Olivier Le Moal

Given the upper rate of interest dynamics, it’s lastly doable for buyers to plan actually yield-seeking methods with out taking extreme threat or receiving insignificant present revenue streams.

The uptick in low cost charges (i.e., rates of interest) has pushed down the multiples throughout the board, rendering the yield ranges extra attractive. These extra aggressive low cost charges have impacted each risk-heavy and defensive belongings (or corporations). In different phrases, there are actually prospects to enter into corporations which have strong capital buildings and rising money flows, however elevated dividend yield merely resulting from the next low cost price.

Whereas it’s true that the general yield ranges have gone up, buyers should nonetheless make a selection whether or not to focus extra on maximizing the yield potential or sacrifice some foundation factors in present revenue streams with a view to entry dividend progress potential.

As lots of my followers / readers have in all probability observed, I’m an enormous fan of excessive yielding securities and don’t care a lot in regards to the dividend progress part so long as the underlying dividends are actually underpinned by sturdy money flows. With that being mentioned, there’s a advantage of getting some diversification in place (asset, sector in addition to technique clever).

On this context, I wish to spotlight two particular devices by way of which excessive yield in search of buyers can seize totally different threat and return dynamics that might not be doable through pure-play excessive yielding exposures. In a nutshell, there are three main benefits:

- Investing in a bit decrease yielding securities creates a chance to learn from a dividend progress that has the potential to over time end in a a lot greater present revenue era relative to excessive yielding options.

- Usually, dividend progress implies an publicity in direction of growth-tilted financial sectors, which, in flip, must also reward buyers by way of a value appreciation on high of attractive dividend progress.

- Importantly, because the rates of interest are up, it’s doable to scope progress investments that provide comparatively attention-grabbing yields already from the beginning.

Listed here are two particular names that meet the aforementioned standards.

Decide #1: The Schwab U.S. Dividend Fairness ETF (SCHD)

SCHD is without doubt one of the hottest dividend progress ETF with AuM of circa $55 billion. The underlying asset choice course of is as follows:

- An organization has to have at the least 10 consecutive years of dividends

- Market cap degree must be minimal $500 million.

- After the pattern is developed primarily based on the 2 standards above, SCHD selects corporations that maximize the next elements: money circulation yield, return on fairness, dividend yield and 5-year dividend progress.

So, at its core, SCHD is targeted on well-established companies that possess comparatively low monetary threat and have ample dividend progress potential.

The plain motive why SCHD might be deemed enticing is the mix of defensive publicity with a transparent dividend progress potential.

Apart from this, there are two further the explanation why dividend buyers ought to think about including SCHD to their portfolios:

- The FWD dividend yield of SCHD has reached 4.2%, which is materially above its 10-year historic common of ~ 3%. Such a yield must be enough sufficient for dividend buyers to deploy their capital right here with out incurring an excessive amount of of a chance value by way of the foregone revenue degree. Plus, towards the backdrop of SCHD’s historic double-digit dividend progress at the side of robust revenue progress momentum, the general case for SCHD as a yield-focused play seems very enticing.

- The present FOMC dot plot, which signifies a declining trajectory sooner or later rates of interest introduces favorable dynamics for SCHD’s underlying investments. As many of the corporations that share a constituency in SCHD’s asset base are growth-tilted, the results from the rate of interest adjustments must be somewhat important. This is because of a magnified length issue that’s attribute of corporations which exhibit back-end loaded money flows (i.e., resulting from progress potential, the money flows sooner or later exceed those that are generated within the current).

Decide #2: NEOS NASDAQ-100 Excessive Revenue ETF (QQQI)

QQQI is a comparatively new ETF that was established in January this 12 months. It’s an actively managed car implementing a dynamic possibility technique with a objective to generate excessive streams of present revenue. On this course of, QQQI applies totally different possibility methods, however the important thing one – which can also be how the yield enhancement can happen – is a coated name technique. Right here, the choices are bought towards the Nasdaq 100.

Resulting from this feature technique, QQQI yields roughly 14% on a FWD annualized foundation. Nevertheless, as it’s the case with the entire option-based ETFs that devise particular methods to maximise yield, the upside potential is per definition restricted. It’s certainly the case with QQQI additionally.

With that being mentioned, we now have to remember the fact that QQQI makes use of a dynamic possibility technique, beneath which the administration has some discretion by way of deciding when to depart some room open for potential value appreciation within the underlying securities.

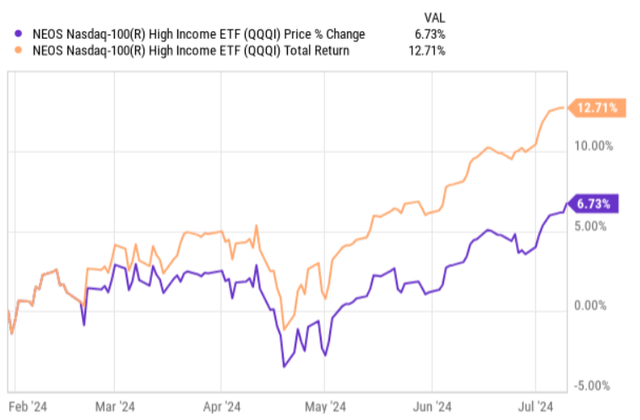

Wanting on the chart beneath, we will properly see how QQQI value has ticked greater regardless of its large distribution yield.

YCharts

So, by investing in QQQI, dividend buyers cannot solely profit from a transparent yield enhancement stemming from the present double-digit yield, but in addition introduce a component of value appreciation potential of their portfolios, which is underpinned by the Nasdaq 100 names.

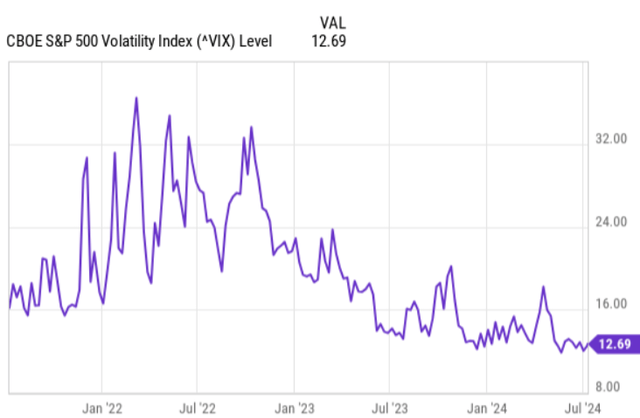

Lastly, it’s value underscoring the prevailing VIX ranges which can be at historic lows. For an ETF like QQQI this imposes headwinds for pocketing wealthy premiums from the bought choices.

YCharts

Whereas it’s tough (or virtually unattainable) to foretell when the VIX will shoot greater, it could be truthful to imagine that simply primarily based on the historic knowledge, the percentages are greater for experiencing some upward swing from right here.

The underside line

Though on this explicit atmosphere, dividend buyers have wider choices to choose corporations which generate first rate yield with restricted threat, there’s nonetheless a rationale behind diversifying into extra progress targeted devices.

For the reason that rates of interest are excessive, investing in progress tilted devices doesn’t essentially have to come back with big sacrifices on the yield.

For instance, SCHD is a ~4% yielding ETF with historic dividend progress within the double-digit territory and has a big dividend progress potential forward. Equally, QQQI is an instance of how some progress might be accessed, whereas nonetheless benefiting from very enticing present revenue streams.

")

")

Presents at H.C. Wainwright 27th")

")

{kind=link}