Printed on July 14th, 2025 by Bob Ciura

The S&P 500 has been traditionally overvalued (in hindsight) continuous since 2010 utilizing the Shiller P/E ratio.

The Shiller P/E ratio makes use of a median of 10 years of earnings for the “E” (earnings) within the P/E ratio to clean out outcomes and make the metric related when earnings short-term flip detrimental, throughout recessions.

The historic common Shiller P/E ratio is 17.3. It’s presently at 38.1. Subsequently, the S&P 500 is 121% overvalued in accordance with the Shiller P/E ratio.

The massive takeaway from that is that the market is buying and selling at a really excessive valuation a number of in the present day, relative to its historical past.

When the market is overvalued, buyers ought to look to dividend shares to scale back portfolio volatility, and for dividend revenue which supplies a buffer in opposition to falling inventory costs.

For instance, the free excessive dividend shares listing spreadsheet under has our full listing of particular person securities (shares, REITs, MLPs, and so forth.) with with 5%+ dividend yields.

Shopping for overvalued dividend shares can jeopardize future returns. Even high quality corporations can quantity to mediocre or poor investments, if too excessive worth is paid.

Falling valuations can result in low (and even detrimental) complete returns, even together with dividends.

Subsequently, buyers must be cautious in relation to overvalued dividend shares. The next 10 overvalued dividend shares must be averted.

The listing is sorted by the extent of overvaluation.

Desk of Contents

Overvalued Dividend Inventory #10: Kulicke & Soffa Industries (KLIC)

- Annual Valuation Return: -14.0%

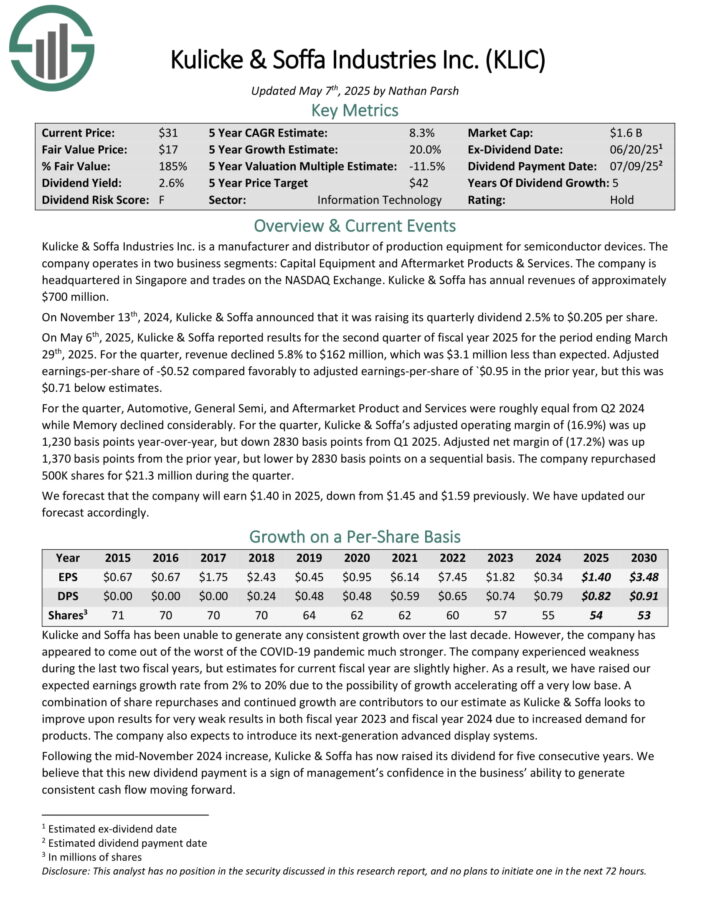

Kulicke & Soffa Industries Inc. is a producer and distributor of manufacturing tools for semiconductor units. The corporate operates in two enterprise segments: Capital Gear and Aftermarket Merchandise & Providers.

