.

So sure, maybe Bridgewater and different funds do generate some alpha, the issue is that they maintain all of it for themselves.

Regardless, it’s good to see that you may replicate an incredible quantity of their technique simply by shopping for the worldwide market portfolio with ETFs and rebalancing it yearly whereas avoiding big administration charges, paying further taxes, or requiring huge minimal buy-ins.

The relevance to your portfolio

Let’s take this away from the educational and make it related to your cash and portfolio.

As you sift by year-end articles proclaiming how you can place your portfolio for a monster 2024, or extra seemingly given a pundit’s choice for gloom and doom, information an impending large recession and crash coming… as you stress about how a lot cash to place into gold, or oil, or rising markets… as you lose sleep wrestling with whether or not U.S .shares are too costly… take into account a extra essential query…

“Does it even matter?”

If the largest pension fund and the largest hedge fund can’t outperform primary purchase and maintain asset allocations, what likelihood do you may have?

To all of the pension funds and endowments on the market, the supply stands – we’re completely happy to design a strategic asset allocation without spending a dime. We’ll prevent the $1 million in base and bonus for the CalPERS CIO function. All that we ask is that simply possibly, we meet yearly, rebalance, and share some drinks.

Q3 2026 Earnings Call Transcript")

")

")

")

{kind=link}