It’s headquartered in Singapore and trades on the NASDAQ Trade. Kulicke & Soffa has annual revenues of roughly $700 million.

On Might sixth, 2025, Kulicke & Soffa reported outcomes for the second quarter of fiscal yr 2025. For the quarter, income declined 5.8% to $162 million, which was $3.1 million lower than anticipated.

Adjusted earnings-per-share of -$0.52 in contrast favorably to adjusted earnings-per-share of -$0.95 within the prior yr.

For the quarter, Automotive, Normal Semi, and Aftermarket Product and Providers have been roughly equal from Q2 2024 whereas Reminiscence declined significantly.

For the quarter, Kulicke & Soffa’s adjusted working margin of (16.9%) was up 1,230 foundation factors year-over-year, however down 2830 foundation factors from Q1 2025.

Click on right here to obtain our most up-to-date Certain Evaluation report on KLIC (preview of web page 1 of three proven under):

Overvalued Dividend Inventory #9: Fortitude Gold (FTCO)

- Annual Valuation Return: -14.3%

Fortitude Gold Company was spun-off from Gold Useful resource Company right into a separate public firm in December 2021. Fortitude Gold is a junior gold producer with operations in Nevada, U.S.A, one of many world’s premier mining pleasant jurisdictions.

The corporate targets high-grade gold open pit heap leach operations averaging one gram per tonne of gold or higher. Its property portfolio presently consists of 100% possession in seven high-grade gold properties.

All seven properties are inside an approximate 30-mile radius of each other inside the prolific Walker Lane Mineral Belt. The corporate generated $37.3 million in revenues final yr, nearly all of which have been from gold, and relies in Colorado Springs, Colorado.

On April twenty ninth, 2025, Fortitude Gold launched its first-quarter 2025 outcomes for the interval ending March thirty first, 2025. For the quarter, revenues got here in at $6.5 million, marking a 20% decline in comparison with Q1 2024.

The lower in income was largely on account of a 41% drop in gold gross sales quantity and a 26% lower in silver gross sales quantity. These declines have been partially offset by a 38% enhance in gold costs and a 38% enhance in silver costs.

Shifting to the underside line, Fortitude reported a mine gross revenue of $3.3 million in comparison with $4.2 million the earlier yr, reflecting the decrease internet gross sales.

The corporate additionally introduced a discount in its month-to-month dividend from $0.04 to $0.01 per share, efficient with the Might 2025 fee.

Click on right here to obtain our most up-to-date Certain Evaluation report on FTCO (preview of web page 1 of three proven under):

Overvalued Dividend Inventory #8: KKR & Co. (KKR)

- Annual Valuation Return: -15.1%

KKR & Co is a worldwide funding firm with belongings beneath administration (AUM) of $496 billion. KKR operates on 4 enterprise traces: Non-public markets, public markets, capital markets, and principal actions.

KKR manages personal fairness funds that make investments capital for long-term appreciation by means of the Non-public Markets enterprise line.

KKR & Co launched Q1 2025 outcomes on Might 1st, 2025. In Q1, KKR reported fee-related earnings of $823 million, up 23% year-over-year, and complete working earnings of $1.1 billion, which was a 16% enhance.

Adjusted internet revenue reached $1.0 billion, marking a 20% rise. Charge-related earnings grew 37% to $3.4 billion for the final twelve months, whereas complete working earnings climbed 32% to $4.5 billion.

Adjusted internet revenue totaled $4.4 billion, reflecting a 37% enhance. KKR’s belongings beneath administration (AUM) rose 15% year-over-year to $664 billion, with fee-paying AUMs up 12% to $526 billion.

Click on right here to obtain our most up-to-date Certain Evaluation report on KKR (preview of web page 1 of three proven under):

Overvalued Dividend Inventory #7: HF Sinclair (DINO)

- Annual Valuation Return: -15.3%

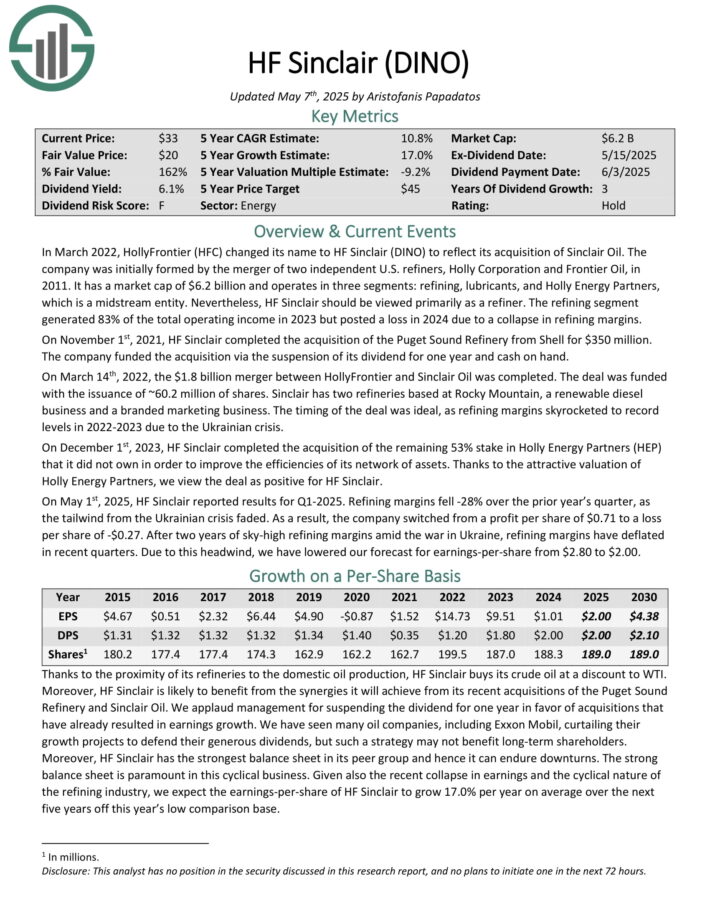

HF Sinclair was initially shaped by the merger of two impartial U.S. refiners, Holly Company and Frontier Oil, in

2011. It operates in three segments: refining, lubricants, and Holly Power Companions, which is a midstream entity.

HF Sinclair must be seen primarily as a refiner. The refining section generated 83% of the whole working revenue in 2023 however posted a loss in 2024 on account of a collapse in refining margins.

On Might 1st, 2025, HF Sinclair reported outcomes for Q1-2025. Refining margins fell -28% over the prior yr’s quarter, because the tailwind from the Ukrainian disaster light. Because of this, the corporate switched from a revenue per share of $0.71 to a loss per share of -$0.27.

Because of the proximity of its refineries to the home oil manufacturing, HF Sinclair buys its crude oil at a reduction to WTI.

Furthermore, HF Sinclair is prone to profit from the synergies it is going to obtain from its latest acquisitions of the Puget Sound Refinery and Sinclair Oil.

HF Sinclair has the strongest steadiness sheet in its peer group and it may endure downturns. The robust steadiness sheet is paramount on this cyclical enterprise.

Click on right here to obtain our most up-to-date Certain Evaluation report on DINO (preview of web page 1 of three proven under):

Overvalued Dividend Inventory #6: Constellation Power (CEG)

- Annual Valuation Return: -15.3%

Constellation Power Company was spun off from Exelon Company on February 1st, 2022. Constellation Power supplies clear and sustainable vitality options to properties, business companies, and wholesale prospects resembling municipalities and cooperatives.

The corporate’s vitality merchandise embrace electrical, pure gasoline, and renewables and markets such merchandise to corporations of all sizes.

Constellation Power operates 13 nuclear vegetation with a mixed 21 gigawatts of capability. The corporate operates within the decrease 48 U.S. states, Canada, and the UK.

On January tenth, 2025, the corporate introduced that it had agreed to buy Calpine Corp. utilizing a mixture of money and inventory. This transaction will make Constellation Power the most important clear vitality supplier within the U.S.

On Might sixth, 2025, Constellation Power reported first quarter outcomes for the interval ending March thirty first, 2025. For the quarter, income grew 8.6% to $6.69 billion, which was $1.35 billion above estimates.

On an adjusted foundation, earnings-per-share totaled $2.14, which in contrast favorably to adjusted earnings-per-share of $1.82 within the prior yr, however was $0.08 under expectations.

Constellation Power’s nuclear fleet produced 45,582 gigawatt-hours within the first quarter, up from 45,391 gigawatt-hours within the prior yr. Nuclear vegetation achieved a 94.1% capability issue, in comparison with 93.3% in Q1 2024.

Click on right here to obtain our most up-to-date Certain Evaluation report on CEG (preview of web page 1 of three proven under):

Overvalued Dividend Inventory #5: Energy Integrations Inc. (POWI)

- Annual Valuation Return: -15.5%

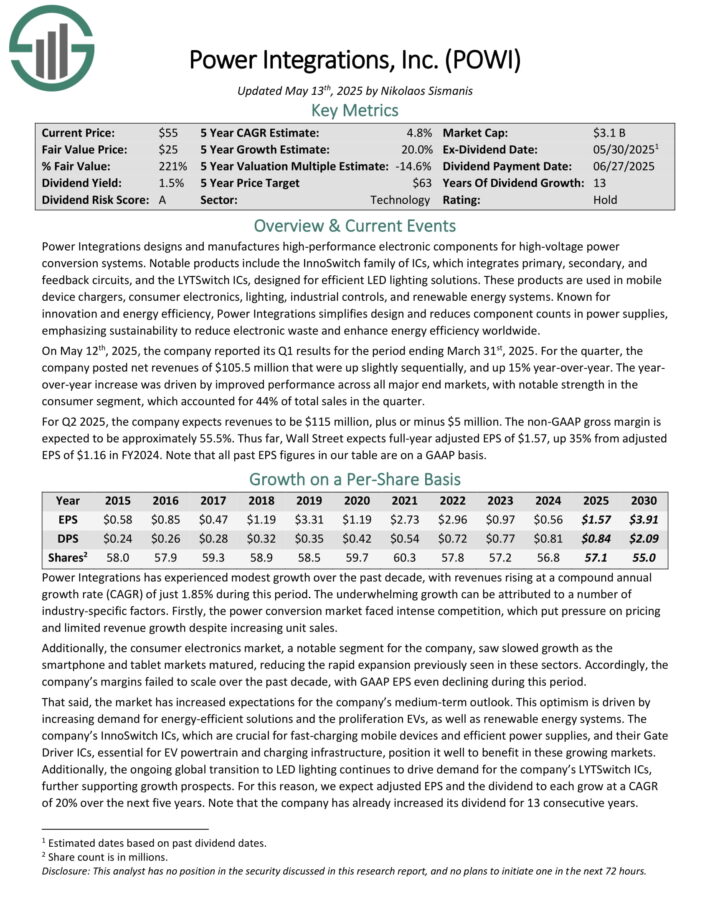

Energy Integrations designs and manufactures high-performance digital elements for high-voltage energy conversion methods.

Notable merchandise embrace the InnoSwitch household of ICs, which integrates major, secondary, and suggestions circuits, and the LYTSwitch ICs, designed for environment friendly LED lighting options.

These merchandise are utilized in cellular system chargers, shopper electronics, lighting, industrial controls, and renewable vitality methods.

On Might twelfth, 2025, the corporate reported its Q1 outcomes for the interval ending March thirty first, 2025. For the quarter, the corporate posted internet revenues of $105.5 million that have been up barely sequentially, and up 15% year-over-year.

The year-over-year enhance was pushed by improved efficiency throughout all main finish markets, with notable energy within the shopper section, which accounted for 44% of complete gross sales within the quarter.

Click on right here to obtain our most up-to-date Certain Evaluation report on POWI (preview of web page 1 of three proven under):

Overvalued Dividend Inventory #4: Hyster Yale (HY)

- Annual Valuation Return: -15.8%

Hyster-Yale Supplies Dealing with was based in 1985 and has since turn out to be a distinguished international participant within the supplies dealing with business.

The corporate designs, manufactures, and sells a complete vary of carry vehicles and aftermarket elements, serving various prospects throughout numerous sectors, together with manufacturing, warehousing, and logistics.

The corporate segments its income primarily into three classes: new tools gross sales, elements gross sales, and repair revenues.

On Might sixth, 2025, the corporate introduced outcomes for the primary quarter of 2025. The corporate reported Q1 non-GAAP EPS of $0.49, in-line with analysts’ estimates, and produced income of $910.4 million, which was down 14.1% year-over-year.

Hyster-Yale opened the yr with Q1 2025 consolidated revenues of $910 million, down 14% from final yr, as softer carry truck demand carried over from late 2024.

Internet revenue dipped to $8.6 million in comparison with $51.5 million a yr in the past, as decrease manufacturing volumes and value pressures weighed on margins. Stock ranges improved, down $69 million versus Q1 2024, exhibiting early progress in aligning manufacturing with present demand developments.

Encouragingly, the carry truck section noticed a notable rebound in bookings, up 13% year-over-year and 48% sequentially, pushed by energy within the Americas and EMEA.

Click on right here to obtain our most up-to-date Certain Evaluation report on HY (preview of web page 1 of three proven under):

Overvalued Dividend Inventory #3: Paramount Sources Ltd. (PRMRF)

- Annual Valuation Return: -16.0%

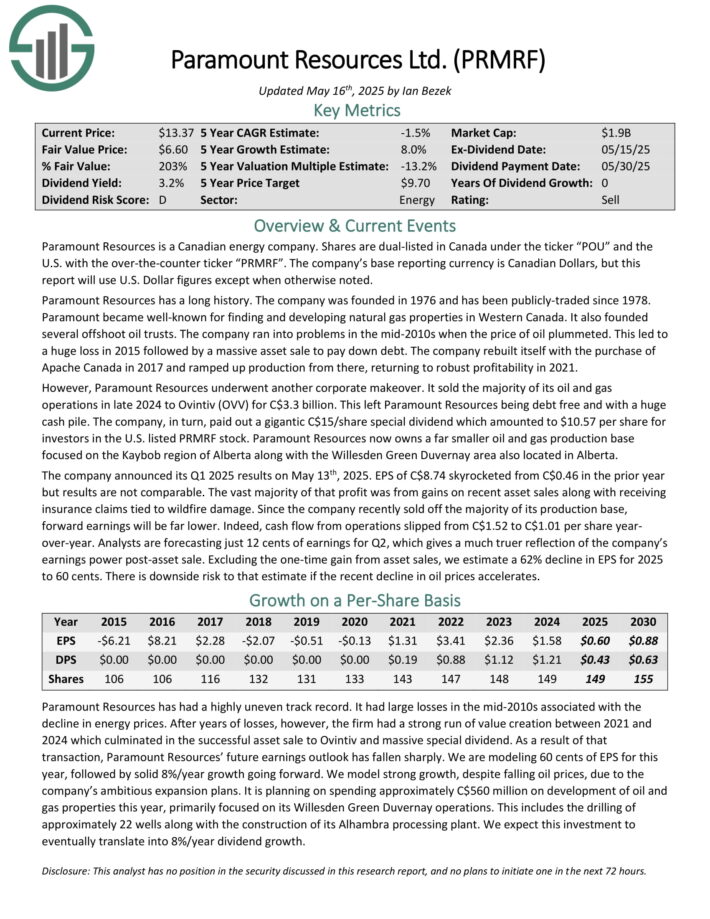

Paramount Sources is a Canadian vitality firm. Paramount Sources has an extended historical past. The corporate was based in 1976 and has been publicly-traded since 1978.

Paramount Sources now owns a much smaller oil and gasoline manufacturing base centered on the Kaybob area of Alberta together with the Willesden Inexperienced Duvernay space additionally positioned in Alberta.

The corporate introduced its Q1 2025 outcomes on Might thirteenth, 2025. EPS of C$8.74 skyrocketed from C$0.46 within the prior yr however outcomes usually are not comparable. The overwhelming majority of that revenue was from features on latest asset gross sales together with receiving insurance coverage claims tied to wildfire injury.

Because the firm lately bought off nearly all of its manufacturing base, ahead earnings will likely be far decrease. Certainly, money circulate from operations slipped from C$1.52 to C$1.01 per share year-over-year.

Analysts are forecasting simply 12 cents of earnings for Q2, which supplies a a lot more true reflection of the corporate’s earnings energy post-asset sale.

Click on right here to obtain our most up-to-date Certain Evaluation report on PRMRF (preview of web page 1 of three proven under):

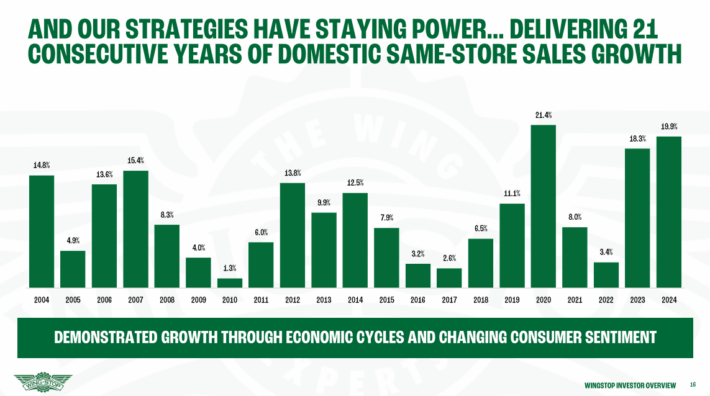

Overvalued Dividend Inventory #2: Wingstop Inc. (WING)

- Annual Valuation Return: -16.1%

Wingstop is headquartered in Addison, Texas and franchises and operates eating places beneath the Wingstop model.

The corporate has an extended monitor file of excessive progress.

Supply: Investor Presentation

On April 30, 2025, Wingstop Inc. reported its monetary outcomes for the fiscal first quarter ended March 29, 2025. The

firm achieved complete income of $171.1 million, marking a 17.4% enhance in comparison with the identical interval in 2024.

System-wide gross sales grew by 15.7% to $1.3 billion, pushed by a file 126 internet new restaurant openings, representing an 18% internet new unit progress. Home same-store gross sales skilled a modest enhance of 0.5%, whereas company-owned home same-store gross sales grew by 1.4%.

Internet revenue surged by 221% to $92.3 million, or $3.24 per diluted share, primarily on account of a $97.2 million acquire from the sale of Wingstop’s non-controlling curiosity in its United Kingdom grasp franchisee, Lemon Pepper Holdings, Ltd.

Adjusted internet revenue stood at $28.3 million, or $0.99 per diluted share, surpassing analyst expectations of $0.87 per share. Adjusted EBITDA elevated by 18.4% year-over-year to $59.5 million.

Click on right here to obtain our most up-to-date Certain Evaluation report on WING (preview of web page 1 of three proven under):

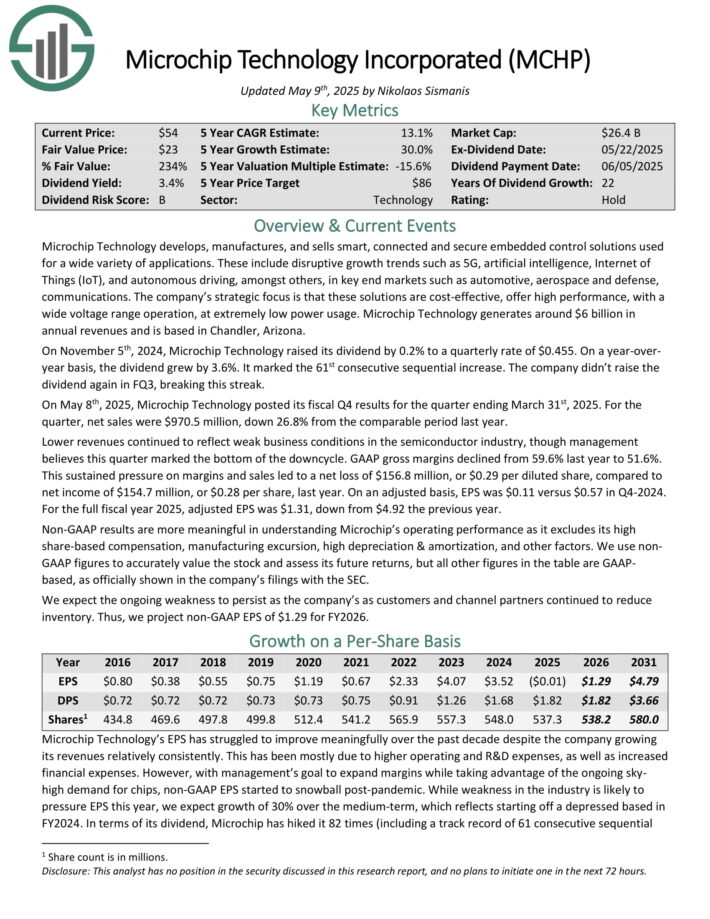

Overvalued Dividend Inventory #1: Microchip Expertise (MCHP)

- Annual Valuation Return: -20.9%

Microchip Expertise develops, manufactures, and sells sensible, linked and safe embedded management options used for all kinds of functions.

These embrace disruptive progress developments resembling 5G, synthetic intelligence, Web of Issues (IoT), and autonomous driving, amongst others, in key finish markets resembling automotive, aerospace and protection, communications.

Microchip Expertise generates round $6 billion in annual revenues and relies in Chandler, Arizona.

On Might eighth, 2025, Microchip Expertise posted its fiscal This fall outcomes for the quarter ending March thirty first, 2025. For the quarter, internet gross sales have been $970.5 million, down 26.8% from the comparable interval final yr.

Decrease revenues continued to mirror weak enterprise situations within the semiconductor business, although administration believes this quarter marked the underside of the downcycle. GAAP gross margins declined from 59.6% final yr to 51.6%.

This sustained stress on margins and gross sales led to a internet lack of $156.8 million, or $0.29 per diluted share, in comparison with internet revenue of $154.7 million, or $0.28 per share, final yr. On an adjusted foundation, EPS was $0.11 versus $0.57 in This fall-2024.

Click on right here to obtain our most up-to-date Certain Evaluation report on MCHP (preview of web page 1 of three proven under):

Ultimate Ideas

The inventory market has been on a virtually uninterrupted rally for the reason that Nice Recession. After a quick downturn throughout the coronavirus pandemic, the inventory market has as soon as once more raced to file highs.

Because of this, the S&P 500 is now markedly overvalued in accordance with a number of valuation metrics, such because the Shiller P/E ratio.

Subsequently, risk-averse revenue buyers must be cautious of overvalued dividend shares resembling the ten on this article.

If you’re taken with discovering high-quality dividend progress shares and/or different high-yield securities and revenue securities, the next Certain Dividend assets will likely be helpful:

Excessive-Yield Particular person Safety Analysis

Different Certain Dividend Sources

Thanks for studying this text. Please ship any suggestions, corrections, or inquiries to [email protected].

{kind=link}